UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 28, 2019. | |

or | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to . | |

Commission File Number 000-06217

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||

(Address of principal executive offices) | (Zip Code) | |||

Registrant’s telephone number, including area code (408 ) 765-8080

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading symbol | Name of each exchange on which registered | ||

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every interactive data file required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Accelerated Filer | Non-Accelerated Filer | Smaller Reporting Company | Emerging Growth Company | |

☑ | ☐ | ☐ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

Aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant as of June 28, 2019, based upon the closing price of the common stock as reported by the Nasdaq Global Select Market on such date, was $212.0 billion. 4,277 million shares of common stock were outstanding as of January 17, 2020.

DOCUMENTS INCORPORATED BY REFERENCE

TABLE OF CONTENTS

ORGANIZATION OF OUR ANNUAL REPORT ON FORM 10-K

The order and presentation of content in our Form 10-K differs from the traditional SEC Form 10-K format. Our format is designed to improve readability and better presents how we organize and manage our business. See "Form 10-K Cross-Reference Index" within the Financial Statements and Supplemental Details for a cross-reference index to the traditional SEC Form 10-K format. To reflect our focus on transforming from a PC-centric1 company to a data-centric company, we have presented our data-centric businesses1 first in the "Segment Trends and Results" within MD&A.

We have defined certain terms and abbreviations used throughout our Form 10-K in "Key Terms" within the Financial Statements and Supplemental Details.

The preparation of our Consolidated Financial Statements is in conformity with U.S. GAAP. We have included key metrics that we use to measure our business, some of which are non-GAAP measures. See these "Non-GAAP Financial Measures" within MD&A.

FUNDAMENTALS OF OUR BUSINESS | PAGE | |

Introduction to Our Business | ||

A Year in Review | ||

Our Strategy | ||

Our Capital | ||

MANAGEMENT'S DISCUSSION AND ANALYSIS | ||

How We Organize Our Business | ||

Our Products | ||

Segment Trends and Results | ||

Consolidated Results of Operations | ||

Liquidity and Capital Resources | ||

Contractual Obligations | ||

Quantitative and Qualitative Disclosures about Market Risk | ||

Non-GAAP Financial Measures | ||

OTHER KEY INFORMATION | ||

Selected Financial Data | ||

Sales and Marketing | ||

Competition | ||

Intellectual Property Rights and Licensing | ||

Critical Accounting Estimates | ||

Risk Factors | ||

Properties | ||

Market for Our Common Stock | ||

Information about Our Executive Officers | ||

Availability of Company Information | ||

FINANCIAL STATEMENTS AND SUPPLEMENTAL DETAILS | ||

Auditor's Reports | ||

Consolidated Financial Statements | ||

Notes to the Consolidated Financial Statements | ||

Key Terms | ||

Financial Information by Quarter | ||

Controls and Procedures | ||

Exhibits | ||

Form 10-K Cross-Reference Index | ||

1 | Intel's definition is included in "Key Terms" within the Financial Statements and Supplemental Details. |

FORWARD-LOOKING STATEMENTS

This Form 10-K contains forward-looking statements that involve a number of risks and uncertainties. Words such as “anticipates,” “expects,” “intends,” “goals,” “plans,” "opportunities," "future," “believes,” “seeks,” "targets," “estimates,” “continues,” “may,” “will,” “would,” “should,” “could,” and variations of such words and similar expressions are intended to identify such forward-looking statements. In addition, any statements that refer to projections of our future financial performance; future business, social, and environmental performance, goals, and measures; our anticipated growth and trends in our businesses; projected growth and trends in markets relevant to our businesses; future products and technology and the expected availability and benefits of such products and technology; expected timing and impact of acquisitions, divestitures, and other significant transactions; expected completion of restructuring activities; expected returns to stockholders; future production capacity and product supply; uncertain events or assumptions, including statements relating to TAM or market opportunity; and other characterizations of future events or circumstances are forward-looking statements. Such statements are based on management's expectations as of the date of this filing and involve many risks and uncertainties that could cause our actual results to differ materially from those expressed or implied in our forward-looking statements. Such risks and uncertainties include those described throughout this report and particularly in “Risk Factors” within Other Key Information. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. Readers are urged to carefully review and consider the various disclosures made in this Form 10-K and in other documents we file from time to time with the SEC that disclose risks and uncertainties that may affect our business. Unless specifically indicated otherwise, the forward-looking statements in this Form 10-K do not reflect the potential impact of any divestitures, mergers, acquisitions, or other business combinations that have not been completed as of the date of this filing. In addition, the forward-looking statements in this Form 10-K are made as of the date of this filing, including expectations based on third-party information and projections that management believes to be reputable, and Intel does not undertake, and expressly disclaims any duty, to update such statements, whether as a result of new information, new developments, or otherwise, except to the extent that disclosure may be required by law.

NOTE REGARDING THIRD-PARTY INFORMATION

This Form 10-K includes market data and certain other statistical information and estimates that are based on reports and other publications from industry analysts, market research firms, and other independent sources, as well as management’s own good faith estimates and analyses. Intel believes these third-party reports to be reputable, but has not independently verified the underlying data sources, methodologies, or assumptions. The reports and other publications referenced are generally available to the public and were not commissioned by Intel. Information that is based on estimates, forecasts, projections, market research, or similar methodologies is inherently subject to uncertainties, and actual events or circumstances may differ materially from events and circumstances reflected in this information.

* | Other names and brands may be claimed as the property of others. |

The Bluetooth® word mark and logos are registered trademarks owned by Bluetooth SIG, Inc. and any use of such marks by Intel Corporation is under license.

Intel, 3D XPoint, Celeron, Intel Agilex, Intel Atom, Intel Core, eASIC, Intel Inside, the Intel logo, the Intel Inside logo, Intel Nervana, Intel Optane, Itanium, Movidius, Myriad, OpenVINO, Pentium, Quark, Stratix, Thunderbolt, Intel vPro, Xeon, and are trademarks of Intel Corporation or its subsidiaries.

| 1 | |

| 2 | |

| ||||

INTRODUCTION TO OUR BUSINESS | ||||

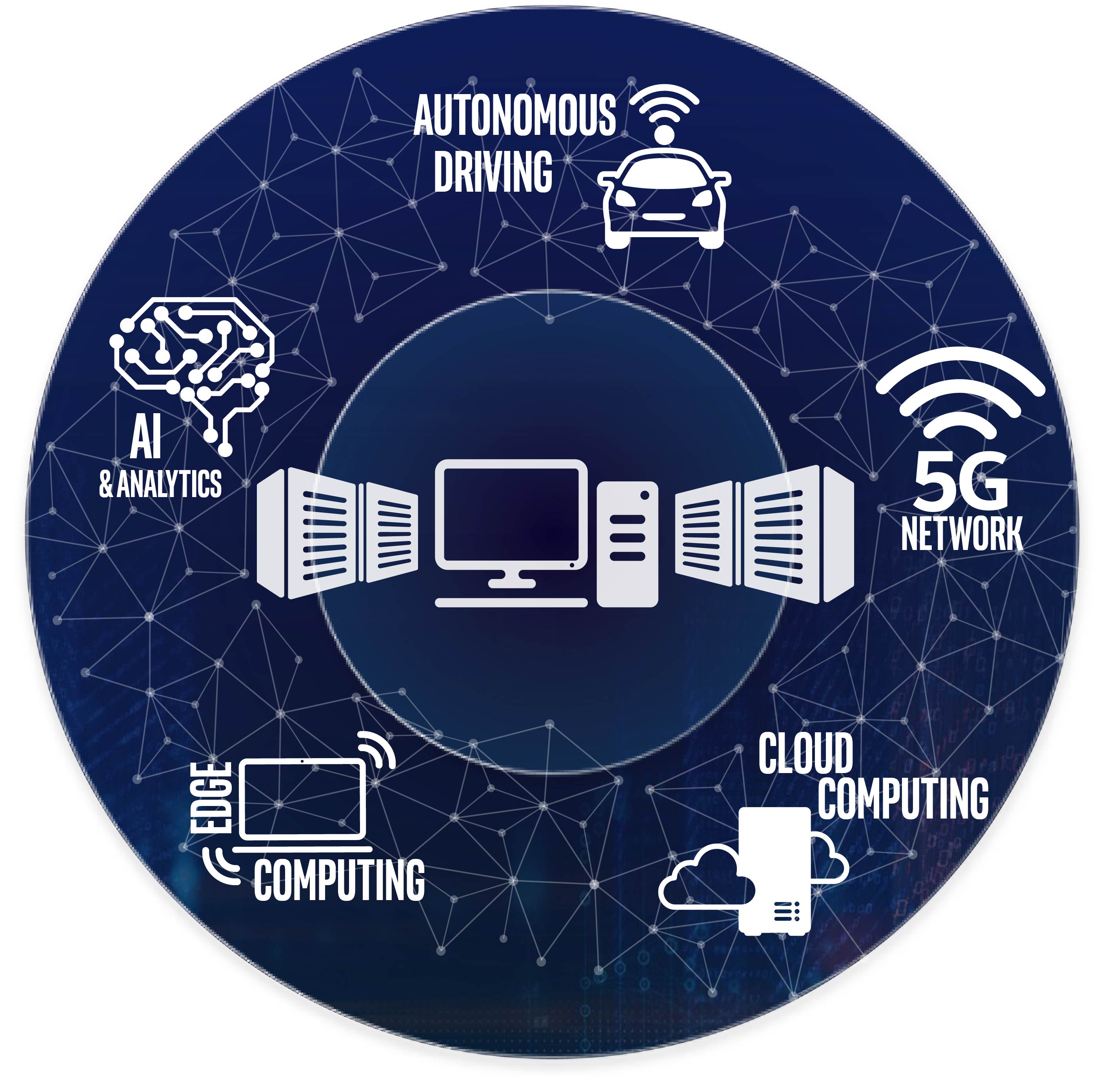

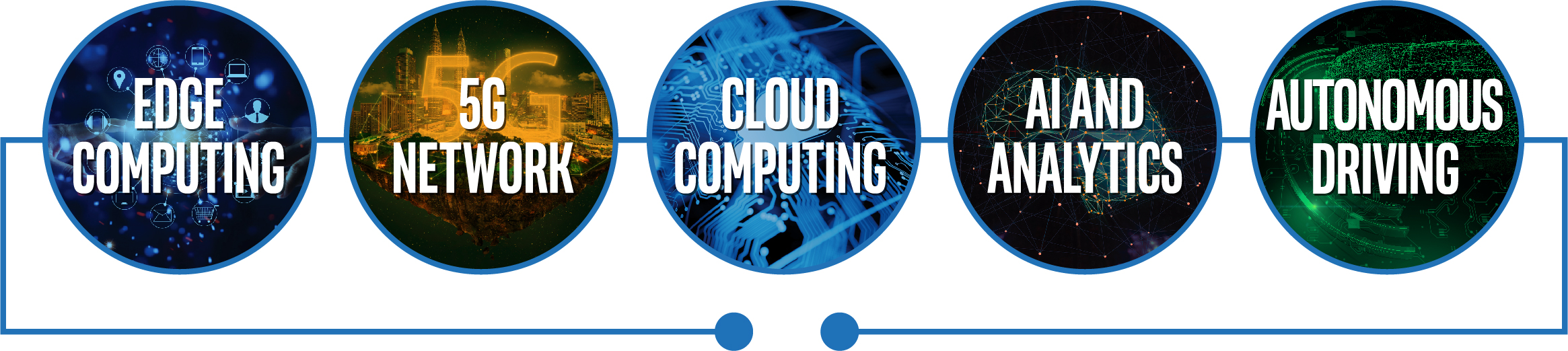

Intel was founded in 1968 and our technology has been at the heart of computing breakthroughs ever since. More than 50 years later, we are a world leader in the design and manufacturing of essential technologies that power the cloud and an increasingly smart, connected world. Intel is transforming from a PC-centric company to a data-centric company, with workload-optimized solutions designed to help a broad set of customers process, move, and store ever-increasing amounts of data. This exponential growth of data is reshaping computing and expanding our opportunity. We are investing to lead data-driven technology inflections that position us to play a bigger role in the success of our customers. These include: the rise of AI, the transformation of networks, the intelligent edge1 emerging with the Internet of Things, and autonomous driving. Intel’s ambitions have never been greater: to create world-changing technology that enriches the lives of every person on earth. Our commitment to corporate responsibility and to creating an inclusive environment to support the talent of our amazing people supports our ambitions and makes us stronger. When every employee has a voice and a sense of belonging, Intel can be more innovative, agile, and competitive. | ||||

| "We are at a key inflection point with the exponential growth of data creating massive demand for semiconductors. Cloud workloads are diversifying, networks are transforming, and more computing performance is moving to the edge. We have been on a multi-year journey to reposition the company’s portfolio to take advantage of this industry catalyst. Today, we have the product and technology leadership that uniquely positions us to capitalize on these trends, and we are investing in the IP required to help our customers win the inflections of the future." —Bob Swan, Chief Executive Officer | |||

1 Intel's definition is included in "Key Terms" within the Financial Statements and Supplemental Details. | ||||

| 3 | |

A YEAR IN REVIEW |

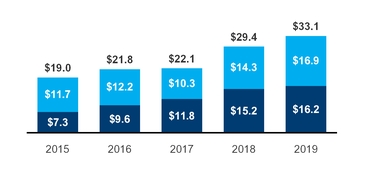

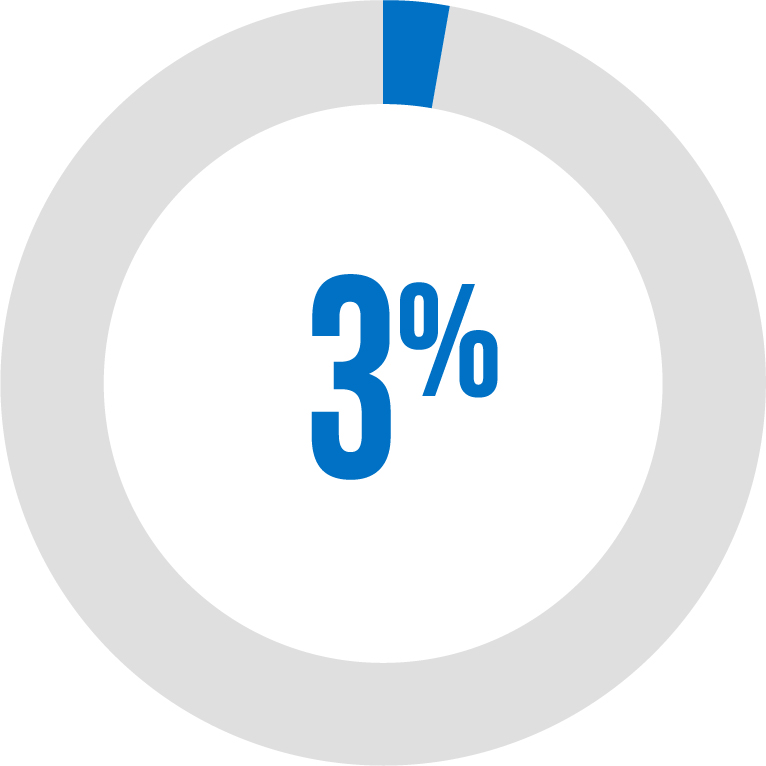

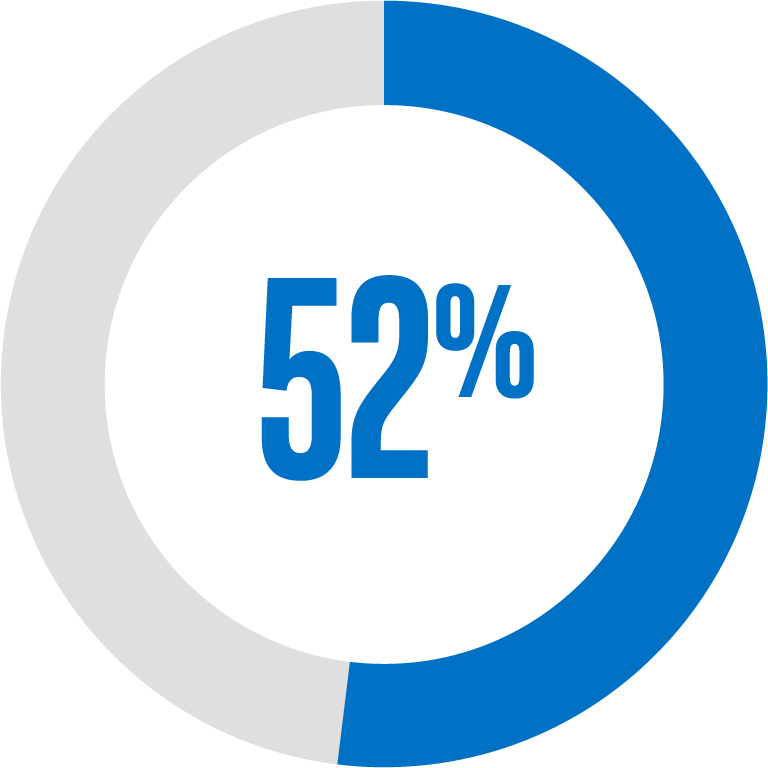

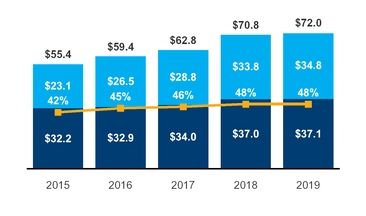

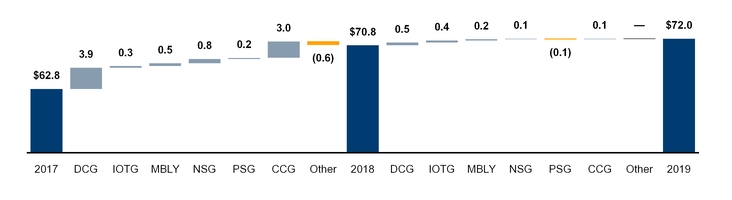

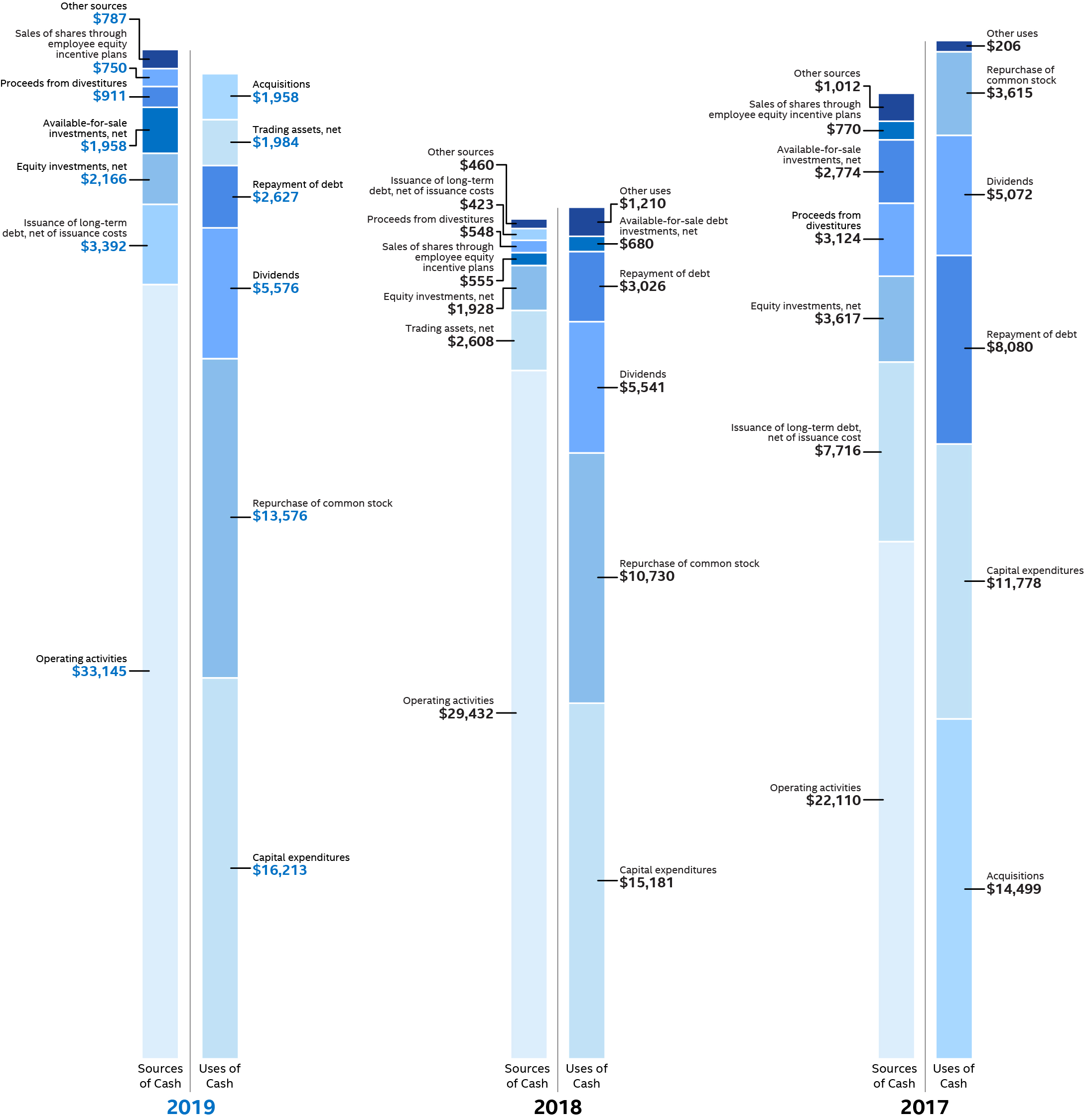

Our transformation to a data-centric company continued in 2019, and we experienced strong demand and reached critical product milestones. We achieved record revenue of $72.0 billion, 48% of which was from our data-centric businesses. We invested $13.4 billion in R&D while reducing our spending to 27% of revenue. Additionally, we made capital investments of $16.2 billion, generated $33.1 billion cash from operations and $16.9 billion of free cash flow, and returned $5.6 billion in dividends to stockholders. We continue to focus on improving supply and supporting our customers' growth. We increased our wafer capacity during 2019; however, we did not see a commensurate increase in client CPU unit volume as wafer capacity was largely consumed by increases in modem and chipset volumes, and unit die sizes. Our 10nm manufacturing process entered full production as we launched our first products from this advanced technology. We are accelerating the pace of process node introductions and moving back to a 2- to 2.5-year cadence. We are on track to deliver our first 7nm-based product, a discrete GPU, at the end of 2021. 5G continues to be a strategic priority, and our exit from the 5G smartphone modem business is enabling us to increase the focus of our 5G efforts on the opportunity to modernize network and edge infrastructure. |  | |

"We achieved record revenue for the fourth consecutive year, exercised discipline to drive spending efficiencies, and returned capital to our stockholders. Our results reflect a relentless commitment to improve execution that benefits our customers and increases shareholder value." —George Davis, Chief Financial Officer | ||

REVENUE | OPERATING INCOME | DILUTED EPS | CASH FLOWS | |||

■ PC-CENTRIC $B ■ DATA-CENTRIC $B | ■ GAAP $B ■ NON-GAAP $B | ■ GAAP ■ NON-GAAP | ■ OPERATING CASH FLOW $B ■ FREE CASH FLOW1 $B | |||

$72.0B | $22.0B | $23.8B | $4.71 | $4.87 | $33.1B | $16.9B | |||||||

GAAP | GAAP | non-GAAP1 | GAAP | non-GAAP1 | GAAP | non-GAAP1 | |||||||

Revenue up 2% from 2018; Data-centric up 3% and PC-centric flat | Operating income down $1.3B or 5% from 2018; 2019 operating margin at 31% | Operating income down $797M or 3% from 2018; 2019 operating margin at 33% | Diluted EPS up $0.23 or 5% from 2018 | Diluted EPS up $0.29 or 6% from 2018 | Operating cash flow up $3.7B or 13%; operating cash flow to net income at 157% | Free cash flow up $2.7B or 19%; free cash flow to non-GAAP net income at 78% | |||||||

High-performance product sales in the second half of 2019, partially offset by NAND pricing pressure and decrease in platform2 unit sales | Lower gross margin from decrease in NAND market pricing and lower platform unit sales, partially offset by platform ASP strength | Lower shares outstanding and platform ASP strength, partially offset by a decrease in platform unit sales and lower NAND market pricing | Working capital changes driven by tax and other assets and liabilities, partially offset by lower memory prepayments and inventory build | ||||||||||

GOAL (2019 - 2021) | GOAL (2019 - 2021) | GOAL (2019 - 2021) | GOAL (2019 - 2021) | |||||||

Low single-digit growth over the next three years to $76B-$78B; data-centric businesses high single- digit growth and PC-centric business approximately flat to slightly down | Keep non-GAAP operating margin roughly flat at approximately 32% over the next three years | Grow non-GAAP diluted EPS in line with revenue over the next three years | Achieve free cash flow of approximately 80% of non-GAAP net income by 2021 | |||||||

Progress | Progress | Progress | Progress | |||||||

Revenue grew 2% from 2018 to 2019, to $72.0B | Non-GAAP operating margin was 33% in 2019 | Non-GAAP diluted EPS grew 6% from 2018 to 2019; revenue grew 2% over the same period | Free cash flow was 78% of non-GAAP net income | |||||||

1 | See "Non-GAAP Financial Measures" within MD&A. |

2 | See "Our Products" within MD&A. |

| FUNDAMENTALS OF OUR BUSINESS | 4 | |

DATA-CENTRIC BUSINESSES EXPAND WITH NEW OPPORTUNITIES | PC-CENTRIC BUSINESS INNOVATES | ||||

Data-Centric Portfolio Launch | 10nm-based 10th Generation Intel® CoreTM Shipping | ||||

We introduced a portfolio of data-centric solutions consisting of 2nd generation Intel® Xeon® Scalable processors, Intel® Optane™ DC memory and storage solutions, and software and platform technologies optimized to help our customers extract more value from their data. Our latest data center solutions target a wide range of use cases within cloud computing, network infrastructure, and intelligent edge applications, and support high-growth workloads, including AI and 5G. | |||||

We started shipping our 10nm-based 10th generation Intel® CoreTM processors, previously referred to as Ice Lake. Our 10th generation Intel® CoreTM processor silicon will enable the first wave of PCs with instructions for AI, includes an all-new CPU Core architecture and Gen 11 graphics engine, and is the first client CPU to integrate Wi-Fi 6 and Thunderbolt™ 3 connectivity modules. | |||||

|  | ||||

| |||||

10nm FPGAs Shipping |  | ||||

We began shipping engineering samples of Intel® Agilex™ FPGAs to customers. The 10nm-based FPGAs are used by our customers to develop advanced solutions for networking, 5G, and accelerated data analytics. The Intel® Agilex™ FPGA family leverages heterogeneous 3D SiP technology to deliver higher performance or higher power efficiency. | |||||

Project Athena Innovation Program | |||||

Project Athena is a new multi-year innovation program to help the PC ecosystem create advanced laptops that meet ambitious key experience indicators in performance, responsiveness, battery life, form factor, and AI. The first laptops verified through the innovation program became |  | ||||

Habana Labs Acquisition | |||||

We acquired Habana Labs Ltd., an Israel-based developer of programmable deep learning accelerators for the data center, for approximately $1.7 billion. Habana's AI processors provide data scientists and developers with accelerator hardware that improves processing performance and reduces power consumption. Habana's Gaudi* AI training processor is currently sampling with select hyperscale customers. Large-node training systems based on Gaudi* are expected to deliver up to four times increase in throughput versus systems built with the equivalent number of GPUs. The acquisition strengthens our AI portfolio and accelerates our efforts in the nascent, fast-growing AI silicon market. | |||||

available in 2019, identified by the visual marker "Engineered for Mobile Performance." | |||||

BIG BETS UPDATE |  | ||||||

We aim to be at the forefront of the constant technological change in our industry. We will evaluate new and existing big bets based on the following criteria: the "bet" is leading the edge of a technology inflection, it plays a significant role in our customers' success, and it offers a clear path to profitability and attractive returns. Currently, our big bets are memory, autonomous driving, and 5G. | |||||||

We exited 5G smartphone modem business to increase the focus of our 5G efforts on the broader opportunity to modernize network and edge infrastructure. | |||||||

| We continue to make progress in memory and autonomous driving. We launched Intel® Optane™ DC persistent memory for the data center and continue to take steps to improve NAND profitability. Mobileye's EyeQ*5, the vision central computer performing sensor fusion for fully autonomous driving, is operational in Mobileye's autonomous test vehicles. | ||||||

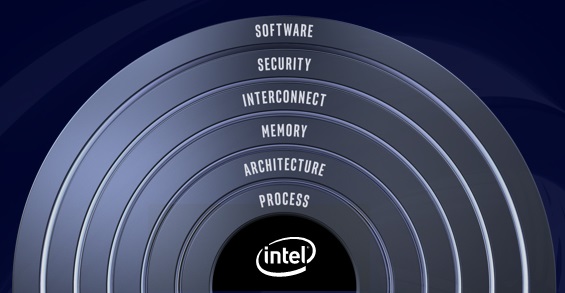

"While process and CPU leadership remain fundamentally important, an extraordinary rate of innovation is required across a combination of foundational building blocks, including architecture, memory, interconnect, security, and software, to take full advantage of the opportunities created by the explosion of data." —Dr. Venkata (Murthy) M. Renduchintala, Group President of the Technology, Systems Architecture and Client Group and Chief Engineering Officer | |||||||

| FUNDAMENTALS OF OUR BUSINESS | 5 | |

OUR STRATEGY |

Data has become a driving force in society. Our customers are asking for solutions to turn data into actionable insights, amazing experiences, and operational efficiencies. Intel platforms provide the foundation for these solutions because we have developed a portfolio of data-centric technologies that span the data center to the edge, enabling us to play a differentiated and growing role in the success of our customers.

Moore’s Law, a law of economics predicted by Intel’s co-founder Gordon Moore more than 50 years ago, continues to be a strategic priority and differentiator. We make significant investments and innovations in our silicon manufacturing technologies and platforms. Our proprietary technologies make it possible to integrate products and platforms that address evolving customer needs and expand the markets we serve. However, making the best semiconductors requires more than just the best manufacturing process technologies.

We manufacture a majority of our products in our own facilities and make significant investments in silicon manufacturing technologies and platforms as an IDM. We are focused on strengthening our IDM position by collaborating with the broader silicon manufacturing and design ecosystem to improve our design efficiency, including increased strategic use of third-party design IP and foundries for certain components to allow us to focus on differentiating technology. We are also pursuing design simplification to accelerate innovation, including a significant reduction of design rules for future process nodes, to allow us to deliver the best solutions for our customer.

MAKE THE WORLD'S BEST SEMICONDUCTORS |

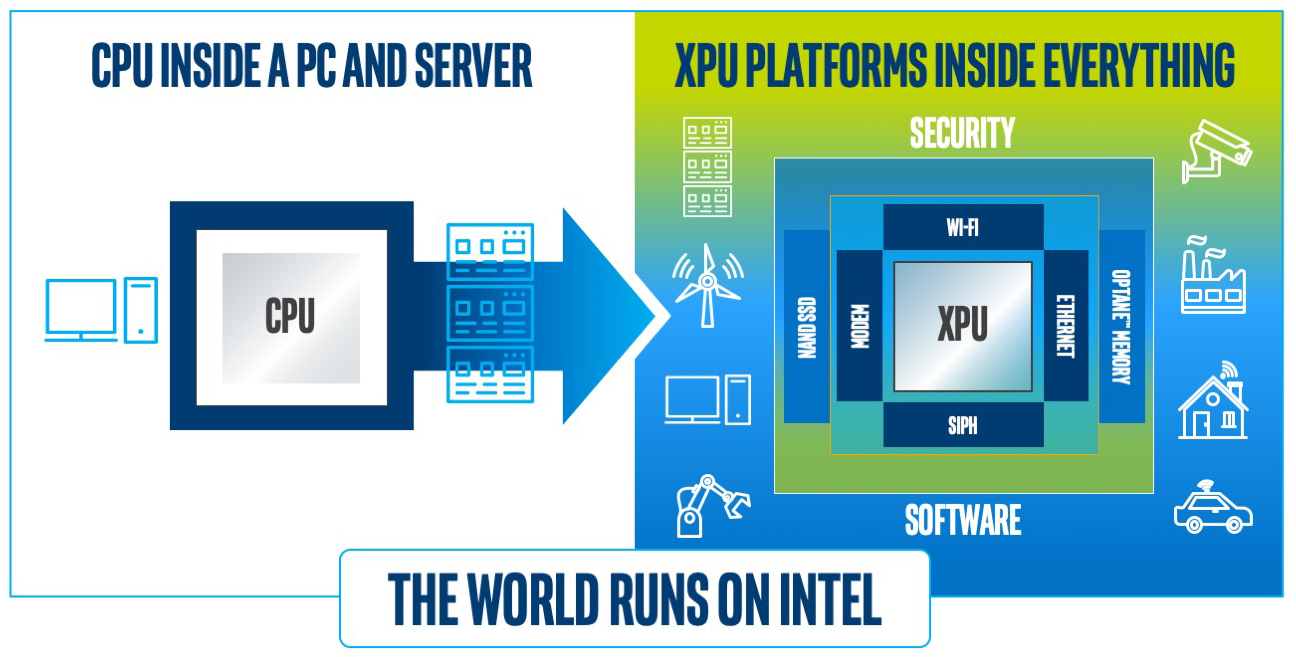

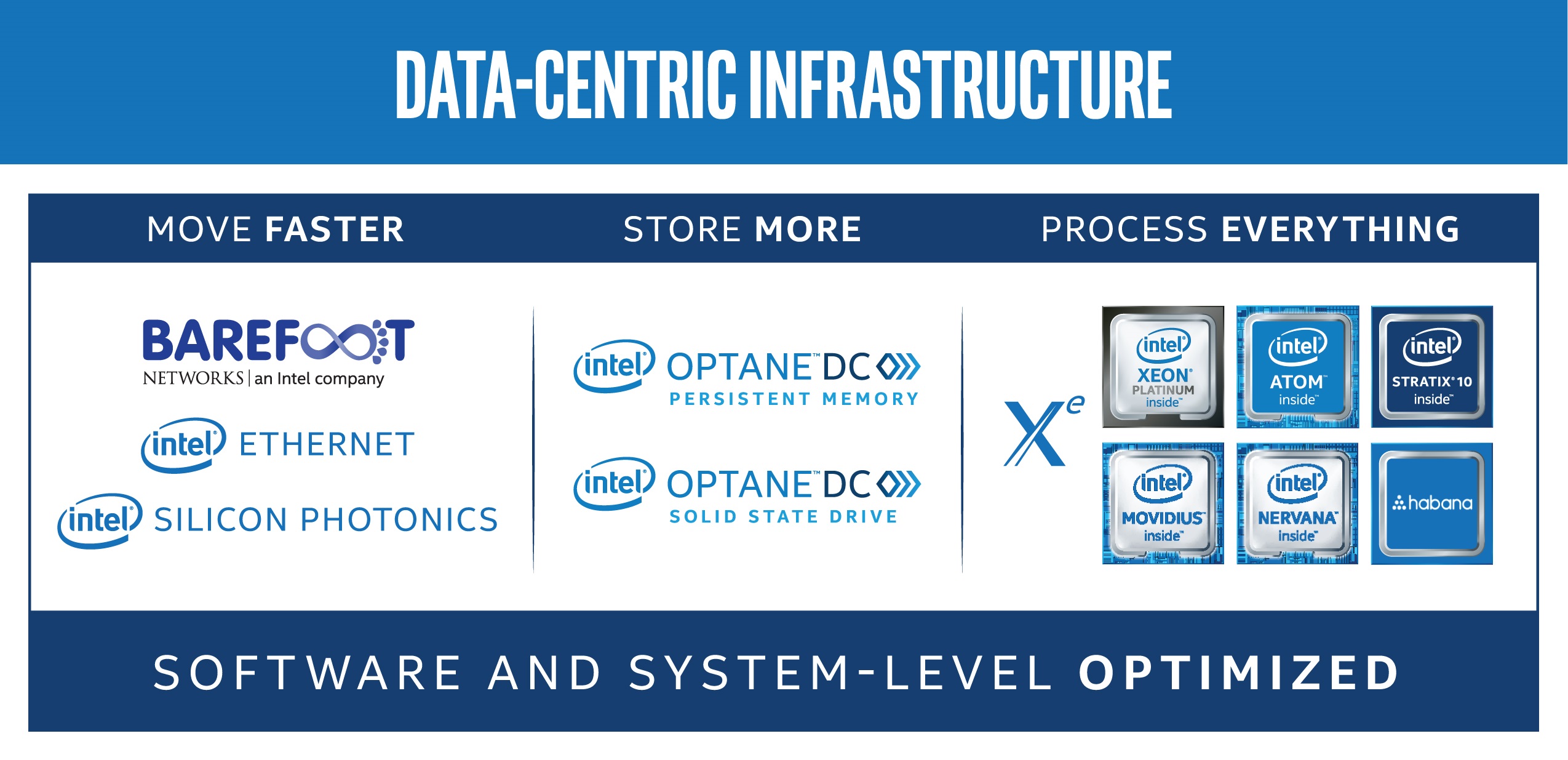

Product leadership is defined by our ability to optimize across six engineering pillars: process technology and packaging, architecture, memory, interconnect, security, and software. With these six pillars, we are accelerating product innovation with a focus on xPU platforms uniquely able to serve diverse new workload opportunities (e.g., CPU, GPU, AI accelerator and FPGA). These innovation efforts will extend Intel’s opportunities to deliver products beyond the CPU that will contribute to the success of our customers. |  |

LEAD TECHNOLOGY INFLECTIONS |

Our strategic intent is to lead in key technology inflections that are fundamentally changing computing and communications. The most important drivers of change we see today are AI, the transformation of networks spearheaded by the transition to 5G, and the rise of the intelligent edge. We see a future where Intel® technologies enable our customers to move faster, store more, and process everything—from large complex applications in the cloud, to autonomous cars and small low-power devices on the edge.

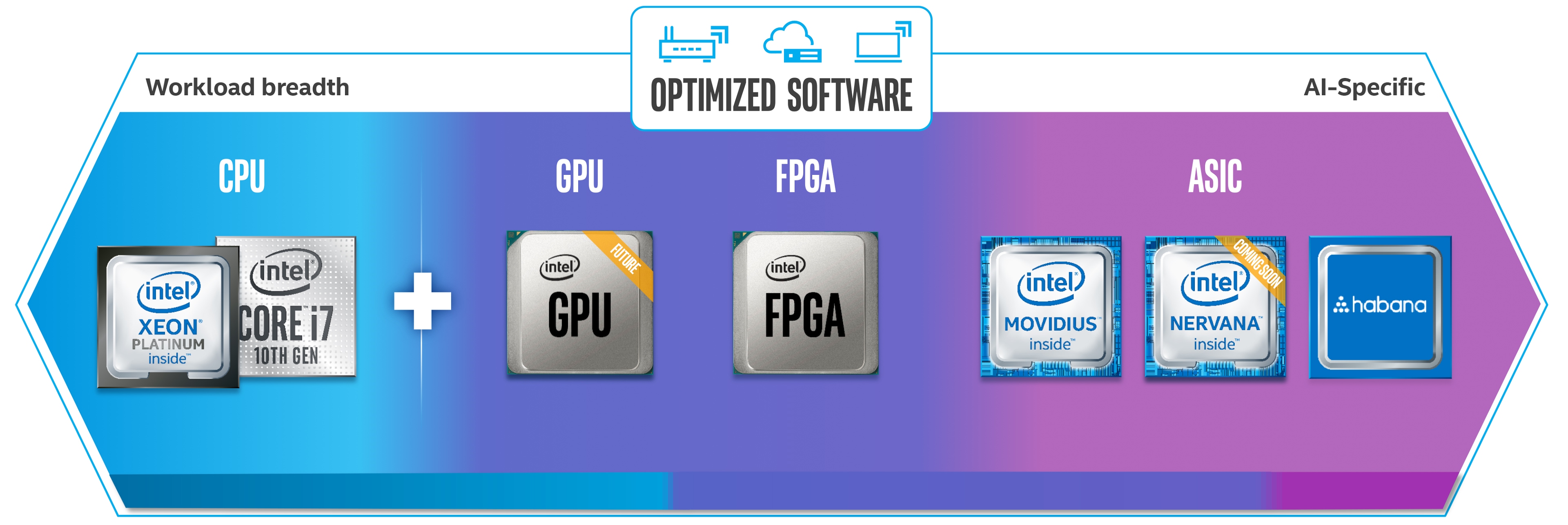

AI helps our customers make sense of big data to unleash its potential. We offer a combination of hardware and software technologies that deliver broad capabilities to support computing, storage, transmission, and tuning in AI. We have taken a multi-architecture approach to AI hardware. Intel® Xeon® processors provide a foundation for analytics and AI, and software like the OpenVINO™ toolkit significantly simplifies the deployment of solutions. Intel® FPGAs allow customers to gain access to leading AI inferencing performance for their models. Similarly, the Intel® Nervana™ Neural Network Processors and Intel® Movidius™ Myriad™ VPUs are purpose-built for AI and support diverse approaches for innovation in a wide range of applications, from healthcare to autonomous driving to facial recognition. Habana's Gaudi* AI training Processor and Goya* AI Inference Processor offer an easy-to-program development environment to help customers deploy and differentiate their solutions as AI workloads continue to evolve with growing demands on compute, memory, and connectivity.

| FUNDAMENTALS OF OUR BUSINESS | 6 | |

We are optimistic about the opportunity presented to us by the 5G transition and the cloudification1 of the network. 5G connectivity will transform industries from all business sectors and it continues to be a strategic priority across Intel. We are collaborating with ecosystem and vertical industry partners to define, prototype, test, and deliver 5G standards and solutions, and our team has developed products designed to support 5G network infrastructure and a valuable IP portfolio. With our exit from the 5G smartphone modem business, our 5G efforts are now focused on network infrastructure and other data-centric opportunities.

We provide the automobile industry’s leading solution for ADAS and we continue to build on that leadership in pursuit of higher levels of autonomy, developing Road Experience Management for real-time crowdsourced mapping, and the Responsibility Sensitive Safety model for autonomous vehicle safety. As the data explosion creates new opportunities, we continue to assess other service models that will leverage our product leadership and deep technical expertise to drive more value to our customers.

BE THE LEADING END-TO-END PLATFORM PROVIDER FOR THE NEW DATA WORLD | ||||

Customers look to Intel for our end-to-end capability to deliver solutions that enable customers to move faster, store more, and process everything. We continue to make investments in optimizing our Intel® Xeon® processors in response to our customers’ need for high-performance computing. We continue to develop innovative memory and storage solutions, including Intel® QLC 3D NAND Technology and Intel® Optane™ memory, to provide data center products that are optimized to deliver world-class performance and drive lower total cost of ownership for cloud workloads. Our advancements in FPGAs enable efficient management of the changing demands of next-generation data centers and accelerate the performance of emerging applications. |  | |||

RELENTLESS FOCUS ON OPERATIONAL EXCELLENCE AND EFFICIENCY | ||||

Underlying our transformation to a data-centric company is a relentless focus on operational excellence and efficiency. This focus includes the elimination of lower growth investments and activities, and the simplification and automation of routine processes and activities. These efforts also extend to our product design processes, where we are striving to reduce the complexity of our designs to improve our efficiency and enhance quality. | ||||

These improvements enable us to achieve scale in our core operations, providing a stable and cost-effective platform to support additional investments in the design, development, and delivery of new products. Operational excellence helps us fund the expansion of our TAM through big-bet investments. | ||||

CONTINUE TO HIRE, DEVELOP, AND RETAIN THE BEST, MOST DIVERSE AND INCLUSIVE TALENT | |

At the core of our organization are highly skilled, diverse, and talented people capable of accelerating as one team in everything we do. We are proud of our past and inspired by how our employees are rising to the challenge to evolve our culture. Inclusion is the foundation of this evolution and runs through each of our culture attributes. These attributes reinforce: | |

● | Customer Obsessed: Our customer’s success is our success. We listen, learn, and anticipate our customers’ needs to deliver on their ambitions. |

● | One Intel: We are stronger together and commit to team over individual success. |

● | Fearless: We are bold and innovative. We take risks, fail fast, and learn from mistakes. |

● | Truth and Transparency: We are committed to being open and honest while bringing clarity to complex challenges. |

● | Inclusion: We strive to build a culture of belonging and welcome differences, knowing it makes us better. |

Our evolution is a multi-year journey, and one that requires new and different thinking, actions, systems, and processes to ensure that our employees are equipped to innovate for a world where all data needs to be processed, moved, stored, and analyzed. | |

1 | Intel's definition is included in "Key Terms" within the Financial Statements and Supplemental Details. |

| FUNDAMENTALS OF OUR BUSINESS | 7 | |

OUR CAPITAL |

We deploy various forms of capital to execute our strategy in a way that seeks to reflect our corporate values, help our customers succeed, and create value for our stakeholders. |

CAPITAL | STRATEGY | VALUE |

FINANCIAL | ||

| Leverage cash flow to invest in ourselves and grow our capabilities, supplement and strengthen our capabilities through acquisitions and strategic investments, and provide returns to stockholders. | We strategically invest financial capital to create long-term value and provide returns to our stockholders in the form of dividends and buybacks. |

INTELLECTUAL | ||

| Invest significantly in R&D and IP to ensure our process and product technologies are competitive in our strategic pursuit of making the world’s best semiconductors and realizing data-centric opportunities. | We develop IP for our platforms to enable next-generation products, create synergies across our businesses, provide a higher return as we expand into new markets, and establish and support our brands. |

MANUFACTURING | ||

| Invest timely and at a level sufficient to meet customer demand for current technologies and prepare for future technologies. | Our manufacturing scope and scale enables innovations to provide our customers and consumers with a broad range of leading-edge products. |

HUMAN | ||

| Develop the talent needed to remain at the forefront of innovation and create a diverse, inclusive, and safe workplace. | We attract and retain talented employees who enable the development of solutions and enhance the intellectual and manufacturing capital critical to helping our customers win the technology inflections of the future. |

SOCIAL AND RELATIONSHIP | ||

| Build trusted relationships for both Intel and our stakeholders, including employees, suppliers, customers, local communities, and governments. | We collaborate with stakeholders on programs to empower underserved communities through education and technology, and on initiatives to advance accountability and capabilities across our global supply chain, including accountability for the respect of human rights. |

NATURAL | ||

| Continually strive to reduce our environmental footprint through efficient and responsible use of natural resources and materials used to create our products. | Our proactive efforts help us mitigate climate and water impacts, achieve efficiencies and lower costs, and position us to respond to the expectations of our stakeholders. |

| FUNDAMENTALS OF OUR BUSINESS | 8 | |

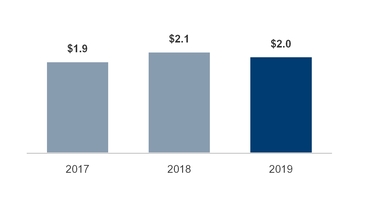

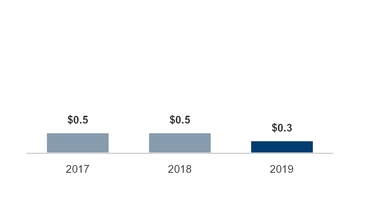

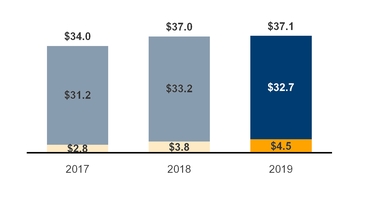

| FINANCIAL CAPITAL |

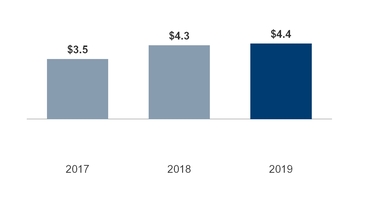

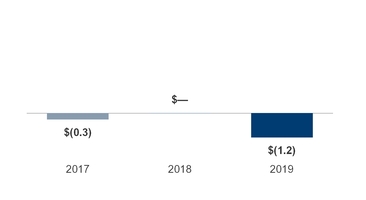

Our financial capital allocation strategy focuses on building stockholder value. We have returned approximately 90% of free cash flow to investors over the past five years and expect to return approximately 100% in 2020.

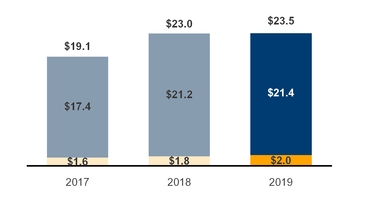

CASH FROM OPERATING ACTIVITIES $B |

■ Capital Investment | ■ Free Cash Flow1 | |

OUR FINANCIAL CAPITAL ALLOCATION DECISIONS ARE DRIVEN BY THREE PRIORITIES |

INVEST IN THE BUSINESS | ACQUIRE AND INTEGRATE | RETURN CASH TO STOCKHOLDERS | ||||||

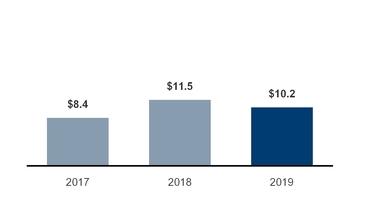

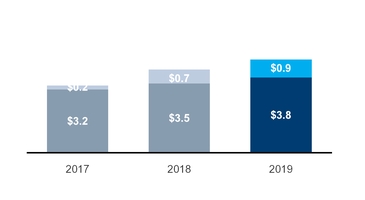

Our first allocation priority is to invest in R&D and capital spending to strengthen our competitive position. We shifted our R&D focus as we began a transformation to a data-centric company, while efficiently maintaining our investment at approximately 20% of revenue. We invested record levels of capital in logic (primarily platform wafer manufacturing) during the last two years to expand our capacity. With that investment, we increased our 14nm wafer capacity while also ramping 10nm production. We expect to further increase our PC client supply on both process nodes in 2020. | Our second allocation priority is to invest in companies around the world that will complement our strategic objectives and stimulate growth of data-centric opportunities. We look for acquisitions that leverage and strengthen our capital and R&D investments. In 2019, we completed various acquisitions, including Habana Labs and Barefoot Networks, to expand our product offerings and the markets we serve. We take action when investments do not meet our criteria, and in 2019 we divested the majority of our 5G smartphone modem business for this reason. | Our third allocation priority is to return cash to stockholders. We achieve this through our dividend and share repurchase programs. During 2019, we paid $5.6 billion in dividends and repurchased $13.6 billion in shares, up from 2018. In October 2019, we announced that we expect to repurchase $20.0 billion in shares over the next 15 to 18 months. Our approach has reduced diluted shares outstanding over time. | ||||||

Dividends Per Share | Diluted Shares Outstanding (In Millions) | |||||||

2019 | $1.26 | 8% CAGR | 4,473 | |||||

2018 | $1.20 | 4,701 | ||||||

2017 | $1.0775 | 4,835 | ||||||

R&D AND CAPITAL INVESTMENTS $B | ACQUISITIONS | CASH TO STOCKHOLDERS $B | |||

■ R&D | ■ Logic | ■ Memory | — # of Acquisitions | ■ Total Spent $B | ■ Buyback | ■ Dividend | |||

1 | See "Non-GAAP Financial Measures" within MD&A. |

| FUNDAMENTALS OF OUR BUSINESS | Our Capital | 9 |

| INTELLECTUAL CAPITAL |

RESEARCH AND DEVELOPMENT

R&D is a critical factor in achieving our strategic objectives to make the world's best semiconductors, to lead technology inflections, and to provide leading end-to-end platform solutions. Successful R&D efforts can lead to new products and technologies or improvements to existing ones, which we seek to protect through our IP rights. We may augment our R&D initiatives through the following methods: acquiring or investing in companies, entering into R&D agreements, and directly purchasing or licensing technology.

PRODUCT TECHNOLOGY

Architecture. We are designing products for four major computing architectures—CPU, GPU, AI accelerator, and FPGA products—as we move toward a model of providing multiple "xPU" compute platforms for a more diverse era of computing. We shipped the 10th generation Intel® CoreTM processors with our next-generation CPU microarchitecture, which has architectural extensions designed for special-purpose computing tasks such as AI and cryptography, among other features. These processors also include the next generation of graphics microarchitecture, with performance and feature upgrades. We also continue to make progress on the development of our first discrete GPU.

Every year we make significant investments in R&D and we have intensified our focus on six engineering pillars to advance our product capabilities. Our objective is to improve user experiences and value through advances in performance, power, cost, connectivity, security, form factor, and other features with each new generation of products. We are also focused on reducing our design complexity to improve our efficiency, including a significant reduction of design rules for future process nodes. |  | |

Process. Development of next-generation manufacturing processes remains a critical and fundamental pillar. We announced that we are planning multiple waves of 10nm process, progressively increasing transistor performance. We also announced advances in our next-generation 2.5D (EMIB) and 3D (Foveros) packaging technology which will enable us to mix and match chips made on different processes into a single SiP, enabling new design flexibility and new device form factors. The Intel 10nm product era is underway, as we began shipping our new 10th generation Intel® CoreTM processors, previously referred to as Ice Lake. | ||

Six Pillars of Product Leadership | ||

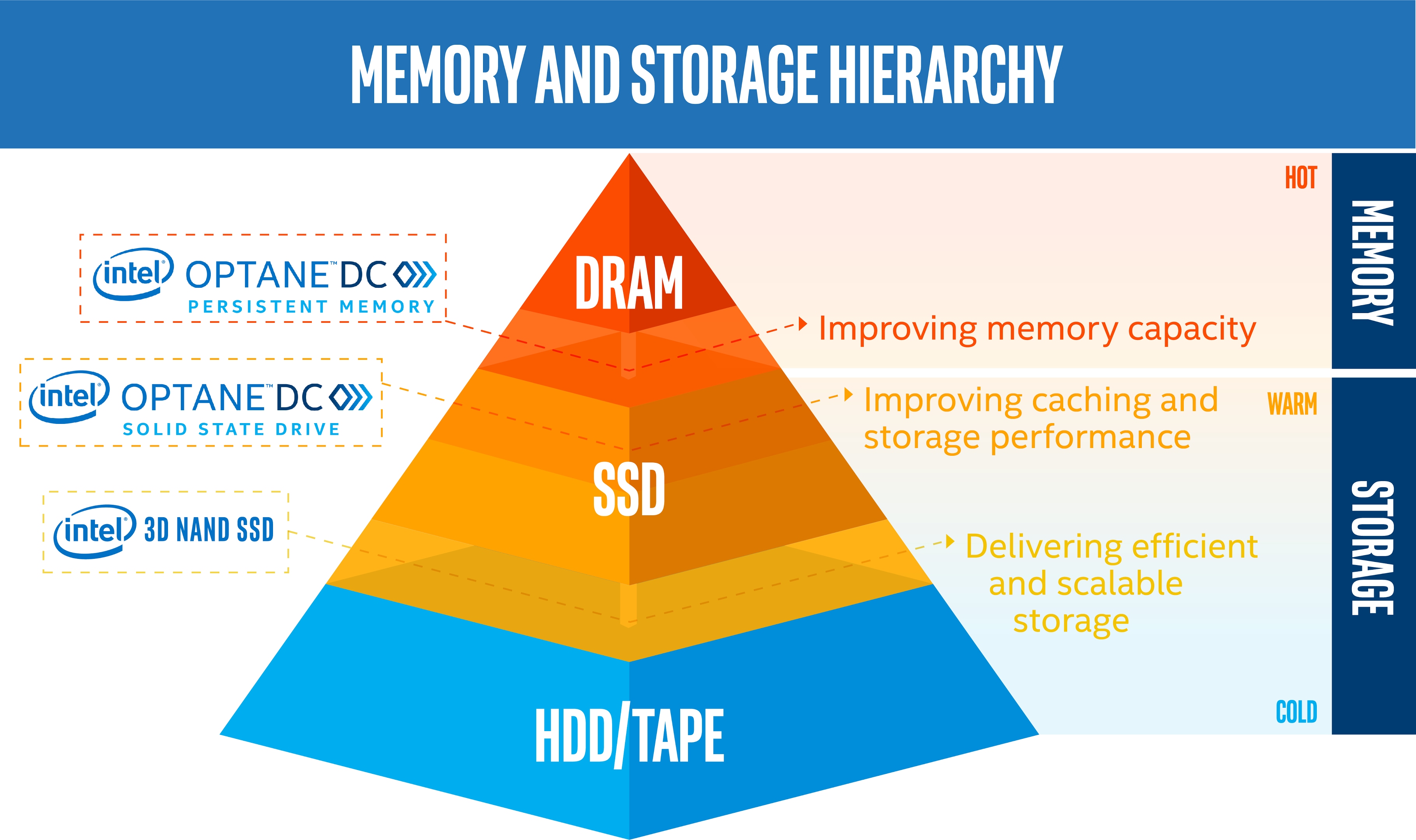

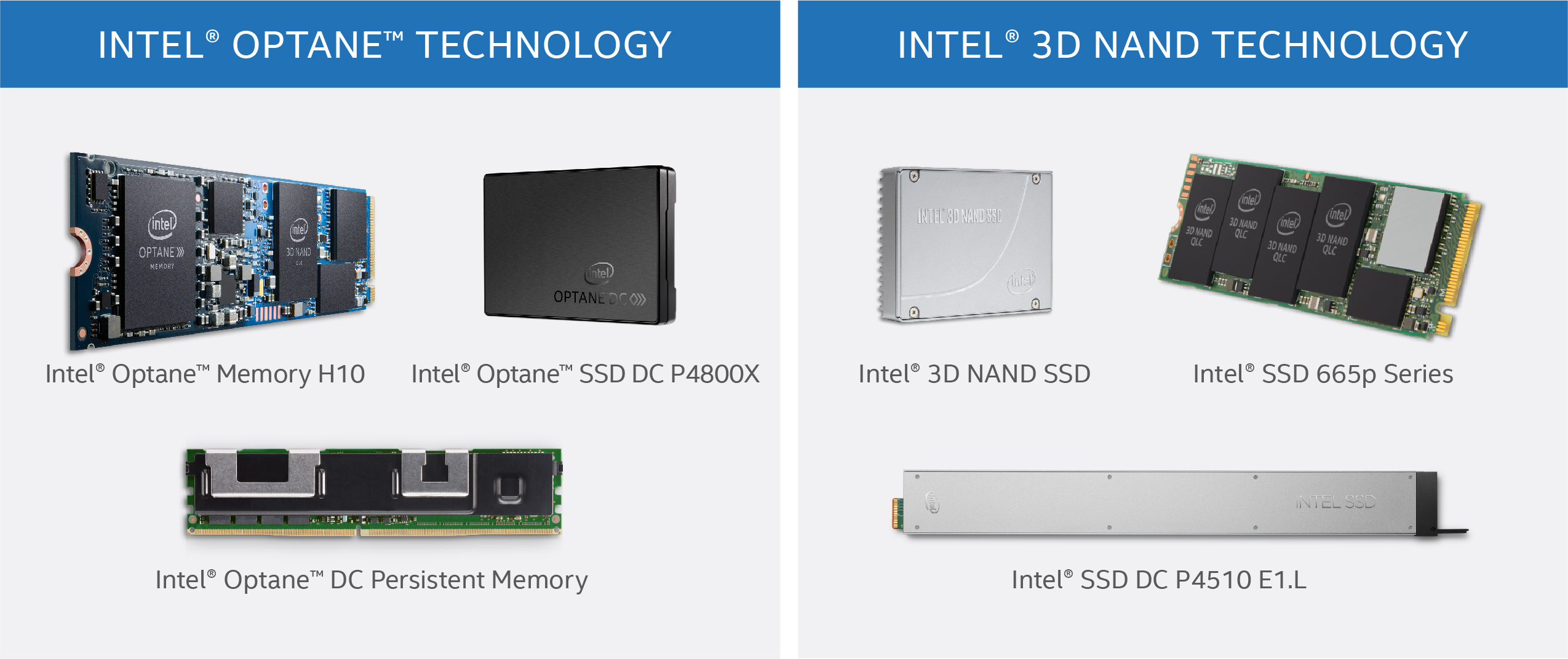

Memory. With our Intel® 3D NAND technology and Intel® Optane™ technology, we are developing products to disrupt the memory and storage hierarchy. The 4th generation of Intel®-based SSDs are scheduled to launch in 2020 with 144-layer QLC memory technology. These SSDs are also Intel’s first NAND memory technology created independently by Intel since the conclusion of our partnership with Micron Technology, Inc. (Micron). The 2nd generation Intel® OptaneTM SSDs for data centers are scheduled to start shipping samples in 2020, and are designed to deliver three times the throughput while reducing application latency by four times. In addition, the second-generation Intel® OptaneTM DC persistent memory is expected to achieve PRQ in 2020, and is designed for use with our future Intel® Xeon® CPUs.

Interconnect. We have a broad portfolio of interconnect solutions, ranging from silicon to the data center to wireless. Our silicon photonics technology integrates lasers into silicon to create high-speed optical connections that can help remove networking bottlenecks in the data center. We announced two initiatives to help influence the industry—USB4 and CXL. USB4 advances the speed and capability for interconnect in client platforms. CXL, an open interconnect technology, creates a high-speed, low latency interconnect between the CPU and accelerators, such as GPUs, FPGAs, and networking.

Security. We continue to make significant investments in security technologies. We created the Intel Security Architecture and Technologies Group to serve as a center for security architecture across our products to design world-class product security architecture for the years ahead.

Software. The performance potential of our hardware products is unlocked with software. Our vision is to unify our software abstractions across all our xPU platforms. We are developing a project called oneAPI to simplify programming for developers across our CPU, GPU, FPGA, AI accelerator, and other accelerator products, providing a unified portfolio of developer tools for mapping software to the hardware that can best accelerate the code.

IP RIGHTS

We own and develop significant IP and related IP rights around the world that support our products, services, R&D, and other activities and assets. Our IP portfolio includes patents, copyrights, trade secrets, trademarks, mask work, and other rights. We actively seek to protect our global IP rights and to deter unauthorized use of our IP and other assets. For a detailed discussion of our IP rights, see "Intellectual Property Rights and Licensing" within Other Key Information.

| FUNDAMENTALS OF OUR BUSINESS | Our Capital | 10 |

| MANUFACTURING CAPITAL |

We are an IDM. Unlike many other semiconductor companies, we primarily design and manufacture our products in our own manufacturing facilities, and we see our in-house manufacturing as an important advantage. We continue to develop new generations of manufacturing process technology as we seek to realize the benefits from Moore’s Law. Realizing Moore’s Law results in economic benefits as we are able to either reduce a chip's cost as we shrink its size, or increase functionality and performance of a chip while maintaining the same cost with higher density. This makes possible the innovation of new products with higher performance while balancing power efficiency, cost, and size to meet customers' needs. Our ability to optimize and apply our manufacturing expertise to deliver more advanced, differentiated products is foundational to our current and future success.

We are on track to deliver our first 7nm-based product, a data center-focused discrete GPU, at the end of 2021. We are approaching next-generation process nodes with a focus on striking an optimal balance between schedule, performance, power, and cost and will continue to drive intra-node advancement.

We improved our 10nm factory production, yield, and volume during 2019, and launched 10th-generation Intel® CoreTM processors, our first 10nm volume product, and Intel® AgilexTM, our first 10nm FPGA. We expect to deliver initial production shipments of our first 10nm-based Intel® Xeon® Scalable product, Ice Lake, in the latter part of 2020. |  | "Our technology and innovation pipeline is as full and as strong as it’s ever been. By embracing our ecosystems and delivering new capability on a predictable cadence, we will continue to drive Moore’s Law forward and create compelling products for our customers.” —Mike Mayberry, Senior Vice President, Chief Technology Officer and General Manager of Technology Development | |

NETWORK AND SUPPLY CHAIN

We previously announced multiple manufacturing site expansions with multi-year construction activities that began in 2019. In addition to expanding our own manufacturing capability, we are increasing our use of foundries to enable our differentiated manufacturing to produce more CPU products. We use third-party foundries to manufacture wafers for certain components and leverage subcontractors to augment capacity to perform assembly and test in addition to our in-house manufacturing, primarily for chipsets and adjacent products. As we considered the estimated $300 billion TAM1 opportunity ahead of us, it was imperative that we prepare our global manufacturing network to be responsive to changes in demand. However, despite increasing 14nm wafer capacity, we did not see a commensurate increase in client CPU unit volume as wafer capacity was largely consumed by increases in modem and chipset volumes, and unit die sizes. Our focus on capacity expansion and meeting customer expectations is critical as we move into 2020.

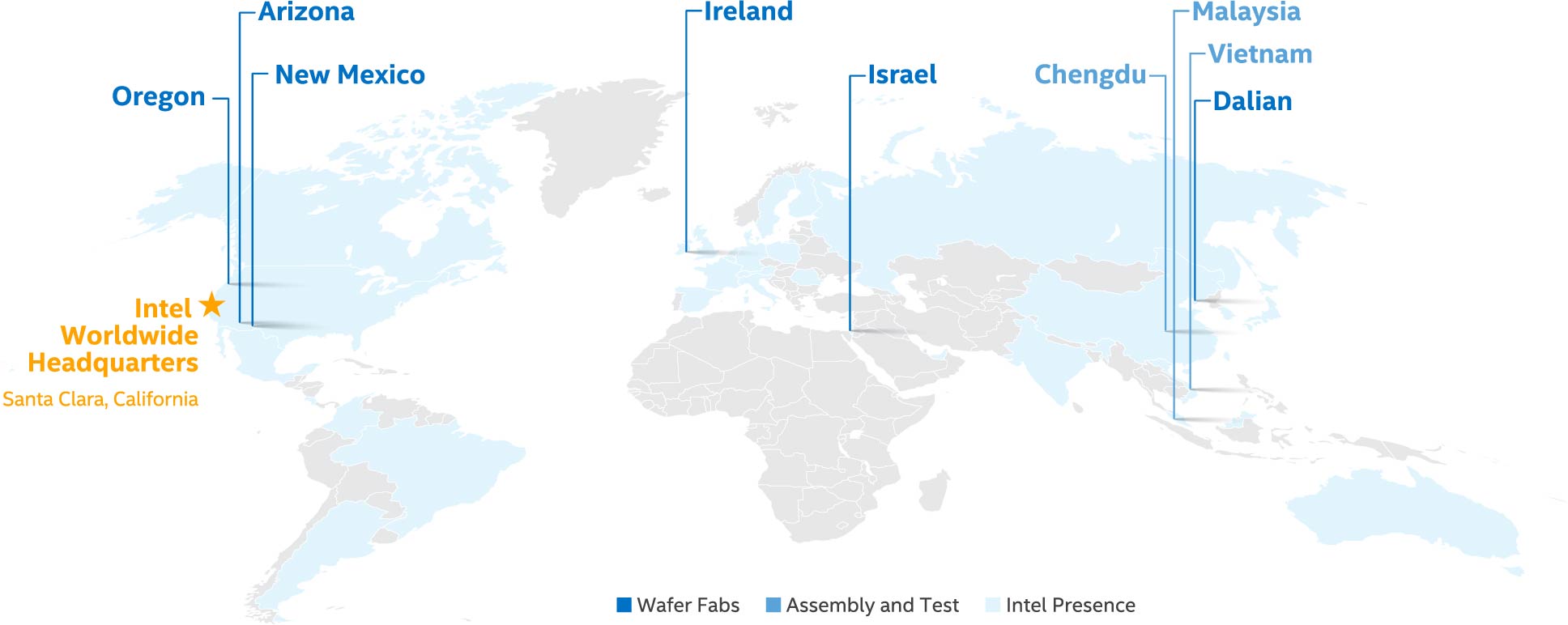

We have nine manufacturing sites—six are wafer fabrication and three are assembly/test facilities. The map marks our manufacturing sites and the countries where we have a significant R&D or sales and marketing presence. The majority of our logic wafer manufacturing is conducted in the U.S. We incur factory start-up costs as we ramp facilities for new process technologies. We ramped the 10nm process node in Oregon and Israel in 2019, and began production in Arizona in our 2020 fiscal year. We also expanded our memory facilities in Dalian, China. |  |

Our manufacturing facilities are primarily used for silicon wafer manufacturing of our platform and memory products. These facilities are built following a “copy exactly” methodology, whereby new process technologies are transferred identically from a central development fab to each manufacturing facility. This enables fast ramp of the operation as well as better quality control. These wafer fabs operate in a network of manufacturing facilities integrated as one factory to provide the most flexible supply capacity, allowing us to better analyze our production costs and adapt to changes in capacity needs.

In 2019, we ramped 96-layer 3D NAND technology and prepared to begin manufacturing our 144-layer 3D NAND technology in 2020 in our facility in Dalian, China. The next generation of Intel® Optane™ technology and SSDs are being developed in New Mexico following the sale of our non-controlling interest in IMFT to Micron on October 31, 2019. We will continue to purchase product manufactured by Micron at the IMFT facility under established supply agreements.

1 Source: Intel calculated 2024 TAM derived from industry analyst reports.

| FUNDAMENTALS OF OUR BUSINESS | Our Capital | 11 |

| HUMAN CAPITAL |

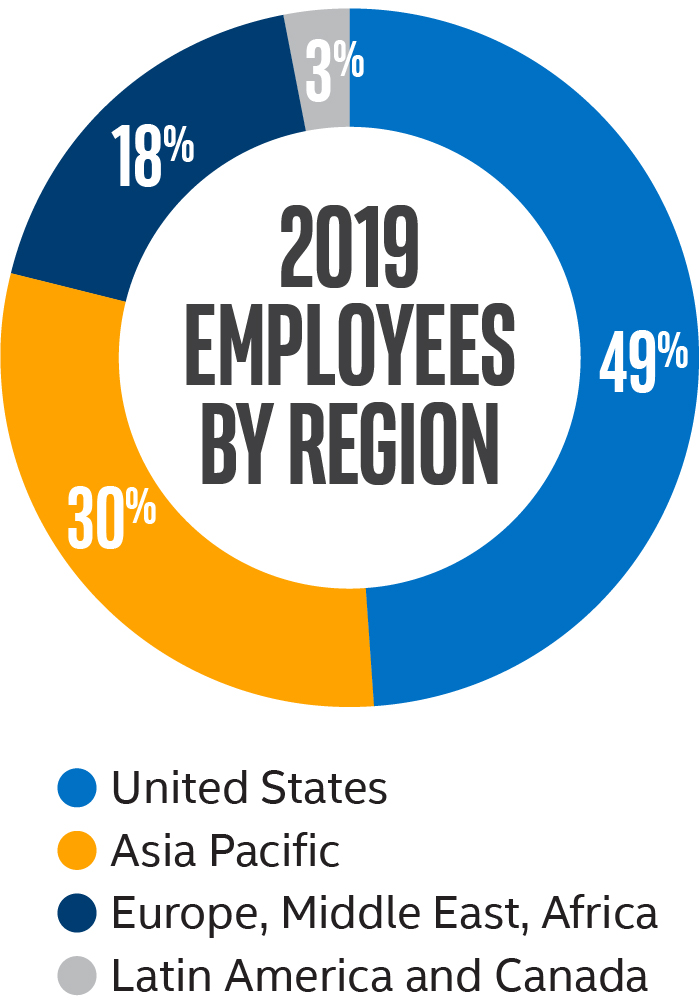

Evolving our culture is critical to delivering on our growth strategy and for continuing to attract and retain top talent needed to support our transformation to a data-centric company. We have an amazing legacy of innovation and a powerful culture, yet our ambitions have grown. Together, we are evolving our culture to build an even brighter future. Our global workforce of 110,800 is highly educated, with approximately 90% of our people working in technical roles. We invest in creating a diverse, inclusive, and safe work environment where our employees can deliver their workplace best every day. | ||

All employees are responsible for upholding the Intel Values, Intel Code of Conduct, and Intel Global Human Rights Principles, which form the foundation of our policies and practices. For over a decade, we have tracked and publicly reported on key human capital metrics, including workforce demographics, diversity and inclusion data, turnover, and training data. |  | "Tapping into the richness of our diverse workforce is key to driving future growth. Intel will continue to be transparent about our progress and our challenges, so we can partner with our customers and ecosystem to find better solutions together." —Sandra Rivera, Executive Vice President and Chief People Officer |

DIVERSITY AND INCLUSION |  |

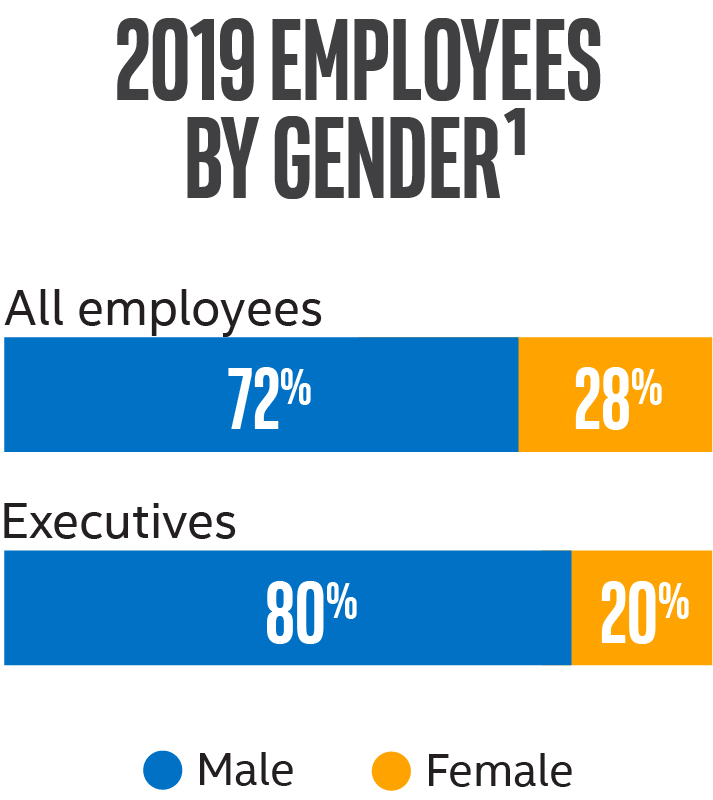

To shape the future of technology, we must be representative of that future. A diverse and inclusive workforce is a business imperative and key to our long-term success. We committed $300 million to advance diversity and inclusion in our workforce and in the technology industry. We achieved our goal of full representation in our U.S. workforce two years ahead of schedule, meaning our workforce now reflects the percentage of women and underrepresented minorities available in the skilled labor market in the U.S. This achievement was the result of a comprehensive strategy that considered hiring, retention, and progression. Though we are proud of what we have accomplished to advance diversity in our workforce, we still have work to do, including beyond the walls of Intel. We took action by joining 11 other companies to fund an initiative to double the number of women of color graduating with computing degrees in the U.S. by 2025. We also continue to look for and implement partnerships and programs to increase retention and advancement of women and underrepresented populations within our workplace. The breakout of employees by gender provides our current global gender diversity. | |

COMPENSATION AND BENEFITS |  |

We strive to provide pay, benefits, and services that help meet the varying needs of our employees. Our generous total rewards package includes market-competitive pay, broad-based stock grants and bonuses, an Employee Stock Purchase Plan, healthcare and retirement benefits, paid time off and family leave, parent reintegration, fertility assistance, flexible work schedules, sabbaticals, and on-site services. In 2019, we announced that we achieved gender pay equity globally by closing the gap in average pay between employees of different genders in the same or similar roles after accounting for legitimate business factors that can explain differences, such as performance, time at grade level, and tenure. We also continued to advance transparency in our pay and representation data by publicly releasing our 2017 and 2018 EEO-1 survey pay data mandated by the U.S. Equal Employment Opportunity Commission. The results reflected representation gaps and point to work that lies ahead. However, due to our diversity and inclusion efforts, there is promising growth of our junior female and underrepresented talent from which our future leadership will be drawn. Our challenge now is to create an environment that better helps our female and underrepresented employees develop and progress in their careers, while also ensuring we are expanding our hiring and retention of diverse talent at more senior, higher-paying positions. | |

1 | Executives refers to salary grades 12+ and equivalent grades. While we present male and female, we acknowledge this is not fully encompassing of all gender identities. |

| FUNDAMENTALS OF OUR BUSINESS | Our Capital | 12 |

GROWTH AND DEVELOPMENT |  |

We invest significant resources to develop the talent needed to remain at the forefront of innovation and make Intel an employer of choice. We deliver training annually and provide rotational assignment opportunities. We launched a new performance management system to support our culture evolution and increase focus on continuous learning and development. Over the past five years, our undesired voluntary turnover rate has been at or below 5%. | |

COMMUNICATION AND ENGAGEMENT | |

Our success depends on employees understanding how their work contributes to the company’s overall strategy. We use a variety of channels to facilitate open and direct communication, including open forums with executives; employee experience surveys; and engagement through more than 30 different employee resource groups, including the Women at Intel Network, the Network of Intel African American Employees, the Intel Latino Network, and others. | |

HEALTH, SAFETY, AND WELLNESS | |

We are committed to the safety of our employees, customers, and communities, from operations to product development to supplier partnerships. Our ultimate goal is to achieve zero serious injuries through continued investment in and focus on our core safety programs and injury-reduction initiatives. We provide access to a variety of innovative, flexible, and convenient health and wellness programs, including on-site health centers. | |

| SOCIAL AND RELATIONSHIP CAPITAL |

We are committed to developing trusted relationships, giving back to our communities, and engaging in corporate responsibility and sustainability initiatives. Collaboration with stakeholders and investments in social impact initiatives, like the United Nations Sustainable Development Goals, led to our reputation as a leading corporate citizen and creates value in the form of consistent stakeholder support.

ECONOMIC, SOCIAL, AND HUMAN RIGHTS IMPACT

The health of our company and local economies depends on continued investments in innovation. We provide high-skill, high-paying jobs around the world. Many of these are manufacturing and R&D jobs located in our own domestic and international factories. We also impact economies through our R&D ecosystem spending, sourcing activities, consumer spending by our employees, and tax revenue. We make sizable capital investments and provide leadership in public-private partnerships to spur economic growth and innovation.

We are at the forefront of new technologies that are increasingly being used to empower individuals, companies, and governments around the world to solve major societal challenges. Simultaneously, we are empowering people through education and advancing social impact initiatives to create new career pathways into the technology industry, helping us build trust with key external stakeholders and support the interests of our employees. Our employees actively share their expertise and skills through volunteer initiatives, and contributed 1 million hours of service in the communities where we operate in 2019.

We are committed to maintaining and improving processes to avoid human rights violations related to our operations, supply chain, and products. While we do not always know nor can we control what products our customers create or the applications end-users may develop, we do not support or tolerate our products being used to violate human rights. Where we become aware of a concern that Intel products are being used by a business partner in connection with abuses of human rights, we will restrict or cease business with the third party until and unless we have high confidence that Intel’s products are not being used to violate human rights.

SUPPLY CHAIN RESPONSIBILITY

We have robust programs to educate and engage suppliers that support our global manufacturing operations to drive responsible and sustainable practices throughout the supply chain. Actively managing our supply chain creates business value for Intel and our customers by helping to reduce risk, improve product quality, achieve environmental and social goals, and raise the overall performance of our suppliers. Over the past five years, we completed more than 600 supplier audits using the Responsible Business Alliance Code of Conduct standard. We actively collaborate with other companies and lead industry initiatives on key issues such as advancing responsible minerals sourcing, improving transparency around climate and water impacts in the global electronics supply chain, and addressing risks of forced and bonded labor. Our commitment to building a diverse and inclusive workforce extends to the expectations we set for our suppliers—a diverse supply chain supports greater innovation and value for our business. We continue working toward our 2020 goal of reaching $1.0 billion in annual spending with diverse-owned suppliers. We also announced the "Intel Rule" to help improve diversity in the legal profession: Beginning in 2021, we will not retain or use outside law firms in the U.S. that are average or below average on diversity for their equity partners. We are applying a similar rule to firms used by our tax department, including non-legal firms.

| FUNDAMENTALS OF OUR BUSINESS | Our Capital | 13 |

| NATURAL CAPITAL | |||

Driving to the lowest environmental footprint possible helps us achieve efficiency, lower costs, and respond to the needs of our stakeholders. We invest in conservation projects and set company-wide environmental targets, seeking to drive reductions in greenhouse gas emissions, energy use, water use, and waste generation. We focus on building energy efficiency into our products to help our customers lower their own emissions and energy costs. We also collaborate with policymakers and other stakeholders to identify opportunities to apply technology to environmental challenges such as climate change and water conservation.

| "At Intel, we have long believed that to truly be a leader in manufacturing, we must also advance environmental sustainability and corporate responsibility. For more than two decades, our sustainability practices have enabled us to create significant value for our customers, investors, employees, and community stakeholders." —Ann Kelleher, Senior Vice President and General Manager of Manufacturing and Operations | |

CLIMATE AND ENERGY

We focus on reducing our own direct climate “footprint” and over the past two decades have reduced our direct emissions and electricity-generated emissions. Since 2012, we have invested more than $200 million in energy conservation projects in our global operations, resulting in cumulative savings of more than 4.5 billion kWh and cost savings of more than $500 million. In addition to conserving energy, we invest in green power and on-site alternative energy projects that provide power directly to our buildings and design all new buildings to LEED* standards. In 2019, we opened a LEED Platinum building in Israel with sensors that monitor lighting, temperature, ventilation, parking, and other building services and systems that enable and foster smart innovation. It also employs stormwater runoff collection and injection wells to avoid groundwater runoff. We also focus on increasing our “handprint”—the ways in which Intel technologies can help others reduce their footprints, including Internet of Things solutions that enable intelligence in machines, buildings, supply chains, and factories, and make electrical grids smarter, safer, and more efficient.

We are leveraging a leading framework developed by TCFD to communicate our approach to climate governance, strategy, risk management, and metrics and targets. In terms of governance and strategy, we follow an integrated approach to addressing climate change, with multiple teams responsible for managing climate-related activities, initiatives, and policies, including manufacturing and operations, government and public affairs, supply chain, and product teams. Strategies and progress toward goals are reviewed with senior executives and the Board’s Corporate Governance and Nominating Committee. We describe our overall risk management processes in our Proxy Statement, and we describe our climate-related risks and opportunities in our annual Corporate Responsibility Report, the Intel Climate Change Policy, and "Risk Factors" within this Form 10-K. Regarding metrics and goals, for two decades we have set aggressive GHG reduction goals, including our 2020 goal to reduce our direct GHG emissions by 10% on a per-unit basis from 2010 levels, which we are on track to achieve. Additional detail on our proactive efforts to address climate change is included in our Corporate Responsibility Report, as well as our CDP Climate Change Survey, both available on our website1.

WATER STEWARDSHIP

Water is essential to the semiconductor manufacturing process. We use ultrapure water to remove impurities from our silicon wafers, and we use industrial and reclaimed water to run our manufacturing facility systems. Over the last two decades, our sustainable water management efforts and partnerships have enabled us to conserve billions of gallons of water, and over the last decade we have returned approximately 80% of our water back to our communities. We continue to work toward our goal to restore 100% of our global water use by 2025, with more than 20 projects funded in collaboration with environmental and community partners through the end of 2019. We expect to restore approximately 1.5 billion gallons of water each year to local watersheds once these projects are complete.

CIRCULAR ECONOMY AND WASTE MANAGEMENT

We have long been committed to waste management, recycling, and circular economy strategies that enable the recovery and productive re-use of waste streams. We achieved our 2020 goal of recycling 90% of our non-hazardous waste ahead of schedule. We continue to work toward our 2020 goal of sending zero hazardous waste to landfills. Our aim is to continue to invest in reducing the amount of waste we generate while increasing the amount recycled and identifying re-use solutions that reduce costs and environmental impact.

1 The contents of our website and our Corporate Responsibility Report, Climate Change Policy, and CDP Climate Change Survey are referenced for general information only and are not incorporated by reference in this Form 10-K.

| FUNDAMENTALS OF OUR BUSINESS | Our Capital | 14 |

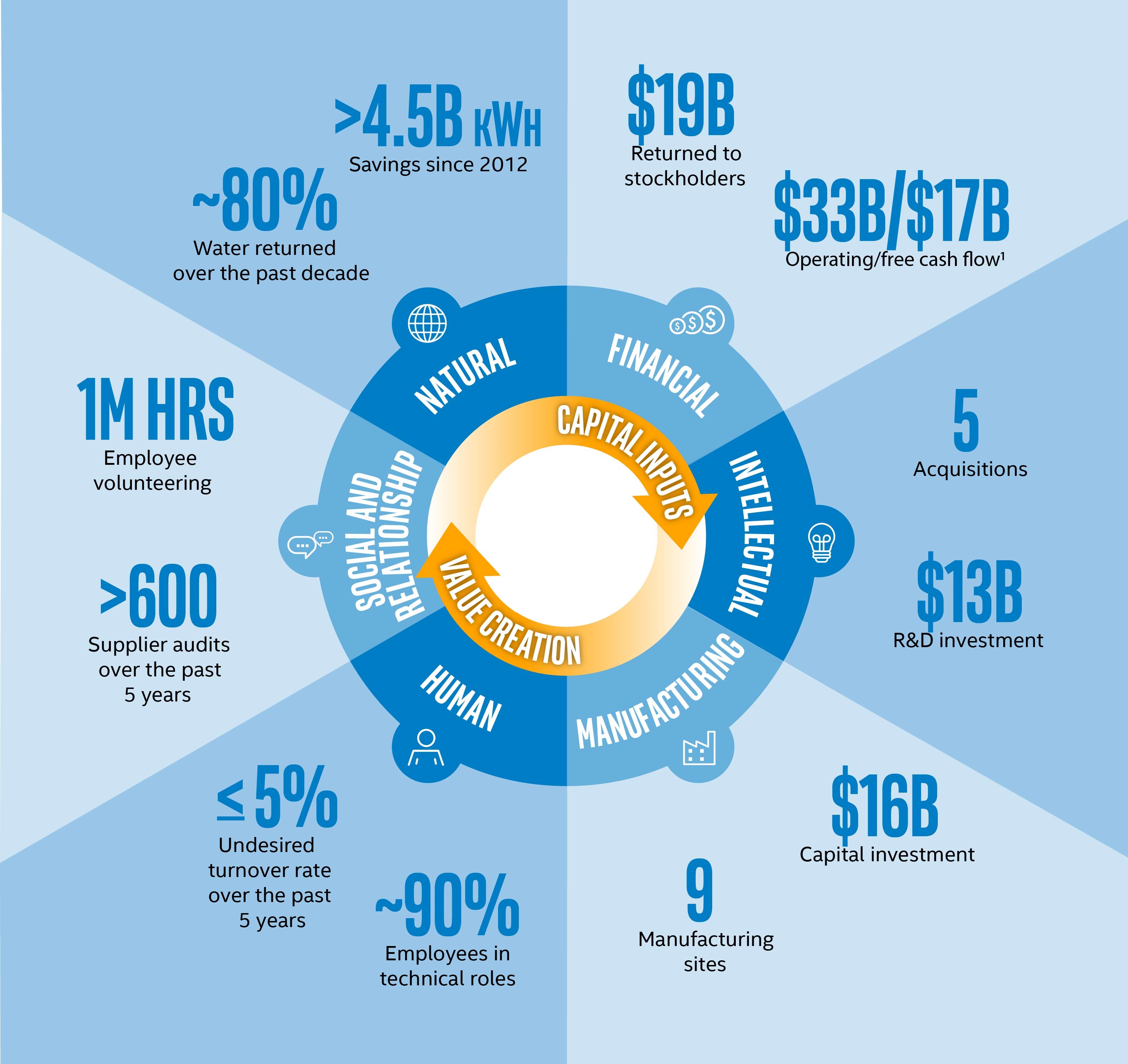

VALUE WE CREATE

Each of our six forms of capital plays a critical role in our long-term value creation. We consider numerous indicators in determining the success of our capital deployment in creating value. Highlights of value created up to and in 2019 are as follows:

|

1 | See "Non-GAAP Financial Measures" within MD&A. |

| FUNDAMENTALS OF OUR BUSINESS | Our Capital | 15 |

MANAGEMENT'S DISCUSSION AND ANALYSIS |

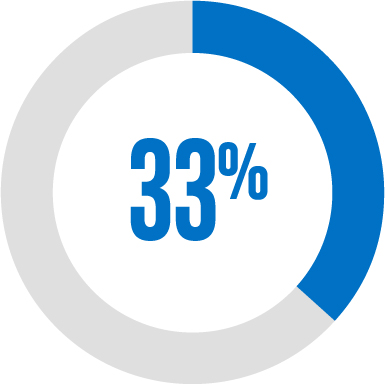

% INTEL REVENUE | KEY PRODUCTS AND MARKETS | HIGHLIGHTS | |||||

DCG |  | Includes workload-optimized platforms and related products designed for cloud, enterprise, and communication infrastructure market segments. | Revenue for our data-centric businesses was up 3% year over year. Growth in DCG, IOTG, Mobileye, and NSG was offset by decline in PSG. We introduced new data-centric products, such as the Intel® AgilexTM FPGA, 2nd generation Intel® Xeon® Scalable processor, and Intel® Optane™ DC persistent memory. In addition, Mobileye continued to secure new design wins at major U.S. and global automakers and announced plans to commercialize MaaS. | ||||

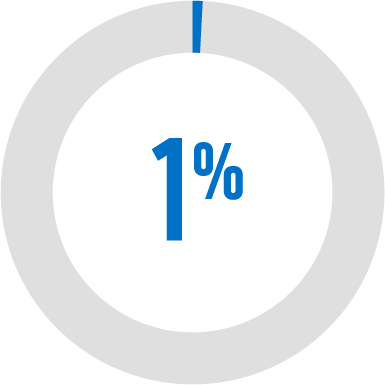

IOTG |  | Includes high-performance compute solutions for targeted verticals and embedded applications in market segments such as retail, industrial, smart infrastructure, and vision. | |||||

OPPORTUNITIES | |||||||

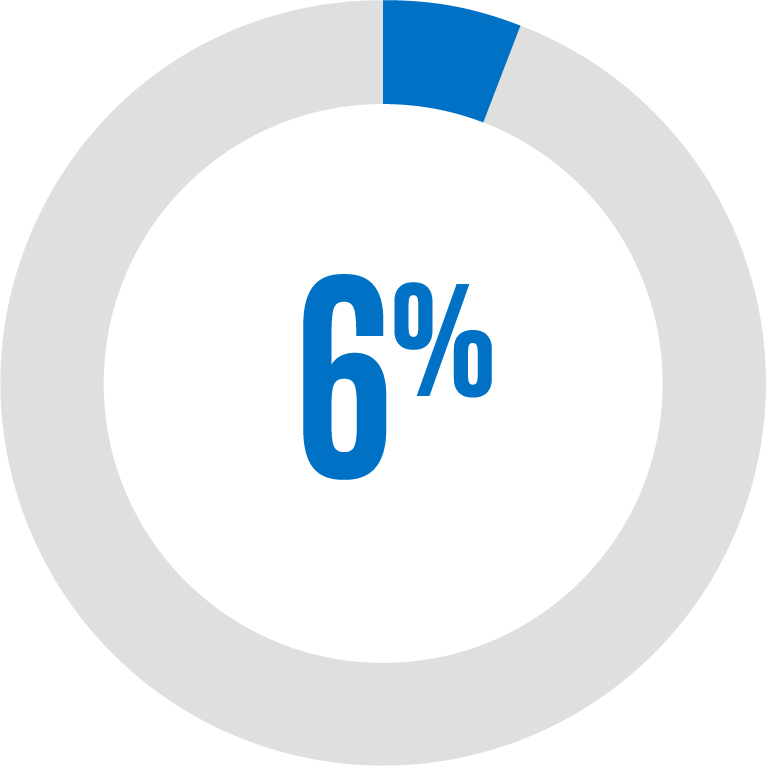

MOBILEYE |  | Includes development of computer vision and machine learning-based sensing, data analysis, localization, mapping, and driving policy technology for ADAS and autonomous driving. | We have expanded our data-centric TAM to approximately $230 billion1 with acquisitions and product innovations. Our broadened portfolio enables new opportunities for us and creates better synergistic value for our customers. For example, our product offerings for AI workloads reach from the cloud to the edge, and we are developing CPU, GPU, FPGA, and AI accelerator products to span inference and training AI workloads, while also pursuing ongoing software optimizations for AI. | ||||

NSG |  | Includes memory and storage products like Intel® Optane™ technology and Intel® 3D NAND technology, primarily used in SSDs. | |||||

CHALLENGES | |||||||

DCG growth slowed as major cloud service providers and enterprise OEMs worked through inventory after a historic platform refresh in 2018. As we enter 2020, we expect to face an increasingly competitive market. In addition, challenging market conditions resulted in margin compression on memory products. | |||||||

PSG |  | Includes programmable semiconductors, primarily FPGAs and structured ASICs, and related products for communications, cloud and enterprise, and embedded market segments. | |||||

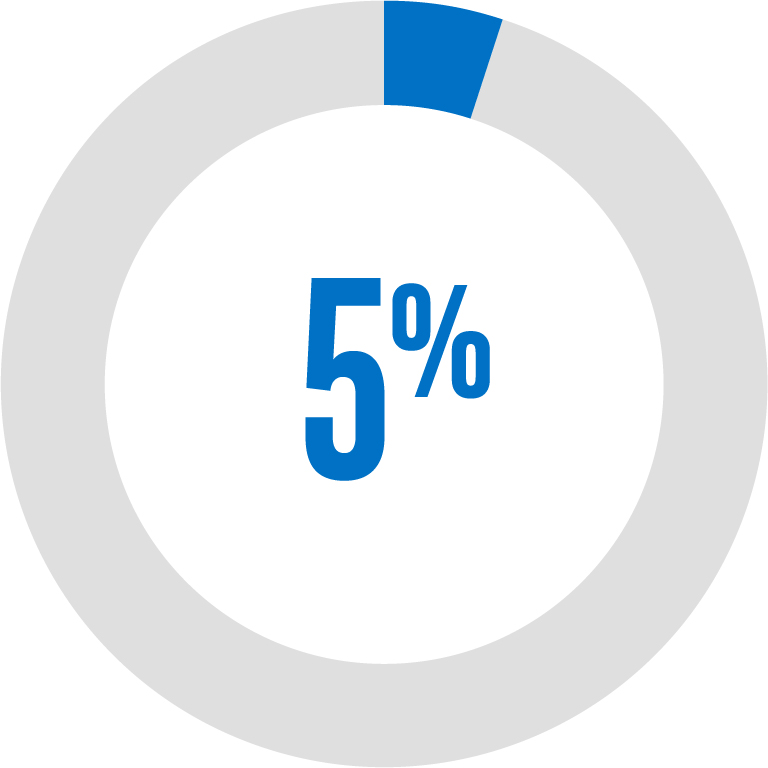

% INTEL REVENUE | KEY PRODUCTS AND MARKETS | ||||||

CCG |  | Includes platforms designed for end-user form factors, focusing on higher growth segments of 2-in-1, thin-and-light, commercial and gaming, and growing adjacencies such as connectivity, graphics, and memory. | |||||

HIGHLIGHTS | OPPORTUNITIES | CHALLENGES | |||||

Our PC-centric business revenue remained flat year over year. We began shipping our 10nm-based 10th generation Intel® CoreTM processors, previously referred to as Ice Lake. These processors feature a new core architecture and are expected to deliver increased graphics performance, AI, and new levels of integrated connectivity for thin-and-light laptops and 2-in-1s. We divested the majority of our 5G smartphone modem business to increase the focus of 5G efforts on the broader opportunity to modernize network and edge infrastructure while retaining critical IP and modem technology. | We are targeting an approximately $70 billion PC-centric revenue TAM1. This expanded portfolio includes markets such as connectivity, graphics, and memory, which enables new opportunities as we innovate through the platform. We launched Project Athena, a multi-year innovation program designed to deliver advanced laptops that meet ambitious key experience indicators in performance, responsiveness, battery life, form factor, and AI. | Our PC-centric business is operating in an increasingly competitive environment and we are focused on executing an annual cadence of leadership products. Strong demand across our product lines, combined with increased capacity consumed by offsetting factors, contributed to tight supply, particularly at the value end of the PC market. We are making additional investments in our manufacturing facilities and working with customers to align demand with available supply. | |||||

1 Source: Intel calculated 2024 TAM derived from industry analyst reports.

| MD&A | 16 | |

OUR PRODUCTS |

OUR PRODUCTS PROVIDE END-TO-END SOLUTIONS | |

WE HAVE A BROAD PRODUCT PORTFOLIO | |

Platform products: Our platform products can be a CPU and chipset, an SoC, or a multichip package, based on Intel® architecture that processes data and controls other devices in a system. These products are primarily used in solutions sold through CCG, DCG, and IOTG.

Adjacent products: Our non-platform, or adjacent products, can be combined with platform products to form comprehensive platform solutions to meet customer needs. These products are used in solutions sold through each of our businesses and include the following:

• | Accelerators - Silicon products that can operate alone or accompany our processors in a system, such as FPGAs, VPUs, and Mobileye EyeQ* SoC |

• | Boards and systems - Server boards and small form factor systems such as Intel® NUCs |

• | Connectivity products - Cellular modems, Ethernet controllers, silicon photonics, Wi-Fi, and Bluetooth® |

• | Memory and storage products - SSD, persistent memory, and memory components |

| MD&A | 17 | |

OVERVIEW |  | |

DCG develops workload-optimized platforms for compute, storage, and network functions. Market segments include cloud service providers, enterprise and government, and communications service providers. In the first half of 2019, DCG customers, specifically the cloud service providers and enterprise and government market segments absorbed capacity and worked through inventory after a historic customer-driven platform refresh in 2018. As consumption picked back up in the second half of 2019, DCG returned to growth. Continued demand for cloud computing and solutions built for the network and edge fueled growth. | ||

HIGHLIGHTS AND SEGMENT IMPERATIVES | ||

"Our workload-optimized, broad portfolio strategy uniquely enables our customers to move, store, and process the world's data." —Navin Shenoy, Data Platforms Group2 General Manager | ||

● | We delivered sweeping innovation across our data-centric product portfolio, including introduction of the 2nd generation Intel® Xeon® Scalable processor family for the data center, first market introduction of Intel® OptaneTM DC persistent memory, new Intel® Xeon® D processors, and Intel® 800 series Ethernet adapters. | |

● | Adjacent products saw double-digit revenue growth primarily due to Intel® Silicon Photonics and Intel® OptaneTM DC persistent memory. | |

● | DCG has significant opportunities in cloud, networking, AI, and data analytics. As we broadened our product offerings and continued to innovate, the data center market TAM1 is expected to grow to approximately $90 billion by 2024. | |

5-YEAR TRENDS |

■ Revenue $B | — Year over Year Growth | ■ Op Income $B | — Year over Year Growth | |||

1 Source: Intel calculated 2024 TAM derived from industry analyst reports.

2 Our Data Platforms Group includes our DCG segment. See "Information About Our Executive Officers" within Other Key Information for more details.

| MD&A | 18 | |

MARKET AND BUSINESS OVERVIEW

Market trends and strategy

Data is a significant force in society, and is being generated at an unprecedented pace. Data center customers want to work with partners who can deliver platforms to address their most important technology challenges. Additionally, as more data is generated, organizations are seeking to analyze data closer to point of origin, giving rise to a data-centric edge environment across industries and providers. We expect the massive growth of data worldwide will increase demand to move, store, and process data and extract value from data. We are one of the few companies that touches every part of the data-centric compute landscape, and we have invested both organically and through acquisitions to capitalize on these demands. We expect these trends to continue to fuel demand in DCG and other data-centric businesses in the long term.

DCG focuses on three market segments: cloud service providers, enterprise and government, and communications service providers. In 2019, cloud revenue grew as service providers continued to invest in infrastructure to meet the explosive demand for digital services, AI, and data analytics. Cloud service provider revenue was down in the first half as customers absorbed capacity and worked through inventory after a historic 2018 platform refresh; this trend stabilized in the second half of 2019. In our enterprise and government market segment, legacy architecture continues to decline on-premise, but enterprises are rapidly embracing cloud as an architecture, and we expect to continue to see growth in hybrid and multi-cloud deployments. In the communications service provider market segment, we gained market segment share as customers chose to virtualize and transform their networks and prepare for the 5G transition using Intel® architecture.

Products and competitiveness

We offer customers an unmatched, broad portfolio of platforms and technologies designed to provide workload-optimized performance across compute, storage, and network. These offerings span the full spectrum from the data center core to the network edge. In addition, DCG focuses on lowering the total cost of ownership and on other specific workload optimizations for the enterprise, cloud service provider, and communications service provider market segments, with hardware-enhanced performance optimizations for AI workloads. DCG's platform value can be extended through Intel adjacent products such as FPGAs and SSDs. As a leading provider of data center platforms, we face competition from competitors such as Advanced Micro Devices, Inc. (AMD), providers of GPU products such as NVIDIA Corporation (NVIDIA), companies using ARM* architecture, new entrants developing products customized for specific data center workloads, and from internally developed solutions by cloud service providers and others. We expect an increasingly competitive environment in 2020.

With over 23 million units shipped to date, the Intel® Xeon® Scalable platform provides the foundation for the data-centric era. In 2019, we launched our 2nd generation Intel® Xeon® Scalable processors, formerly Cascade Lake, which include Intel® Deep Learning Boost. As the industry's only CPUs with built-in AI acceleration, Intel® Xeon® processors can help customers solve challenging problems and gain insight for future opportunities. We also shipped new generations of our Intel® Xeon® D processor product family, designed to deliver improved performance in space- and power-constrained environments. Beyond processing everything, we are enhancing users' digital experiences through continued expansion of adjacent product offerings to store and move data more effectively, such as Intel® OptaneTM DC persistent memory and Intel® 800 series Ethernet adapters.

| MD&A | 19 | |

FINANCIAL PERFORMANCE

DCG REVENUE $B | DCG OPERATING INCOME $B | |||

■ Platform | ■ Adjacent | |

REVENUE SUMMARY |

• | Higher platform ASPs from stronger core mix was partially offset by platform volume decline primarily from TAM contraction in the enterprise and government market segment. |

• | Adjacent growth driven by the continued expansion of Intel® Silicon Photonics in 2019. |

• | Comparing 2019 to 2018, revenue from cloud service providers was up 13%, enterprise and government was down 14%, and communications service providers was up 6% (up 40%, up 2%, and up 25%, respectively, comparing 2018 to 2017). |

2019 – 2018 | 2018 – 2017 | ||||||||||||

(Dollars in Millions) | % Growth | $ Impact | % Growth | $ Impact | |||||||||

Platform volume | down | (3)% | $ | (654 | ) | up | 13% | $ | 2,334 | ||||

Platform ASP | up | 5% | 940 | up | 7% | 1,382 | |||||||

Adjacent products | up | 11% | 204 | up | 13% | 211 | |||||||

Total change in revenue | $ | 490 | $ | 3,927 | |||||||||

OPERATING INCOME SUMMARY |

Operating income decreased 11% year over year, and operating margin was 44% in 2019.

(In Millions) | ||||

$ | 10,227 | 2019 Operating Income | ||

(805 | ) | Higher period charges, primarily associated with the initial ramp of 10nm | ||

(510 | ) | Higher operating expenses primarily related to R&D | ||

(140 | ) | Lower gross margin from adjacent businesses | ||

(80 | ) | Higher platform unit cost | ||

370 | Higher gross margin from platform revenue | |||

(84 | ) | Other | ||

$ | 11,476 | 2018 Operating Income | ||

3,445 | Higher gross margin from platform revenue | |||

(350 | ) | Higher platform unit cost | ||

(14 | ) | Other | ||

$ | 8,395 | 2017 Operating Income | ||

| MD&A | 20 | |

As more intelligence is moving to the edge, more industries are harnessing the power of data to create business value, to innovate, and to grow. We are using our architecture, accelerators, and software assets, combined with scale and partners, to develop a growing Internet of Things portfolio. Our Internet of Things portfolio is comprised of our IOTG and Mobileye businesses. IOTG develops high-performance compute for targeted verticals and embedded markets. Mobileye is the global leader in the development of computer vision and machine learning-based sensing, data analysis, localization, mapping, and driving policy technology for ADAS and autonomous driving.

INTERNET OF THINGS GROUP |

OVERVIEW |  | |

IOTG develops high-performance compute for targeted verticals and embedded markets. Our customers include retailers, manufacturers, healthcare providers, energy companies, automakers, and governments. We facilitate our customers creating, storing, and processing data generated by connected devices to accelerate business transformations. | ||

HIGHLIGHTS AND SEGMENT IMPERATIVES | ||

● | IOTG achieved record revenue and operating income in 2019 on broad business strength and growing demand for edge computing and computer vision-based applications. | |

● | Since 2015, IOTG has had average revenue growth of 14% and operating income growth of 22% per year. | "Intel’s pioneering work in AI and proven data-centric strategy enabled us to predict the massive opportunity of edge computing—years ahead of the industry. Edge is not just a theoretical market opportunity. Together with our ecosystem partners and developers, we’re delivering on this vision today and driving tangible financial results." —Tom Lantzsch, IOTG General Manager |

● | We see significant opportunity for growth driven by an architectural shift toward edge computing, which extends compute from centralized points to be closer to the source inputs. | |

● | We continue to provide updated solutions to accelerate market adoption of computer vision and AI applications. This includes advances in existing offerings such as the OpenVINO™ toolkit, development of the Edge AI Nanodegree* with Udacity to enrich and train the next generation of developers, and the release of Intel® AI DevCloud for the Edge, which allows customers to identify Edge AI solutions that deliver the best mix of performance, power, and price. | |

● | To deliver on the transformative promise of the Internet of Things, we are working with our ecosystem partners to continue to grow the portfolio of Intel® IoT Market Ready Solutions (Intel® IMRS)—scalable, end-to-end solutions that provide solid business results today and lay the foundation for the future. Currently, IOTG has over 170 Intel® IMRS supporting approximately 5,000 new end-to-end deployments in more than 100 countries. | |

| MD&A | 21 | |

5-YEAR TRENDS |

■ Revenue $B | — Year over Year Growth | ■ Op Income $B | — Year over Year Growth | |||||

MARKET AND BUSINESS OVERVIEW

Market trends and strategy

The Internet of Things market sits at the center of a global digital transformation. Through a robust network of devices, software, and sensors, the Internet of Things is transforming the way businesses create products, deliver services, and conduct operations—from schools and hospitals, to retailers and smart factories. Internet of Things-based solutions represent one of the fastest growing segments within the semiconductor industry. However, the Internet of Things is a highly fragmented market with a diverse collection of competitors, products, and vertical segments.

| Many retailers are sitting on mountains of data that can be used to proactively address evolving customer demands. IOTG provides solutions that enable retailers to extract the right insights from their data, in the right place, at the right time, allowing them to use intelligence to transform their businesses to achieve their full potential. The result is greater efficiency, reduced complexity, increased sales, and a more personalized customer experience. | |||||

As a result of consumer preference for more customization and higher-quality manufactured goods, a new kind of factory is emerging—one that is cloud connected and data driven. It is an “intelligent factory” marked by hyper-agility, autonomous production, and the use of data as a transformative force for the business. | ||||||

We help cities and infrastructure providers turn data into actionable insights to enable smarter, safer, and more efficient solutions. Infrastructure providers and cities are seeking the best ways to use Internet of Things technology to enhance the quality of services, improve public safety, reduce congestion, and achieve new levels of efficiency. | ||||||

By 2022, we expect approximately 82% of data traffic will be video1. Processing high-quality video requires the ability to rapidly analyze vast streams of data near the source and to respond to that data in real time, moving only relevant insights to the cloud. Rather than a one-size-fits-all solution, Intel offers a powerful portfolio of scalable hardware and software solutions, including the OpenVINO™ toolkit and the new Intel® Vision Accelerator Design products, to move into an intelligent, data-powered future and to meet the various performance, power, and price requirements of any business, in any industry. | ||||||

Products and competitiveness

We have a long-standing position as a supplier of components and software for embedded products. This marketplace continues to expand significantly, with increasing types and numbers of smart and connected devices for retail, industrial, and consumer uses, including smart video. As this market segment evolves, we face numerous large and small incumbent processor competitors, as well as new entrants that use the ARM* architecture and other operating systems and software. In addition, the Internet of Things requires a broad range of connectivity solutions and we face competition from semiconductor companies providing traditional wireless solutions such as cellular, Wi-Fi, and Bluetooth®, as well as several new entrants who are taking advantage of new focused communications protocols.

IOTG utilizes platform and adjacent products across Intel while making the investments needed to adapt products to the specific requirements for our vertical segments. We offer end-to-end solutions with our wide spectrum of products, including Intel® Atom®, Intel® Core®, and Intel® Xeon® processor-based computing, wireless connectivity, FPGAs, Movidius VPUs, and developer tools such as the OpenVINO™ software toolkit. IOTG product development focuses on addressing the key challenges businesses face when implementing Internet of Things solutions, including interoperability, connectivity, safety, security, industrial use conditions, and long-life support.

1 Source: Cisco Visual Networking Index: Forecast and Trends, 2017-2022, updated February 27, 2019.

| MD&A | 22 | |

MOBILEYE |

OVERVIEW |  | |

Mobileye is the global leader in driving assistance and automation solutions. Our product portfolio employs a broad set of technologies, covering computer vision and machine learning-based sensing, data analysis, localization, mapping, and driving policy technology for ADAS and autonomous driving. Mobileye’s ADAS products form the building blocks for higher levels of autonomy. Our customers and strategic partners include major global OEMs and Tier 1 automotive system integrators. | ||

HIGHLIGHTS AND SEGMENT IMPERATIVES | ||