INVESTOR MEETING 2012

Exhibit 99.1

|

($m)

|

2002

|

2003

|

2004

|

2005

|

2006

|

|

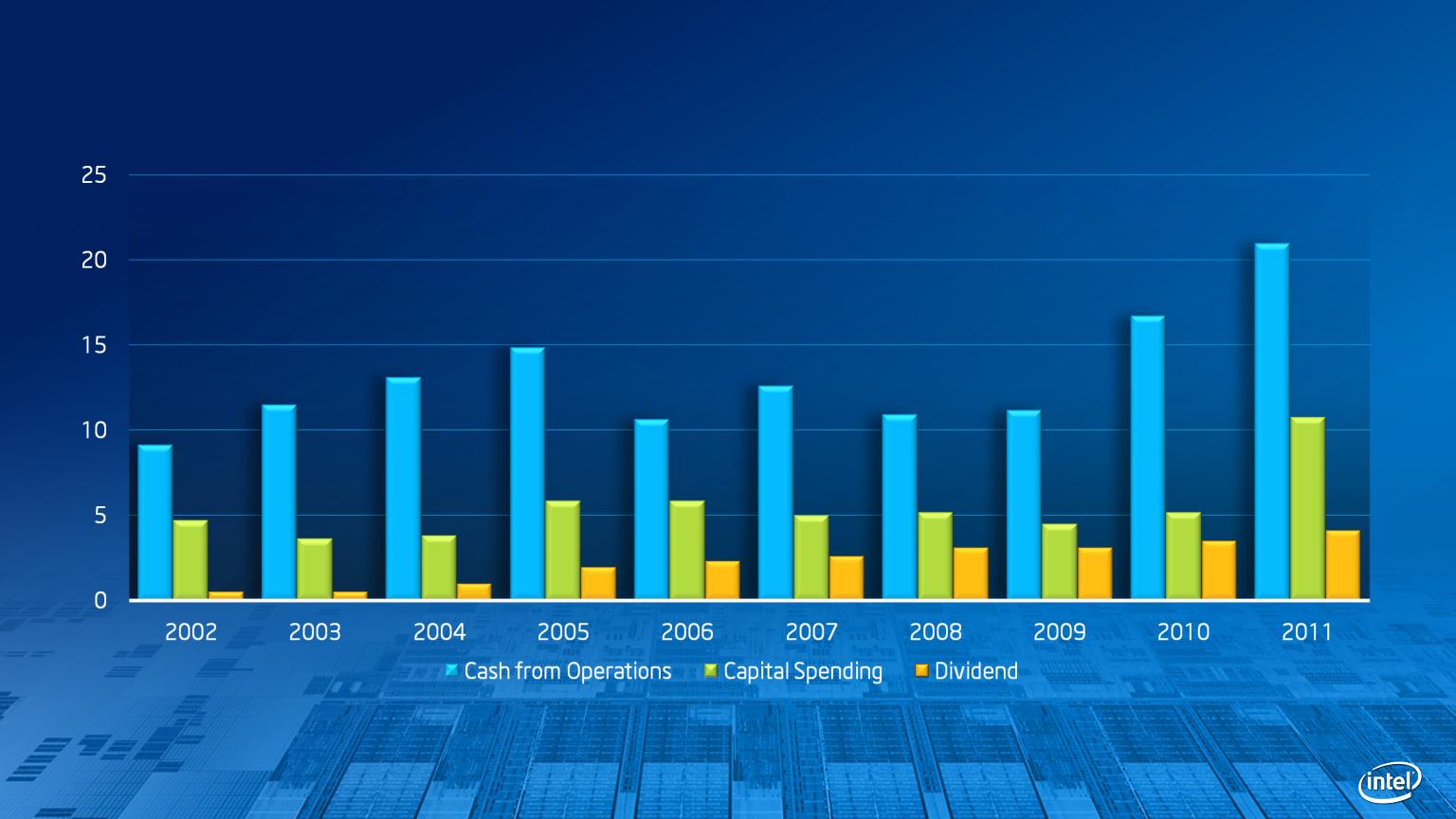

Net income (GAAP)

|

$ 3,117

|

$ 5,641

|

$ 7,516

|

$ 8,664

|

$ 5,044

|

|

Interest expense

|

84

|

62

|

50

|

19

|

24

|

|

Income tax adjustment (1)

|

(22)

|

(15)

|

(14)

|

(6)

|

(7)

|

|

Adjusted net operating profit after taxes

|

$ 3,179

|

$ 5,688

|

$ 7,552

|

$ 8,677

|

$ 5,061

|

|

|

|

|

|

|

|

|

|

2001

|

2002

|

2003

|

2004

|

2005

|

|

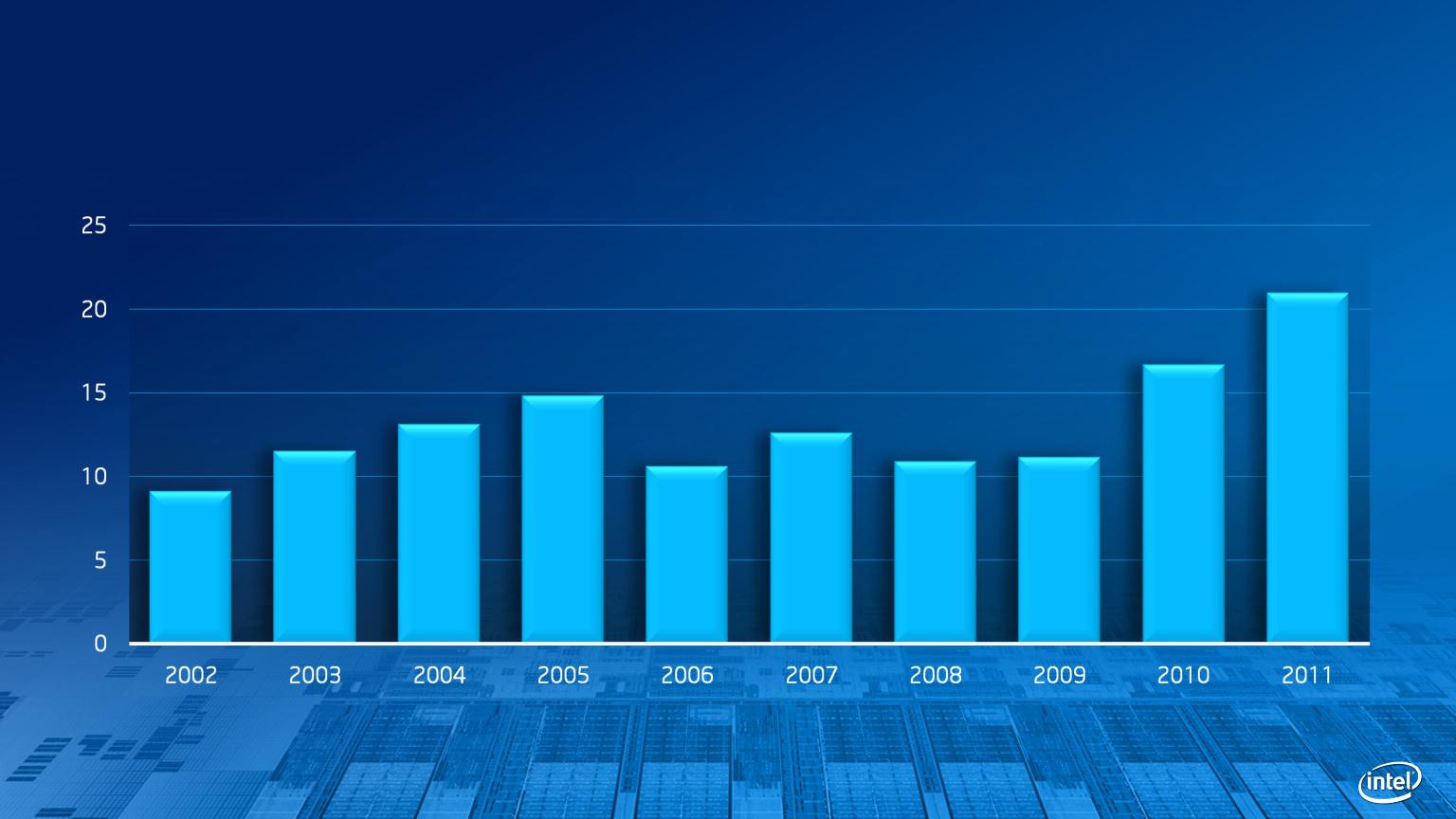

Total assets (GAAP) (2)

|

$ 44,395

|

$ 44,224

|

$ 47,143

|

$ 48,143

|

$ 48,309

|

|

Current liabilities

|

(6,570)

|

(6,595)

|

(6,879)

|

(8,006)

|

(9,234)

|

|

Invested capital

|

$ 37,825

|

$ 37,629

|

$ 40,264

|

$ 40,137

|

$ 39,075

|

|

|

|

|

|

|

|

|

|

2002

|

2003

|

2004

|

2005

|

2006

|

|

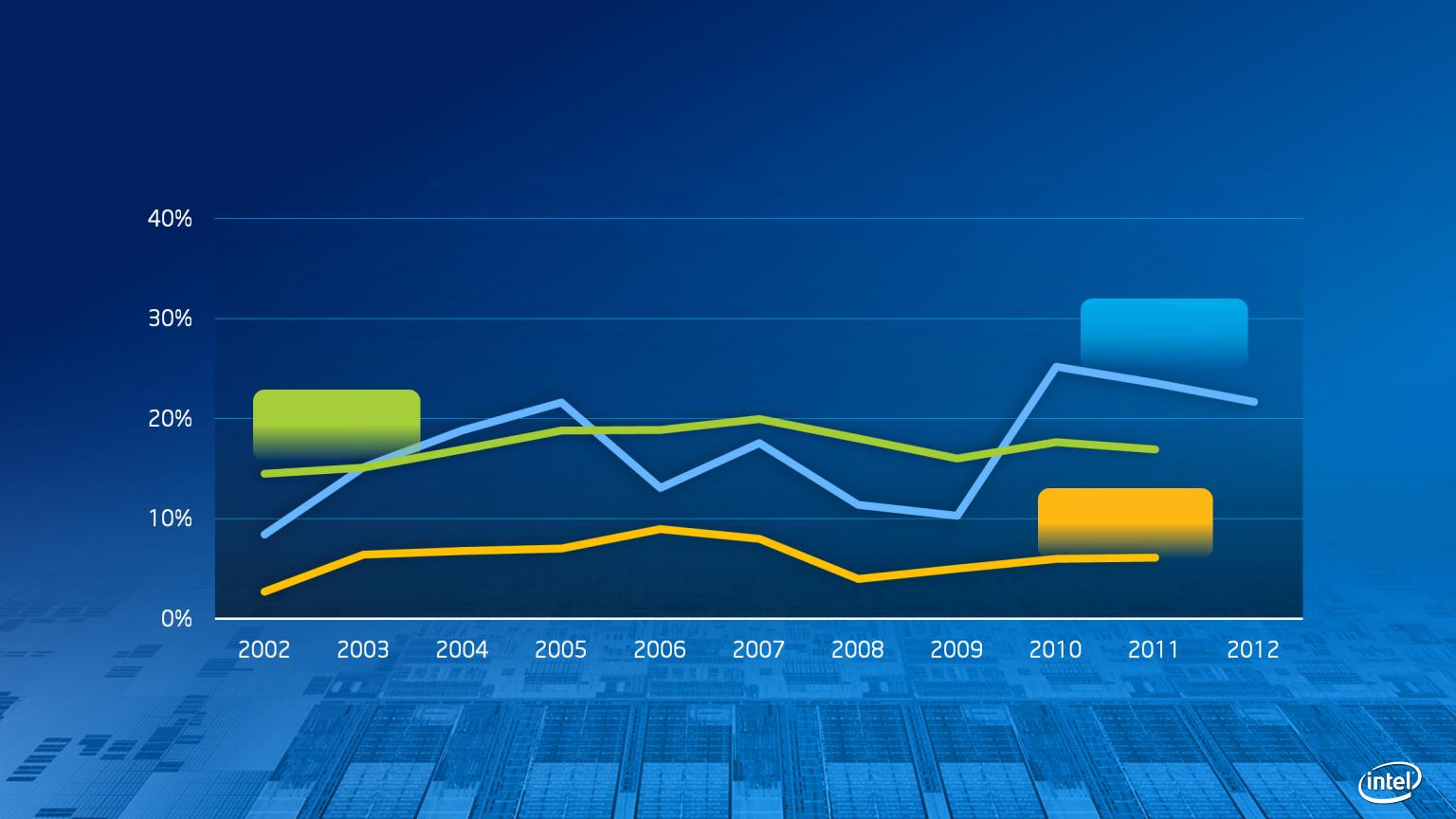

Return on invested capital (Adjusted net operating

profit after taxes / prior year end invested capital) |

8.4%

|

15.1%

|

18.8%

|

21.6%

|

13.0%

|

|

|

|

|

|

|

|

|

Net income/ prior year end total assets

|

7.0%

|

12.8%

|

15.9%

|

18.0%

|

10.4%

|

|

|

|

|

|

|

|

|

(1) Assumed tax effect of interest expense based on the

effective tax rate |

|

|

|

|

|

|

|

|

|

|

|

|

|

(2) 2005-2008 Total assets has been adjusted due to

changes to the accounting for convertible debt instruments |

|

|

|

|

|

|

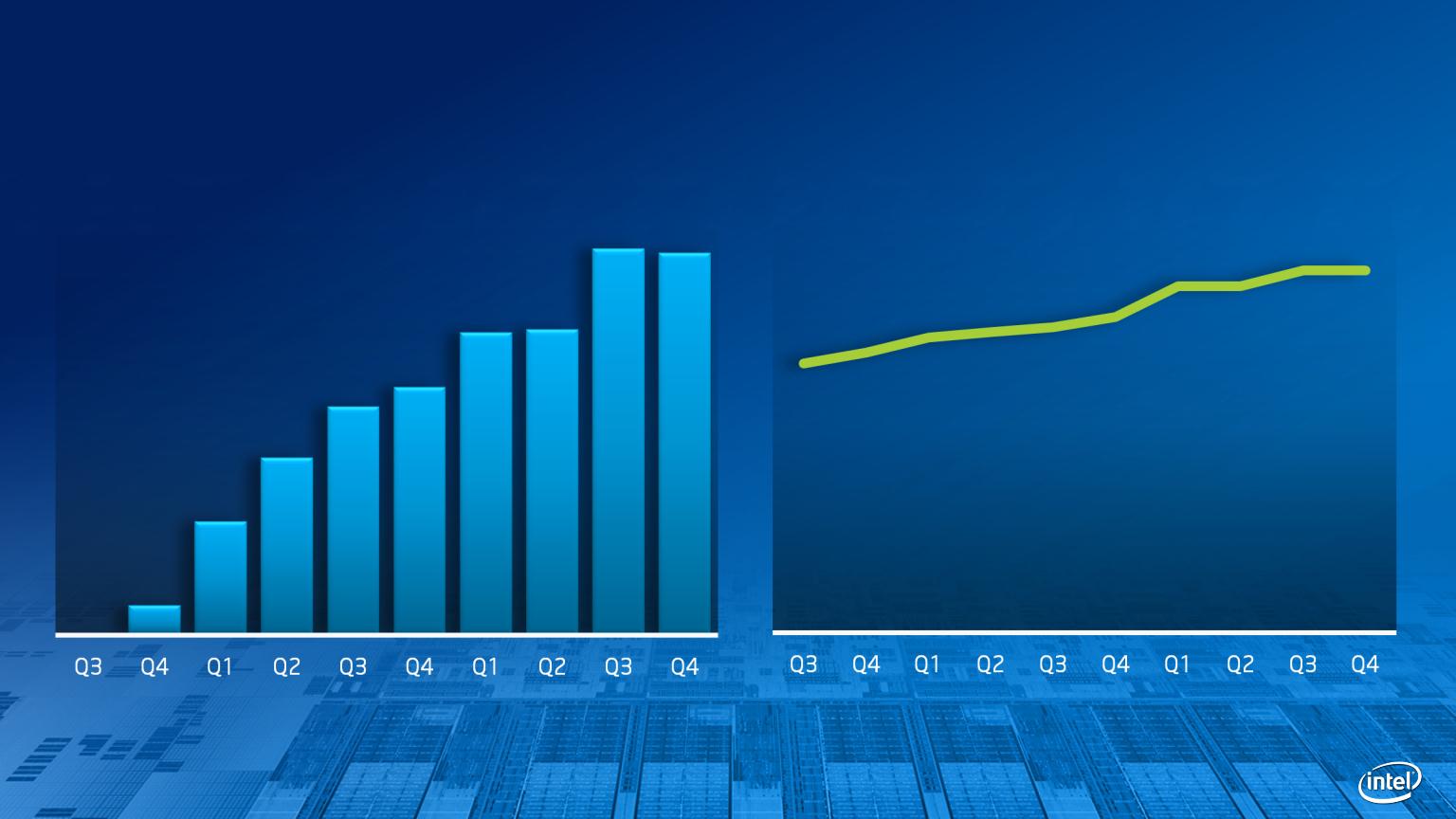

($m)

|

2007

|

2008

|

2009

|

2010

|

2011

|

|

|

Net income (GAAP)

|

$ 6,976

|

$ 5,292

|

$ 4,369

|

$ 11,464

|

$ 12,942

|

|

|

Interest expense

|

15

|

8

|

1

|

0

|

41

|

|

|

Income tax adjustment (1)

|

(4)

|

(2)

|

(0)

|

0

|

(11)

|

|

|

Adjusted net operating profit after taxes

|

$ 6,987

|

$ 5,298

|

$ 4,370

|

$ 11,464

|

$ 12,972

|

|

|

|

|

|

|

|

|

|

|

|

2006

|

2007

|

2008

|

2009

|

2010

|

|

|

Total assets (GAAP) (2)

|

$ 48,372

|

$ 55,664

|

$ 50,472

|

$ 53,095

|

$ 63,186

|

|

|

Current liabilities

|

(8,514)

|

(8,571)

|

(7,818)

|

(7,591)

|

(9,327)

|

|

|

Invested capital

|

$ 39,858

|

$ 47,093

|

$ 42,654

|

$ 45,504

|

$ 53,859

|

|

|

|

|

|

|

|

|

|

|

|

2007

|

2008

|

2009

|

2010

|

2011

|

10 YR AVG

|

|

Return on invested capital (Adjusted net

operating profit after taxes / prior year end invested capital) |

17.5%

|

11.3%

|

10.2%

|

25.2%

|

24.1%

|

16.5%

|

|

|

|

|

|

|

|

|

|

Net income/ prior year end total assets

|

14.4%

|

9.5%

|

8.7%

|

21.6%

|

20.5%

|

13.9%

|

|

|

|

|

|

|

|

|

|

(1) Assumed tax effect of interest expense based

on the effective tax rate |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(2) 2005-2008 Total assets has been adjusted due

to changes to the accounting for convertible debt instruments |

|

|

|

|

|

|

|

($m)

|

|

2012 Forecast

|

|

|

Consensus net income (1)

|

|

$ 12,696

|

|

|

Annualized interest expense (2)

|

|

124

|

|

|

Income tax adjustment (3)

|

|

(35)

|

|

|

Adjusted net operating profit after taxes

|

|

$ 12,785

|

|

|

|

|

|

|

|

|

|

2011

|

|

|

Total assets (GAAP)

|

|

$ 71,119

|

|

|

Current liabilities

|

|

(12,028)

|

|

|

Invested capital

|

|

$ 59,091

|

|

|

|

|

|

|

|

|

|

2012 Forecast

|

|

|

Return on invested capital (Adjusted net operating profit after taxes / prior year end invested capital)

|

|

21.6%

|

|