Financial summary

Ten years ended December 29, 2001

| (In millions—except per share amounts) |

Net revenues |

Cost of sales |

Research & development |

Purchased in-process research & development |

Amortization of goodwill & acquistion- related intangibles & costs |

Operating income |

Net income |

Basic earnings per share |

Diluted earnings per share |

||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

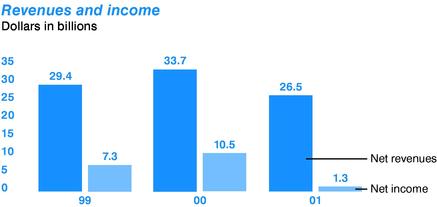

| 2001 | $ | 26,539 | $ | 13,487 | $ | 3,796 | $ | 198 | $ | 2,338 | $ | 2,256 | $ | 1,291 | $ | .19 | $ | .19 | |||||||||

| 2000 | $ | 33,726 | $ | 12,650 | $ | 3,897 | $ | 109 | $ | 1,586 | $ | 10,395 | $ | 10,535 | $ | 1.57 | $ | 1.51 | |||||||||

| 1999 | $ | 29,389 | $ | 11,836 | $ | 3,111 | $ | 392 | $ | 411 | $ | 9,767 | $ | 7,314 | $ | 1.10 | $ | 1.05 | |||||||||

| 1998 | $ | 26,273 | $ | 12,088 | $ | 2,509 | $ | 165 | $ | 56 | $ | 8,379 | $ | 6,068 | $ | .91 | $ | .86 | |||||||||

| 1997 | $ | 25,070 | $ | 9,945 | $ | 2,347 | — | — | $ | 9,887 | $ | 6,945 | $ | 1.06 | $ | .97 | |||||||||||

| 1996 | $ | 20,847 | $ | 9,164 | $ | 1,808 | — | — | $ | 7,553 | $ | 5,157 | $ | .78 | $ | .73 | |||||||||||

| 1995 | $ | 16,202 | $ | 7,811 | $ | 1,296 | — | — | $ | 5,252 | $ | 3,566 | $ | .54 | $ | .50 | |||||||||||

| 1994 | $ | 11,521 | $ | 5,576 | $ | 1,111 | — | — | $ | 3,387 | $ | 2,288 | $ | .34 | $ | .33 | |||||||||||

| 1993 | $ | 8,782 | $ | 3,252 | $ | 970 | — | — | $ | 3,392 | $ | 2,295 | $ | .34 | $ | .33 | |||||||||||

| 1992 | $ | 5,844 | $ | 2,557 | $ | 780 | — | — | $ | 1,490 | $ | 1,067 | $ | .16 | $ | .16 | |||||||||||

| (In millions—except employees and per share amounts) |

Employees at year-end (in thousands) |

Net investment in property, plant & equipment |

Total assets |

Long-term debt & put warrants |

Stock- holders' equity |

Additions to property, plant & equipment |

Weighted average diluted shares outstanding |

Dividends declared per share |

Dividends paid per share |

||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 83.4 | $ | 18,121 | $ | 44,395 | $ | 1,050 | $ | 35,830 | $ | 7,309 | 6,879 | $ | .080 | $ | .080 | |||||||||

| 2000 | 86.1 | $ | 15,013 | $ | 47,945 | $ | 707 | $ | 37,322 | $ | 6,674 | 6,986 | $ | .070 | $ | .070 | |||||||||

| 1999 | 70.2 | $ | 11,715 | $ | 43,849 | $ | 1,085 | $ | 32,535 | $ | 3,403 | 6,940 | $ | .055 | $ | .055 | |||||||||

| 1998 | 64.5 | $ | 11,609 | $ | 31,471 | $ | 903 | $ | 23,377 | $ | 4,032 | 7,035 | $ | .025 | $ | .033 | |||||||||

| 1997 | 63.7 | $ | 10,666 | $ | 28,880 | $ | 2,489 | $ | 19,295 | $ | 4,501 | 7,179 | $ | .029 | $ | .028 | |||||||||

| 1996 | 48.5 | $ | 8,487 | $ | 23,735 | $ | 1,003 | $ | 16,872 | $ | 3,024 | 7,101 | $ | .024 | $ | .023 | |||||||||

| 1995 | 41.6 | $ | 7,471 | $ | 17,504 | $ | 1,125 | $ | 12,140 | $ | 3,550 | 7,072 | $ | .019 | $ | .018 | |||||||||

| 1994 | 32.6 | $ | 5,367 | $ | 13,816 | $ | 1,136 | $ | 9,267 | $ | 2,441 | 6,992 | $ | .014 | $ | .014 | |||||||||

| 1993 | 29.5 | $ | 3,996 | $ | 11,344 | $ | 1,114 | $ | 7,500 | $ | 1,933 | 7,056 | $ | .013 | $ | .013 | |||||||||

| 1992 | 25.8 | $ | 2,816 | $ | 8,089 | $ | 622 | $ | 5,445 | $ | 1,228 | 6,872 | $ | .006 | $ | .003 | |||||||||

Management's discussion and analysis

of financial condition and results of operations

Results of operations

Consolidated revenues and margin > For 2001, our net revenues of $26.5 billion were 21% below 2000 net revenues, reflecting a tough year for the technology industry. Revenues declined across all of our geographies and major product lines as we felt the impact of the worldwide economic slowdown. Our decrease in net revenues came primarily from the Intel Architecture operating segment in the form of significantly lower unit volumes and significantly lower average selling prices of microprocessors. Lower revenues in both the Intel Communications Group and the Wireless Communications and Computing Group also contributed to the decline as demand for these products decreased significantly.

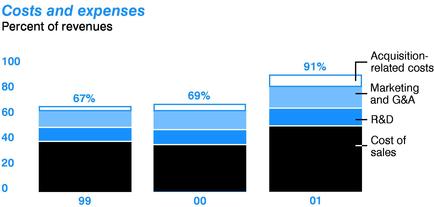

In spite of the revenue decline and the lower sales volume of microprocessors, cost of sales increased 7% in 2001 compared to 2000, primarily due to increased start-up costs and higher unit costs for microprocessors in the Intel Architecture business.

Our gross margin percentage decreased significantly, from 62% in 2000 to 49% in 2001, primarily due to lower revenues from sales of microprocessors, including the effect of lower average selling prices and the impact of spreading fixed factory costs over a lower volume. Higher factory start-up costs for the Intel Architecture business also contributed to the decline in the gross margin percentage. The impact of lower sales volume and a decline in factory capacity utilization in the Wireless Communications and Computing Group, as well as lower sales in the Intel Communications Group, also lowered the gross margin percentage. See "Outlook" for a discussion of gross margin expectations.

By contrast, from 1999 to 2000, our net revenues increased by 15%, primarily due to a higher unit sales volume of microprocessors, partially offset by lower average selling prices in the Intel Architecture business. Additionally, revenues from sales of flash memory in the Wireless Communications and Computing Group grew significantly from 1999 to 2000, as did networking and communications product sales in the Intel Communications Group.

Cost of sales increased 7% in 2000 compared to 1999, due to higher sales volume in the Wireless Communications and Computing Group and the Intel Communications Group. This increase was partially offset by lower cost of sales in the Intel Architecture business, primarily due to lower unit costs.

The gross margin percentage increased to 62% in 2000 from 60% in 1999, primarily as a result of higher gross margin in the Intel Architecture business due to lower microprocessor unit costs. These lower costs were partially offset by lower average selling prices for microprocessors and the costs recorded in 2000 related to chipsets and motherboards with a defective memory translator hub (MTH). Improved demand and higher prices for flash memory in the Wireless Communications and Computing Group also contributed to the improvement in gross margin percentage.

Intel Architecture > The Intel Architecture operating segment consists of the Desktop Platforms Group, the Mobile Platforms Group and the Enterprise Platforms Group. Net revenues for this business decreased by $5.9 billion, or 21%, in 2001 compared to 2000. The decrease in net revenues was primarily due to significantly lower unit volumes and significantly lower average selling prices of microprocessors. The lower selling prices reflect the impact of competitive pricing pressures and our strategy to accelerate the transition from the Pentium® III processor to the Pentium® 4 processor. For 2001, sales of microprocessors based on the P6 microarchitecture (including the Celeron®, Pentium III and Pentium® III Xeon™ processors), as well as related board-level products and chipsets, comprised a majority of our consolidated net revenues and a substantial majority of our gross margin. For the same period, sales of products based on the Intel® NetBurst™ microarchitecture, including the Pentium 4 and Intel® Xeon™ processors and related products, were a significant and rapidly increasing portion of our consolidated net revenues and gross margin.

Net operating results decreased by $6.3 billion, or 50%, in 2001 compared to 2000, primarily due to lower average selling prices, lower unit volumes and higher unit costs for microprocessors. Increased start-up costs related to the 0.13-micron manufacturing process technology, which ramped in four factories during 2001, and start-up costs on 300-millimeter wafer manufacturing also contributed to the decline. Lower revenue-dependent expenses and reduced spending due to company-wide cost reduction programs partially offset the decline in net operating results.

For 2000, net revenues increased by $1.8 billion, or 7%, compared to 1999. The increase in net revenues was primarily due to higher unit sales volume of microprocessors, partially offset by lower average selling prices. For 2000, sales of microprocessors based on the P6 microarchitecture, as well as related board-level products and chipsets comprised a substantial majority of our consolidated net revenues and gross margin.

Net operating results increased by $1.4 billion, or 12%, in 2000 compared to 1999, primarily due to higher sales and lower unit costs of microprocessors. The decreased unit costs were achieved primarily through the continued transition to redesigned microprocessor products with lower cost packaging as well as factory efficiencies. The lower unit costs were partially offset by higher costs due to a higher sales volume of microprocessors and the costs recorded in 2000 related to chipsets and motherboards with the defective MTH component.

In January 2002, we announced the promotion of Paul S. Otellini, who was Executive Vice President and General Manager of the Intel Architecture Group, to President and Chief Operating Officer of Intel.

Intel Communications Group > Net revenues decreased by $903 million, or 26%, in 2001 compared to 2000, primarily due to significantly lower unit volumes of embedded control chips, network processing components, enterprise infrastructure and telecommunications products, including telecommunications boards, consistent with an industry-wide reduction in demand for these products. The overall revenue decline was partially offset by incremental revenues related to acquisitions completed in 2001.

Net operating results decreased by $1.1 billion to a loss of $735 million in 2001 from a profit of $319 million in 2000, primarily due to the lower unit volumes of embedded control chips, network processing components and telecommunications-related products. Higher research and development spending in 2001 also contributed to the decline, primarily due to businesses acquired in 2001 and a full year of spending for acquisitions made in 2000.

For 2000, net revenues increased by $1.1 billion, or 46%, compared to 1999, primarily due to significantly higher unit volumes of telecommunications-related products, network processing components and optical networking equipment. The net increase in revenues includes incremental revenues related to acquisitions completed in 2000 and a full year of revenues from acquisitions completed in 1999.

Net operating results decreased by $118 million to $319 million in 2000 from $437 million in 1999, primarily due to the higher research and development spending from acquired businesses, partially offset by revenues from the higher sales volume of network processing components and telecommunications-related products.

Wireless Communications and Computing Group > Net revenues decreased by $437 million, or 16%, in 2001 compared to 2000. For the first half of 2001, the decline was primarily due to significantly lower unit sales of flash memory as the cellular market worked through inventories built up in the latter part of 2000. For the second half of 2001, the decline was primarily due to lower volumes of flash memory units brought on by the worldwide economic slowdown.

Net operating results decreased by $864 million to a loss of $256 million in 2001 from a profit of $608 million in 2000, primarily due to lower flash memory volume, the impact of decreased factory capacity utilization and higher inventory writedowns in the first half of 2001. Higher research and development spending also contributed to the decline.

By contrast, 2000 net revenues increased by $1.4 billion compared to 1999, primarily due to a significant increase in the unit sales of flash memory as worldwide demand for cellular phones increased dramatically. Average selling prices for flash memory also increased significantly as our mix shifted toward higher density products and we benefited from long-term supply agreements with customers.

Net operating results increased by $704 million to a profit of $608 million in 2000 from a loss of $96 million in 1999, primarily due to increased flash memory revenues, partially offset by increased research and development spending.

Operating expenses, other and taxes > Excluding charges of $198 million for purchased in-process research and development (IPR&D) related to the current year's acquisitions ($109 million in 2000 and $392 million in 1999), research and development spending decreased $101 million, or 3%, in 2001 compared to 2000 and increased $786 million, or 25%, in 2000 compared to 1999. The decrease for 2001 compared to 2000 was primarily due to cost containment efforts, including reductions in discretionary spending on travel-related expenses. The increase for 2000 compared to 1999 was primarily due to increased spending on product development programs, including the product development programs of companies acquired. Marketing, general and administrative expenses decreased $625 million, or 12%, in 2001 compared to 2000, primarily due to decreased revenue-dependent Intel Inside® cooperative advertising program expenses and profit-dependent bonus expenses, as well as lower discretionary spending as a result of cost reduction programs, partially offset by marketing, general and administrative expenses from companies acquired. Marketing, general and administrative expenses increased $1.2 billion, or 31%, from 1999 to 2000, primarily due to increases for the Intel Inside cooperative advertising program, profit-dependent bonus expenses, and marketing, general and administrative expenses from companies acquired.

Amortization of goodwill and other acquisition-related intangibles and costs increased to $2.3 billion in 2001 compared to $1.6 billion in 2000, primarily due to new acquisitions in 2001, a full year's impact of prior-year acquisitions and write-offs of impaired goodwill and identified intangibles of $124 million. Through 2001, in accordance with our accounting policy, we reviewed acquisition-related goodwill and identified intangibles for impairment based on undiscounted cash flows, and these analyses incorporated our estimates of future cash flows related to the acquired businesses. If the new goodwill and intangibles asset accounting standards issued by the Financial Accounting Standards Board (FASB) in July 2001 had been applied in 2001, we estimate that amortization expense would have been approximately $1.6 billion lower than the $2.3 billion reported. For 1999 to 2000, amortization increased $1.2 billion, primarily due to the impact of additional acquisitions and a full year's impact of prior year acquisitions. Amortization for all periods is included in the calculation of the operating loss for the "all other" category for segment reporting purposes.

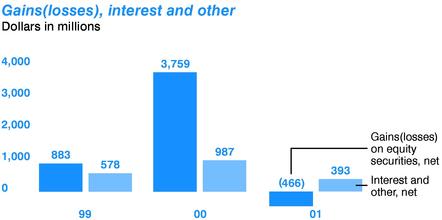

For 2001, net losses on investments in equity securities and certain equity derivatives totaled $466 million, compared to net gains of $3.8 billion (including a significant gain on the sale of our holdings of Micron Technology, Inc.) in 2000. For 2001, the net loss included impairments of $1.1 billion, partially offset by net gains on transactions of $517 million and mark-to-market gains on trading assets and derivatives of $122 million. For 2000 compared to 1999, gains on investments increased by $2.9 billion, primarily due to sales of appreciated securities, including the Micron gain.

Interest and other, net decreased $594 million from 2000 to 2001. Interest income decreased due to lower average investment balances and lower interest rates in 2001 compared to 2000. In addition, we recognized a net loss of $196 million from our investment in Convera Corporation, including $39 million as our proportionate share of Convera's loss and $157 million on the impairment and subsequent sale of the investment. This compares to a gain of $117 million that we recognized on our contribution of a business in the formation of Convera in 2000. For 2000 compared to 1999, interest and other, net increased $409 million, primarily due to higher average investment balances and higher average interest rates, and the $117 million gain on Convera.

Our effective income tax rate was 40.9% in 2001, 30.4% in 2000 and 34.9% in 1999. Excluding the impact of non-deductible IPR&D charges, amortization of non-deductible goodwill, and tax benefits related to prior years of $100 million in 2001 and $600 million in 2000, our adjusted effective tax rate was 25.7% in 2001, 31.8% in 2000 and 33% in 1999. The lower adjusted rate in 2001 compared to 2000 was due to a shift in the mix of income in various tax jurisdictions. The lower adjusted rate in 2000 compared to 1999 reflected the impact of the resolution reached with the Internal Revenue Service in 2000 on a number of issues, including adjustments related to the intercompany allocation of profits.

Purchased in-process research and development

The following table summarizes the significant assumptions underlying the valuations related to IPR&D from major companies acquired at the time of acquisition in fiscal 2001, 2000 and 1999.

| (Dollars in millions) |

IPR&D |

Estimated cost to complete technology |

Discount rate applied to IPR&D |

Weighted average cost of capital |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | |||||||||||

| Xircom | $ | 53 | $ | 7 | 25—55 | % | 22 | % | |||

| VxTel | $ | 68 | $ | 14 | 25—35 | % | 22 | % | |||

| LightLogic | $ | 46 | $ | 7 | 25—35 | % | 23 | % | |||

2000 |

|||||||||||

| GIGA | $ | 52 | $ | 12 | 20 | % | 15 | % | |||

1999 |

|||||||||||

| Dialogic | $ | 83 | $ | 32 | 22 | % | 17 | % | |||

| Level One | $ | 231 | $ | 19 | 30 | % | 23 | % | |||

| DSP Communications | $ | 59 | $ | 13 | 20 | % | 17 | % | |||

Included below are further details regarding the technology acquired in these transactions.

2001 acquisitions > In March, we acquired Xircom, Inc., which specializes in PC cards and other products used to connect mobile computing devices to corporate networks and the Internet. Xircom had 20 IPR&D projects, each contributing from 1% to 24% of the total IPR&D value. The in-process projects included the development of next-generation PC card devices for portable computing connectivity that support various computing standards. These projects ranged from 5% to 86% complete. All projects had expected completion dates in 2001 at the time of acquisition. Expected completion dates for three projects comprising 30% of the total IPR&D value were revised to 2002, and nine additional projects representing 33% of the total IPR&D value were cancelled in the third quarter of 2001 in order to focus on core competencies and the next generation of current products. Xircom's remaining projects were completed as scheduled.

In April, we acquired VxTel Inc., which designs signal and packet processing silicon and system-level solutions that form the foundation for next-generation optical networks. VxTel had two IPR&D projects, with its digital signal processor project accounting for 89% of the total IPR&D value. The project was 84% complete at the time of acquisition and was completed in 2001.

In May, we acquired LightLogic, Inc., which designs advanced opto-electronic modules for next-generation optical communications systems. LightLogic had four IPR&D projects, each contributing from 8% to 52% of the total IPR&D value. These projects ranged from 40% to 80% complete and had expected completion dates in 2001 at the time of acquisition. Two projects have been completed, and the remaining two projects are expected to be completed in 2002.

2000 acquisitions > In March, we acquired GIGA A/S. GIGA specializes in the design of advanced, high-speed communications chips used in optical networking and communications products that direct traffic across the Internet and corporate networks. One project accounted for 73% of the IPR&D value and was approximately 61% complete at the time of acquisition. This project was completed on schedule in 2000.

1999 acquisitions > In July, we acquired Dialogic Corporation. Dialogic designs, manufactures and markets computer hardware and software enabling technology for computer telephony systems. Two projects accounted for 65% of the value assigned to IPR&D and were 55% to 60% complete at the time of acquisition. Dialogic's projects have been completed.

In August, we acquired Level One Communications, Inc. Level One provides silicon connectivity, switching and access solutions for high-speed telecommunications, and networking applications. Eight IPR&D projects were identified and valued, ranging from 39% to 86% complete at the time of acquisition. Level One's projects have been completed.

In November, we acquired DSP Communications, Inc. DSP Communications develops and supplies form-fit reference designs, chipsets and software for mobile telephone manufacturers. Four IPR&D projects were identified and valued, with each project representing from 9% to 31% of the total IPR&D value and ranging from 10% to 90% complete at the time of acquisition. Significant portions of three projects, representing 73% of the value assigned to IPR&D, have been cancelled, with technology development efforts refocused on next-generation standards. Projects completed represented approximately 23% of the value assigned to IPR&D.

Financial condition

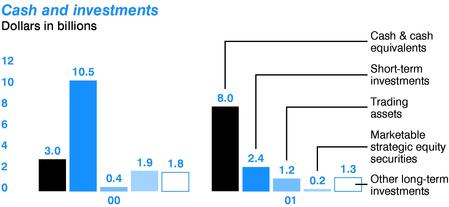

Although 2001 was a difficult year, our financial condition remained strong. At December 29, 2001, cash, short-term investments and trading assets totaled $11.6 billion, down from $13.8 billion at December 30, 2000. Total short-term and long-term debt of $1.5 billion was 4% of stockholders' equity at the end of 2001, compared to 3% of stockholders' equity at the end of 2000. At the end of 2001, we had future operating lease obligations not included on our balance sheet totaling $610 million, primarily related to facilities. In addition, at the end of 2001, we had contractual obligations of $1.9 billion for the purchase or construction of property, plant and equipment. See "Outlook" for a discussion of capital expenditure expectations for 2002.

For 2001, cash provided by operating activities was $8.7 billion, compared to $12.8 billion in 2000 and $12.1 billion in 1999. Although unit sales were down significantly in 2001, we ended the year with inventory levels approximately the same as at the end of 2000. Raw materials and finished goods inventory decreased, offset by an increase in work-in-process inventory associated with the ramp of the

Pentium 4 processor and the 0.13-micron manufacturing process technology. For 2001, accounts receivable decreased significantly, primarily due to the lower revenues, but the days' sales outstanding were unchanged from fiscal year-end 2000. For 2001, as a group, our five largest customers accounted for approximately 38% of net revenues, and of this group one customer accounted for 14% of revenues. At December 29, 2001, these five largest customers accounted for approximately 41% of net accounts receivable.

We used $195 million in net cash for investing activities during 2001, compared to $10.0 billion during 2000 and $6.2 billion during 1999. This decrease reflects net sales of available-for-sale investments and a shift to investments with shorter initial maturities that are classified as cash equivalents. Capital expenditures totaled $7.3 billion in 2001 as we continued to invest in property, plant and equipment, primarily for additional microprocessor manufacturing capacity, including 300-millimeter manufacturing capacity and the transition to the 0.13-micron manufacturing process technology. During 2001, we also paid $883 million in cash for acquisitions, net of cash acquired, including the purchases of Xircom and VxTel.

We used $3.5 billion in net cash for financing activities in 2001, compared to $3.5 billion in 2000 and $4.2 billion in 1999. The major financing applications of cash in 2001 were for the repurchase of 133 million shares of common stock for $4.0 billion and payment of dividends of $538 million. The major financing applications of cash in 2000 were for stock repurchases totaling $4.0 billion ($4.6 billion in 1999) and payments of dividends of $470 million ($366 million in 1999). Financing sources of cash during 2001 were primarily $762 million in proceeds from the sale of shares, pursuant to employee stock plans ($797 million in 2000 and $543 million in 1999).

At December 29, 2001, marketable strategic equity securities totaled $155 million, with $46 million in net unrealized appreciation. The total value of the marketable strategic equity securities decreased by $1.8 billion compared to December 30, 2000, and net unrealized appreciation decreased by approximately $246 million, primarily due to sales of securities and declines in market values. At the end of 2001, the carrying value of our non-marketable equity securities was $1.3 billion, down from $1.7 billion at the end of 2000, primarily due to the impact of impairment charges, partially offset by additional investments.

Another potential source of liquidity is authorized borrowings, including commercial paper, of $3.0 billion. We also maintain the ability to issue an aggregate of approximately $1.4 billion in debt, equity and other securities under U.S. Securities and Exchange Commission shelf registration statements.

We believe that we have the financial resources needed to meet business requirements for the next 12 months, including capital expenditures for the expansion or upgrading of worldwide manufacturing capacity, working capital requirements and the dividend program.

Financial market risks

We are exposed to financial market risks, including changes in interest rates, non-U.S. currency exchange rates and marketable equity security prices. To mitigate these risks, we utilize derivative financial instruments, among other strategies. Other than warrants and other equity derivatives that we acquired for strategic purposes, we do not use derivative financial instruments for speculative purposes. All of the potential changes noted below are based on sensitivity analyses performed on our financial positions at December 29, 2001. Actual results may differ materially.

The primary objective of our investments in debt securities is to preserve principal while maximizing yields, without significantly increasing risk. To achieve this objective, the returns on a substantial majority of our marketable investments in long-term fixed rate debt securities are swapped to U.S. dollar LIBOR-based returns. We considered the historical volatility of the three-month LIBOR rate experienced in the past year and determined that it was reasonably possible that an adverse change of 80 basis points, approximately 43% of the rate at the end of 2001, could be experienced in the near term. A hypothetical 80-basis-point increase in interest rates, after taking into account hedges and offsetting positions, would have resulted in an approximate $10 million decrease in the fair value of our investments in debt securities as of the end of 2001 and a $20 million decrease as of the end of 2000.

We generally hedge currency risks of investments denominated in non-U.S. currencies with non-U.S.-currency borrowings, currency forward contracts and currency interest rate swaps. Gains and losses on these non-U.S.-currency investments would generally be offset by corresponding losses and gains on the related hedging instruments, resulting in negligible net exposure.

A substantial majority of our revenue, expense and capital purchasing activities are transacted in U.S. dollars. However, we do enter into these transactions in other currencies, primarily Japanese yen and certain other Asian and European currencies. To protect against reductions in value and the volatility of future cash flows caused by changes in currency exchange rates, we have established revenue, expense and balance sheet hedging programs. Currency forward contracts and currency options are utilized in these hedging programs. Our hedging programs reduce, but do not always entirely eliminate, the impact of currency exchange rate movements. We considered the historical trends in currency exchange rates and determined that it was reasonably possible that adverse changes in exchange rates of 20% for certain Asian and European currencies and 10% for all other currencies could be experienced in the near term. Such an adverse change, after taking into account hedges and offsetting positions, would have resulted in an adverse impact on income before taxes of less than $6 million as of the end of 2001 and $20 million as of the end of 2000.

We have a portfolio of equity investments that includes marketable securities classified as either marketable strategic equity securities or trading assets, as well as derivative equity instruments such as warrants and options. To the extent that these investments continue to have strategic value, we typically do not attempt to reduce or eliminate our market exposure. These investments are generally in companies in the high-technology industry, and a substantial majority of the market value of the portfolio is in two sectors: communications, including networking and storage companies, and computing. As of December 29, 2001, five equity positions constituted approximately 50% of the market value of the portfolio, with no individual position exceeding 11% of the portfolio.

We analyzed the historical movements over the past several years of high-technology stock indices that we considered appropriate. Based on the analysis, we estimated that it was reasonably possible that the prices of the stocks in our portfolio could experience a 30% adverse change in the near term. Assuming a 30% adverse change in market prices, and after reflecting the impact of hedges and offsetting positions, our portfolio would decrease in value by approximately $70 million, based on the value of the portfolio as of December 29, 2001 (a decrease in value of $575 million based on the portfolio as of the end of 2000). The decrease in this hypothetical exposure from 2000 to 2001 reflects the decrease in the size of the portfolio due to sales of investments and declines in market values. The portfolio's concentrations in specific companies or sectors may vary over time and may be different from the compositions of the indices analyzed, and these factors may affect the portfolio's price volatility. This estimate is not necessarily indicative of future performance, and actual results may differ materially.

An adverse movement of equity market prices would also have an impact on our portfolio of non-marketable strategic equity securities, although the impact cannot be directly quantified. Such a movement and the related underlying economic conditions would negatively affect the prospects of the companies we invest in, their ability to raise additional capital and the likelihood of our being able to realize our investments through liquidity events such as initial public offerings, mergers and private sales. At December 29, 2001, our non-marketable strategic equity securities had a carrying amount of $1.3 billion, excluding equity derivatives that are subject to mark-to-market requirements.

Strategy

This strategy section and the following outlook section contain a number of forward-looking statements, all of which are based on current expectations. Actual results may differ materially. These statements do not reflect the potential impact of any mergers, acquisitions or business combinations that had not closed as of March 7, 2002.

Our goal is to be the preeminent building block supplier to the worldwide Internet economy by focusing on our core competencies in silicon design and manufacturing, and digital computing and communications. Our primary focus areas are the desktop and mobile platforms, the server platform, the networking and communications platform, and the handheld computing platform. The platforms are supported by our four silicon architectures for the Internet: IA-32, the Intel® Itanium™ processor family, the Intel® Internet Exchange Architecture (Intel® IXA) and the Intel® Personal Internet Client Architecture (Intel® PCA).

Intel Architecture > The Intel Architecture operating segment supports the desktop and mobile platforms with the IA-32 architecture. The IA-32 architecture includes both the Intel NetBurst and P6 microarchitectures. Our strategy for desktop and mobile platforms is to introduce ever higher performance microprocessors and chipsets, tailored for the different market segments of the worldwide computing market, using a tiered branding approach. In line with our strategy, we deliver the Pentium 4 processor for the performance and mainstream market segments, focused on both home and business applications. These applications are optimized for consumers who want to take advantage of the latest Web technologies, such as broadband, interactive 3D, and streaming video and audio. (See "Contingencies" in the "Notes to consolidated financial statements" for a discussion of patent litigation by VIA Technologies, Inc. relating to the Pentium 4 processor.) We also deliver the Intel Celeron processor for the value market segment. To further enhance the acceptance and deployment of these products, we drive initiatives that will support technologies that address wireless solutions, software enabling, security and extended battery life for mobile personal computers (PCs). We also strive to align the industry, our customers and end users to increase acceptance of the desktop and mobile platforms by working with standards bodies, trade associations, original equipment manufacturers and independent software vendors.

The Intel Architecture operating segment also supports the server platform with the Intel Xeon processor family under the IA-32 architecture for workstations and mid-range to high-end servers, and the Intel Itanium processor family for enterprise-class servers. Our strategy for the server platform is to provide higher performance processors and the best price for performance for the various server and workstation market segments. In line with this strategy, we introduced a new version of the Intel Xeon processor running at 2.0 GHz, which established benchmark records in a broad range of server workload categories. In December 2001, we began shipping pilot systems of the next-generation Itanium processor, codenamed "McKinley." (See "Contingencies" in the "Notes to consolidated financial statements" for a discussion of patent litigation by Intergraph Corporation relating to the Itanium processor.) To further increase the acceptance and deployment of these server and workstation products by our customers, we also provide e-Business solutions and best practices through our Intel® e-Business Network. In 2001, we also broadened engagements with developers and solutions providers to make it easier for end users to deploy best-of-class solutions on Intel architecture products.

We plan to cultivate new businesses as well as continue to work with the computing industry to expand Internet capabilities and product offerings, and develop compelling software applications that can take advantage of higher performance microprocessors and chipsets, thus driving demand toward our newer products in each computing market segment. Our microprocessor products compete with existing and future products in the various computing market segments, and we have experienced an increase in the competitive product offerings in the performance desktop market segment and recently in the mobile market segment. We may continue to take various steps, including reducing microprocessor prices and offering rebates and other incentives, at such times as we deem appropriate, in order to increase acceptance of our latest technology and to remain competitive within each relevant market segment.

Intel Communications Group > Within the Intel Communications Group, our strategy for the networking and communications platform is based on three focus areas that we believe are defining trends for the Internet: Ethernet connectivity products, optical components and network processing components. Our strategy for Ethernet connectivity is to expand our product portfolio within the local area network (LAN) and to address the emerging metropolitan area network (MAN) and networked storage market segments. Within the LAN, we will invest in Gigabit Ethernet technologies and wireless technologies based on the 802.11 industry standards. In the storage market segment, we are developing products that enable storage resources to be added to any location on an Ethernet network. Our strategy for optical components is to deliver equipment based on industry standards, including Ethernet and data transport standards in the telecommunications industry (SONET/SDH), focused on the MAN and wide area network (WAN) market segments. We are providing 10-Gigabit Ethernet-based optical components at multiple levels of integration with increased speed and signal transmission distance. In network processing, our strategy is to deliver products that are

the basic building blocks for modular networking infrastructure. These include advanced, programmable processors that are used to manage and direct data moving across the Internet and corporate networks.

Wireless Communications and Computing Group > Within the Wireless Communications and Computing Group, our strategy for the cellular handset and handheld computing platform is to deliver complete solutions that enable quick deployment of applications and services for wireless Internet and handheld computing devices. The Intel PCA architecture describes the separation of the communication and application building blocks for data-enabled cellular phones and portable handheld devices. By separating the communication and application elements within a device, Intel PCA allows for faster time-to-market for our customers and a standard, scalable platform for application development. Our current and expected future products for the handheld platform include flash memory, processors based on the Intel® StrongARM* processor and Intel® XScale™ microarchitecture, and cellular baseband chipsets.

The New Business Group > The New Business Group is chartered to develop and grow new businesses around our core capabilities. The group's current investments include Web hosting services, software and semiconductor products.

Outlook

The methods, estimates and judgments we use in applying our most critical accounting policies have a significant impact on the results we report in our financial statements. The U.S. Securities and Exchange Commission has defined the most critical accounting policies as the ones that are most important to the portrayal of our financial condition and results, and require us to make our most difficult and subjective judgments, often as a result of the need to make estimates of matters that are inherently uncertain. Based on this definition, our most critical policies include: valuation of non-marketable equity securities, which impacts gains (losses) on equity securities when we record impairments; valuation of inventory, which impacts cost of sales and gross margin; and the assessment of recoverability of goodwill and other intangible assets, which impacts write-offs of goodwill and intangibles. Below, we discuss these policies further, as well as the estimates and judgments involved. We also have other key accounting policies, such as our policies for revenue recognition, including the deferral of revenues on sales to distributors, and for estimating the useful lives of our manufacturing assets. We believe that these other policies either do not generally require us to make estimates and judgments that are as difficult or as subjective, or it is less likely that they would have a material impact on our reported results of operations for a given period.

In general, as we look ahead to the rest of 2002, economic indicators remain weak, and we continue to be cautious, although the steep declines we saw over the past year appear to have abated. We expect to be ready for a turn in the economy, with products, capacity and people in place, but we cannot predict when that will happen. Although it is difficult to predict product demand in 2002, we expect continued growth in the total number of computers using the Intel Pentium 4 processor based on the new Intel NetBurst microarchitecture. The flash memory business within the Wireless Communications and Computing Group remains soft due to flattening sales of cellular phones, and we continue to see weak demand from telecommunications customers in the Intel Communications Group.

Our financial results are substantially dependent on sales of microprocessors and related components by the Intel Architecture operating segment. Revenues are partly a function of the mix of microprocessor types and speeds sold, as well as the mix of related chipsets, motherboards, purchased components and other semiconductor products, all of which are difficult to forecast. Because of the wide price difference among performance desktop, value desktop, mobile and server microprocessors, the mix of types of microprocessors sold affects the average price that we will realize and has a large impact on our revenues and gross margin. Microprocessor revenues are dependent on the availability of other parts of the system platform, including chipsets, motherboards, operating system software and application software. Our expectations regarding conditions in the worldwide computing industry are dependent in part on the growth in Internet use and the expansion of Internet product offerings. Our expectations are also subject to the impact of economic conditions in various geographic regions.

Our gross margin expectation for 2002 is 51% plus or minus a few points, and 51% is two points higher than the 2001 gross margin of 49%. The gross margin percentage should benefit from revenue growth and expected cost savings as we ramp the 0.13-micron manufacturing process in 2001. Our gross margin varies, depending on unit volumes, the mix of types and speeds of processors sold, as well as the mix of microprocessors, related chipsets and motherboards, and other semiconductor and non-semiconductor products. Our policy for valuation of inventory, including the determination of obsolete or excess inventory, requires us to estimate the future demand for our products within specific time horizons, generally six months or less. The estimates of future demand that we use in the valuation of inventory are also used for near-term factory planning, and are consistent with our published revenue forecast. If our demand forecast is greater than actual demand and we fail to reduce manufacturing output accordingly, we would likely be required to record additional inventory reserves, which would have a negative impact on our gross margin. Various other factors—including unit volumes, yield issues associated with production at factories, ramp of new technologies, excess or shortage of manufacturing capacity and the reusability of factory equipment—will also continue to affect cost of sales and the variability of gross margin percentages.

We have significantly expanded our semiconductor manufacturing and assembly and test capacity over the last few years, and we continue to plan capacity based on the assumed continued success of our strategy as well as the acceptance of our products in specific market segments. However, we expect that capital spending will decrease to approximately $5.5 billion in 2002 from $7.3 billion in 2001. The reduction is primarily the result of expected improvements in capital efficiency as we transition to the larger, 300-millimeter wafer manufacturing process and the timing of manufacturing process technology cycles. If market demand does not grow and move rapidly toward higher performance products in the various market segments, revenues and gross margin may be adversely affected, manufacturing capacity could be under-utilized, and the rate of capital spending could be reduced. Revenues and gross margin may also be affected if we do not add capacity fast enough to meet market demand. This capital spending plan is dependent on expectations regarding production efficiencies and delivery times of various machinery and equipment, and construction schedules for new facilities. Depreciation for 2002 is expected to be approximately $4.6 billion, compared to $4.1 billion in 2001. Most of this increase would be included in cost of sales and research and development spending.

Our industry is characterized by very short product life cycles, and our continued success is dependent on technological advances, including the development and implementation of new processes and new strategic products for specific market segments. Because we consider it imperative to maintain a strong research and development

program, spending for research and development in 2002, excluding purchased in-process research and development, is expected to increase to approximately $4.1 billion from $3.8 billion in 2001. The higher spending is primarily for next-generation manufacturing technology, including development of 90-nanometer (0.09-micron) manufacturing process technology on 300-millimeter wafer manufacturing. We also intend to continue spending to promote our products and to increase the value of our product brands.

In March 2001, we announced that we expected to reduce our employee base by approximately 5,000 people over the remainder of 2001, primarily through attrition and a voluntary separation plan. We had exceeded this goal by the end of 2001.

We are completing the adoption of the FASB Statements of Financial Accounting Standards Nos. 141 and 142 on accounting for business combinations and goodwill as of the beginning of 2002. Accordingly, we will no longer amortize goodwill from acquisitions, but will continue to amortize other acquisition-related intangibles and costs. Consequently, we expect amortization of acquisition-related intangibles and costs to be approximately $440 million for 2002, down from $2.3 billion of amortized goodwill and acquisition-related intangibles and costs in 2001.

In conjunction with the implementation of the new accounting rules for goodwill, as of the beginning of fiscal 2002, we have completed a goodwill impairment review for the Intel Communications Group and the Wireless Communications and Computing Group, the reporting units that have substantially all of our recorded goodwill, and found no impairment. According to our accounting policy under the new rules, we will perform a similar review annually, or earlier if indicators of potential impairment exist. Our impairment review is based on a discounted cash flow approach that uses our estimates of future market share and revenues and costs for these groups as well as appropriate discount rates. The estimates we have used are consistent with the plans and estimates that we are using to manage the underlying businesses. If we fail to deliver new products for these groups, if the products fail to gain expected market acceptance, or if market conditions in the communications businesses fail to improve, our revenue and cost forecasts may not be achieved, and we may incur charges for impairment of goodwill.

During 2000 and 2001, we sold most of our portfolio of marketable strategic equity securities; however, at the end of 2001, we held $1.3 billion in non-marketable equity securities. Our ability to recover our investments in non-marketable equity securities and to earn a return on these investments is largely dependent on equity market conditions and the occurrence of liquidity events, such as initial public offerings, mergers and private sales. All of these factors are difficult to predict, particularly in the current economic environment. In addition, under our accounting policy, we are required to review all of our investments for impairment. For non-marketable equity securities, this requires significant judgment, including assessment of the investees' financial condition, the existence of subsequent rounds of financing and the impact of any relevant contractual preferences, as well as the investees' historical results of operations, and projected results and cash flows. If the actual outcomes for the investees are significantly different from our projections, our recorded impairments may be understated, and we may incur additional charges in future periods.

We currently expect our tax rate to be approximately 28.4% for 2002, excluding the impact of costs from prior and any future acquisitions. This estimate is based on current tax law, the current estimate of earnings and the expected distribution of income among various tax jurisdictions, and is subject to change.

On January 1, 2002, the national currencies of 12 European countries were replaced with the Euro. During the three-year transition period, our conversion of systems and processes was successfully completed with no material impact on our operations. The introduction of the Euro has not materially affected our currency exchange and hedging activities, and has not resulted in any material increase in costs.

We are currently a party to various legal proceedings. Although litigation is subject to inherent uncertainties, management, including internal counsel, does not believe that the ultimate outcome of these legal proceedings will have a material adverse effect on our financial position or overall trends in results of operations. However, if an unfavorable ruling were to occur in any specific period, there exists the possibility of a material adverse impact on the results of operations of that period. Management believes, given our current liquidity and cash and investment balances, that even an adverse judgment would not have a material impact on cash and investments or liquidity.

Our future results of operations and the other forward-looking statements contained in this outlook and in our strategy discussion involve a number of risks and uncertainties—in particular the statements regarding our goals and strategies, expectations regarding new product introductions, plans to cultivate new business to expand the Internet, future economic conditions, revenues, pricing, gross margin and costs, capital spending, depreciation and amortization, research and development expenses, potential impairment of investments, the tax rate and pending legal proceedings. In addition to the factors discussed above, among the other factors that could cause actual results to differ materially are the following: business and economic conditions and trends in the computing and communications industries in various geographic regions; possible disruption in commercial activities related to terrorist activity and armed conflict, such as changes in logistics and security arrangements, and reduced end-user purchases relative to expectations; the impact of events outside the United States, such as the business impact of fluctuating currency rates, unrest or political instability in a locale, such as unrest in Israel; changes in customer order patterns; competitive factors such as competing chip architectures and manufacturing technologies, competing software-compatible microprocessors and acceptance of new products in specific market segments; pricing pressures; development and timing of the introduction of compelling software applications; excess or obsolete inventory and variations in inventory valuation; continued success in technological advances, including development and implementation of new processes and strategic products for specific market segments; execution of the manufacturing ramp, including the transition to 0.13-micron manufacturing process technology; excess manufacturing capacity; the ability to sustain and grow networking, communications, wireless and other Internet-related businesses, and successfully integrate and operate any acquired businesses; unanticipated costs or other adverse effects associated with processors and other products containing errata (deviations from published specifications); and litigation involving intellectual property, stockholder and other issues.

We believe that we have the product offerings, facilities, personnel, and competitive and financial resources for continued business success, but future revenues, costs, margins and profits are all influenced by a number of factors, including those discussed above, all of which are inherently difficult to forecast.

Consolidated statements of income

| Three years ended December 29, 2001 (In millions—except per share amounts) |

2001 |

2000 |

1999 |

||||||

|---|---|---|---|---|---|---|---|---|---|

| Net revenues | $ | 26,539 | $ | 33,726 | $ | 29,389 | |||

| Cost of sales | 13,487 | 12,650 | 11,836 | ||||||

| Research and development | 3,796 | 3,897 | 3,111 | ||||||

| Marketing, general and administrative | 4,464 | 5,089 | 3,872 | ||||||

| Amortization of goodwill and other acquisition-related intangibles and costs | 2,338 | 1,586 | 411 | ||||||

| Purchased in-process research and development | 198 | 109 | 392 | ||||||

| Operating costs and expenses | 24,283 | 23,331 | 19,622 | ||||||

| Operating income | 2,256 | 10,395 | 9,767 | ||||||

| Gains (losses) on equity securities, net | (466 | ) | 3,759 | 883 | |||||

| Interest and other, net | 393 | 987 | 578 | ||||||

| Income before taxes | 2,183 | 15,141 | 11,228 | ||||||

| Provision for taxes | 892 | 4,606 | 3,914 | ||||||

| Net income | $ | 1,291 | $ | 10,535 | $ | 7,314 | |||

| Basic earnings per common share | $ | 0.19 | $ | 1.57 | $ | 1.10 | |||

| Diluted earnings per common share | $ | 0.19 | $ | 1.51 | $ | 1.05 | |||

| Weighted average common shares outstanding | 6,716 | 6,709 | 6,648 | ||||||

| Weighted average common shares outstanding, assuming dilution | 6,879 | 6,986 | 6,940 | ||||||

See accompanying notes.

Consolidated balance sheets

| December 29, 2001 and December 30, 2000 (In millions-except par value) |

2001 |

2000 |

||||||

|---|---|---|---|---|---|---|---|---|

| Assets | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | 7,970 | $ | 2,976 | ||||

| Short-term investments | 2,356 | 10,497 | ||||||

| Trading assets | 1,224 | 350 | ||||||

| Accounts receivable, net of allowance for doubtful accounts of $68 ($84 in 2000) | 2,607 | 4,129 | ||||||

| Inventories | 2,253 | 2,241 | ||||||

| Deferred tax assets | 958 | 721 | ||||||

| Other current assets | 265 | 236 | ||||||

| Total current assets | 17,633 | 21,150 | ||||||

| Property, plant and equipment: | ||||||||

| Land and buildings | 10,709 | 7,416 | ||||||

| Machinery and equipment | 21,605 | 15,994 | ||||||

| Construction in progress | 2,042 | 4,843 | ||||||

| 34,356 | 28,253 | |||||||

| Less accumulated depreciation | 16,235 | 13,240 | ||||||

| Property, plant and equipment, net | 18,121 | 15,013 | ||||||

| Marketable strategic equity securities | 155 | 1,915 | ||||||

| Other long-term investments | 1,319 | 1,797 | ||||||

| Goodwill, net | 4,330 | 4,977 | ||||||

| Acquisition-related intangibles, net | 797 | 964 | ||||||

| Other assets | 2,040 | 2,129 | ||||||

| Total assets | $ | 44,395 | $ | 47,945 | ||||

Liabilities and stockholders' equity |

||||||||

| Current liabilities: | ||||||||

| Short-term debt | $ | 409 | $ | 378 | ||||

| Accounts payable | 1,769 | 2,387 | ||||||

| Accrued compensation and benefits | 1,179 | 1,696 | ||||||

| Accrued advertising | 560 | 782 | ||||||

| Deferred income on shipments to distributors | 418 | 674 | ||||||

| Other accrued liabilities | 1,247 | 1,440 | ||||||

| Income taxes payable | 988 | 1,293 | ||||||

| Total current liabilities | 6,570 | 8,650 | ||||||

| Long-term debt | 1,050 | 707 | ||||||

| Deferred tax liabilities | 945 | 1,266 | ||||||

| Commitments and contingencies | ||||||||

| Stockholders' equity: | ||||||||

| Preferred stock, $0.001 par value, 50 shares authorized; none issued | — | — | ||||||

| Common stock, $0.001 par value, 10,000 shares authorized; 6,690 issued and outstanding (6,721 in 2000) and capital in excess of par value | 8,833 | 8,486 | ||||||

| Acquisition-related unearned stock compensation | (178 | ) | (97 | ) | ||||

| Accumulated other comprehensive income | 25 | 195 | ||||||

| Retained earnings | 27,150 | 28,738 | ||||||

| Total stockholders' equity | 35,830 | 37,322 | ||||||

| Total liabilities and stockholders' equity | $ | 44,395 | $ | 47,945 | ||||

See accompanying notes.

Consolidated statements of cash flows

| Three years ended December 29, 2001 (In millions) |

2001 |

2000 |

1999 |

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Cash and cash equivalents, beginning of year | $ | 2,976 | $ | 3,695 | $ | 2,038 | |||||||

| Cash flows provided by (used for) operating activities: | |||||||||||||

| Net income | 1,291 | 10,535 | 7,314 | ||||||||||

| Adjustments to reconcile net income to net cash provided by (used for) operating activities: | |||||||||||||

| Depreciation | 4,131 | 3,249 | 3,186 | ||||||||||

| Amortization of goodwill and other acquisition-related intangibles and costs | 2,338 | 1,586 | 411 | ||||||||||

| Purchased in-process research and development | 198 | 109 | 392 | ||||||||||

| (Gains) losses on equity investments, net | 466 | (3,759 | ) | (883 | ) | ||||||||

| (Gain) loss on investment in Convera | 196 | (117 | ) | — | |||||||||

| Net loss on retirements of property, plant and equipment | 119 | 139 | 193 | ||||||||||

| Deferred taxes | (519 | ) | (130 | ) | (219 | ) | |||||||

| Tax benefit from employee stock plans | 435 | 887 | 506 | ||||||||||

| Changes in assets and liabilities: | |||||||||||||

| Trading assets | 898 | 38 | (72 | ) | |||||||||

| Accounts receivable | 1,561 | (384 | ) | 153 | |||||||||

| Inventories | 24 | (731 | ) | 169 | |||||||||

| Accounts payable | (673 | ) | 978 | 79 | |||||||||

| Accrued compensation and benefits | (524 | ) | 231 | 127 | |||||||||

| Income taxes payable | (270 | ) | (362 | ) | 726 | ||||||||

| Other assets and liabilities | (1,017 | ) | 558 | 52 | |||||||||

| Total adjustments | 7,363 | 2,292 | 4,820 | ||||||||||

| Net cash provided by operating activities | 8,654 | 12,827 | 12,134 | ||||||||||

| Cash flows provided by (used for) investing activities: | |||||||||||||

| Additions to property, plant and equipment | (7,309 | ) | (6,674 | ) | (3,403 | ) | |||||||

| Acquisitions, net of cash acquired | (883 | ) | (2,317 | ) | (2,979 | ) | |||||||

| Purchases of available-for-sale investments | (7,141 | ) | (17,188 | ) | (7,055 | ) | |||||||

| Maturities and sales of available-for-sale investments | 15,398 | 17,124 | 7,987 | ||||||||||

| Other investing activities | (260 | ) | (980 | ) | (799 | ) | |||||||

| Net cash used for investing activities | (195 | ) | (10,035 | ) | (6,249 | ) | |||||||

| Cash flows provided by (used for) financing activities: | |||||||||||||

| Increase in short-term debt, net | 23 | 138 | 69 | ||||||||||

| Additions to long-term debt | 306 | 77 | 118 | ||||||||||

| Repayment and retirement of long-term debt | (10 | ) | (46 | ) | — | ||||||||

| Proceeds from sales of shares through employee stock plans and other | 762 | 797 | 543 | ||||||||||

| Proceeds from sales of put warrants | — | — | 20 | ||||||||||

| Repurchase and retirement of common stock | (4,008 | ) | (4,007 | ) | (4,612 | ) | |||||||

| Payment of dividends to stockholders | (538 | ) | (470 | ) | (366 | ) | |||||||

| Net cash used for financing activities | (3,465 | ) | (3,511 | ) | (4,228 | ) | |||||||

| Net increase (decrease) in cash and cash equivalents | 4,994 | (719 | ) | 1,657 | |||||||||

| Cash and cash equivalents, end of year | $ | 7,970 | $ | 2,976 | $ | 3,695 | |||||||

Supplemental disclosures of cash flow information: |

|||||||||||||

| Cash paid during the year for: | |||||||||||||

| Interest | $ | 53 | $ | 43 | $ | 40 | |||||||

| Income taxes | $ | 1,208 | $ | 4,209 | $ | 2,899 | |||||||

See accompanying notes.

Consolidated statements of stockholders' equity

| |

Common stock and capital in excess of par value |

|

|

|

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Acquisition- related unearned stock compensation |

Accumulated other comprehensive income |

|

|

||||||||||||||||

| Three years ended December 29, 2001 (In millions—except per share amounts) |

Number of shares |

Amount |

Retained earnings |

Total |

||||||||||||||||

| Balance at December 26, 1998 | 6,631 | $ | 4,822 | $ | — | $ | 603 | $ | 17,952 | $ | 23,377 | |||||||||

Components of comprehensive income: |

||||||||||||||||||||

| Net income | — | — | — | — | 7,314 | 7,314 | ||||||||||||||

| Change in net unrealized gain on available-for-sale investments, net of tax | — | — | — | 3,188 | — | 3,188 | ||||||||||||||

| Total comprehensive income | 10,502 | |||||||||||||||||||

| Proceeds from sales of shares through employee stock plans, tax benefit of $506 and other | 112 | 1,049 | — | — | — | 1,049 | ||||||||||||||

| Proceeds from sales of put warrants | — | 20 | — | — | — | 20 | ||||||||||||||

| Reclassification of put warrant obligation, net | — | 7 | — | — | 64 | 71 | ||||||||||||||

| Repurchase and retirement of common stock | (143 | ) | (1,076 | ) | — | — | (3,536 | ) | (4,612 | ) | ||||||||||

| Issuance of common stock and assumption of stock options in connection with acquisitions | 69 | 2,494 | — | — | — | 2,494 | ||||||||||||||

| Cash dividends declared ($0.055 per share) | — | — | — | — | (366 | ) | (366 | ) | ||||||||||||

| Balance at December 25, 1999 | 6,669 | 7,316 | — | 3,791 | 21,428 | 32,535 | ||||||||||||||

| Components of comprehensive income: | ||||||||||||||||||||

| Net income | — | — | — | — | 10,535 | 10,535 | ||||||||||||||

| Change in net unrealized gain on available-for-sale investments, net of tax | — | — | — | (3,596 | ) | — | (3,596 | ) | ||||||||||||

| Total comprehensive income | 6,939 | |||||||||||||||||||

| Proceeds from sales of shares through employee stock plans, tax benefit of $887 and other | 116 | 1,687 | — | — | (3 | ) | 1,684 | |||||||||||||

| Reclassification of put warrant obligation, net | — | 35 | — | — | 95 | 130 | ||||||||||||||

| Issuance of common stock and assumption of stock options in connection with acquisitions | 3 | 401 | (123 | ) | — | — | 278 | |||||||||||||

| Amortization of acquisition-related unearned stock compensation | — | — | 26 | — | — | 26 | ||||||||||||||

| Conversion of subordinated notes | 7 | 207 | — | — | — | 207 | ||||||||||||||

| Repurchase and retirement of common stock | (74 | ) | (1,160 | ) | — | — | (2,847 | ) | (4,007 | ) | ||||||||||

| Cash dividends declared ($0.070 per share) | — | — | — | — | (470 | ) | (470 | ) | ||||||||||||

| Balance at December 30, 2000 | 6,721 | 8,486 | (97 | ) | 195 | 28,738 | 37,322 | |||||||||||||

| Components of comprehensive income: | ||||||||||||||||||||

| Net income | — | — | — | — | 1,291 | 1,291 | ||||||||||||||

| Change in net unrealized gain on available-for-sale investments, net of tax | — | — | — | (163 | ) | — | (163 | ) | ||||||||||||

| Change in net unrealized loss on derivatives, net of tax | — | — | — | (7 | ) | — | (7 | ) | ||||||||||||

| Total comprehensive income | 1,121 | |||||||||||||||||||

| Proceeds from sales of shares through employee stock plans, tax benefit of $435 and other | 81 | 1,197 | — | — | — | 1,197 | ||||||||||||||

| Issuance of common stock and aassumption of stock options in connection with acquisitions, net | 21 | 817 | (255 | ) | — | — | 562 | |||||||||||||

| Amortization of acquisition-related unearned stock compensation | — | — | 174 | — | — | 174 | ||||||||||||||

| Repurchase and retirement of common stock | (133 | ) | (1,667 | ) | — | — | (2,341 | ) | (4,008 | ) | ||||||||||

| Cash dividends declared ($0.080 per share) | — | — | — | — | (538 | ) | (538 | ) | ||||||||||||

| Balance at December 29, 2001 | 6,690 | $ | 8,833 | $ | (178 | ) | $ | 25 | $ | 27,150 | $ | 35,830 | ||||||||

See accompanying notes.

Notes to consolidated financial statements

Accounting policies

Fiscal year > Intel Corporation has a fiscal year that ends on the last Saturday in December. Fiscal year 2001, a 52-week year, ended on December 29, 2001. Fiscal year 2000 was a 53-week year that ended on December 30, while 1999, a 52-week year, ended on December 25. The next 53-week year will end on December 31, 2005.

Basis of presentation > The consolidated financial statements include the accounts of Intel and its wholly owned subsidiaries. Intercompany accounts and transactions have been eliminated. Partially owned equity affiliates are accounted for under the equity method. Accounts denominated in non-U.S. currencies have been remeasured using the U.S. dollar as the functional currency.

The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and judgments that affect the amounts reported in the financial statements and accompanying notes. The critical accounting policies that require management's most significant estimates and judgments include valuation of non-marketable equity securities, valuation of inventory, and the assessment of recoverability of goodwill and other intangible assets. The actual results experienced by the company may differ materially from management's estimates.

Recent accounting pronouncements > In July 2001, the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Standards (SFAS) No. 141, "Business Combinations," and SFAS No. 142, "Goodwill and Other Intangible Assets." Beginning in the first quarter of fiscal 2002, the company will no longer amortize goodwill, but will perform impairment tests annually, or earlier if indicators of potential impairment exist. All other intangible assets continue to be amortized over their estimated useful lives. In conjunction with the implementation of SFAS No. 142, the company has completed a goodwill impairment review as of the beginning of fiscal 2002 using a fair-value based approach in accordance with provisions of that standard and found no impairment. Based on acquisitions completed as of June 30, 2001, application of the goodwill non-amortization provisions is expected to result in a decrease in amortization of approximately $1.6 billion for fiscal year 2002.

Accounting change > Effective as of the beginning of 2001, the company adopted SFAS No. 133, "Accounting for Derivative Instruments and Hedging Activities," as amended, which requires the company to recognize all derivative instruments as either assets or liabilities on the balance sheet at fair value. The accounting for gains or losses from changes in fair value of a derivative instrument depends on whether it has been designated and qualifies as part of a hedging relationship, as well as on the type of hedging relationship.

The cumulative effect of the adoption of SFAS No. 133 was an increase in income before taxes of $45 million, which is included in interest and other, net for 2001. The adoption did not have a material effect on other comprehensive income.

Cash and cash equivalents > Highly liquid debt securities with insignificant interest rate risk and with original maturities of three months or less are classified as cash and cash equivalents.

Investments > The company's investments consist of:

Trading assets. The company elects to classify as trading assets certain marketable debt and equity securities. The interest, currency and/or equity market risks inherent in these investments are generally mitigated through the use of derivative instruments. Also included in trading assets is a marketable equity portfolio held to generate returns that offset changes in liabilities related to certain deferred compensation arrangements. Trading assets are stated at fair value, with gains or losses resulting from changes in fair value recognized currently in earnings. For marketable debt securities, gains or losses from changes in fair value, offset by losses or gains on related derivatives, are included in interest and other, net. For marketable equity securities having related derivative instruments, gains or losses from changes in fair value, offset or partially offset by losses or gains on the derivatives, are included in gains (losses) on equity securities, net. For other marketable equity securities related to deferred compensation arrangements, gains or losses from changes in fair value, offset by losses or gains on the related liabilities, are included in interest and other, net.

Available-for-sale investments. Investments designated as available-for-sale include marketable debt and equity securities. Investments that are designated as available-for-sale as of the balance sheet date are reported at fair value, with unrealized gains and losses, net of tax, recorded in stockholders' equity. The cost of securities sold is based on the specific identification method. Realized gains and losses on the sale of debt securities are recorded in interest and other, net. Realized gains or losses on the sale or exchange of equity securities and declines in value judged to be other than temporary are recorded in gains (losses) on equity securities, net. Marketable equity securities are presumed to be impaired if the fair value is less than the cost basis for six months, absent compelling evidence to the contrary.

Debt securities with original maturities greater than three months and remaining maturities less than one year are classified as short-term investments. Debt securities with remaining maturities greater than one year are classified as other long-term investments.

The company acquires certain equity investments for the promotion of business and strategic objectives, and to the extent these investments continue to have strategic value, the company typically does not attempt to reduce or eliminate the inherent market risks. The marketable portion of these investments is classified separately as marketable strategic equity securities.

Non-marketable equity securities and other investments. Non-marketable equity securities and other investments are accounted for at historical cost or, if Intel has significant influence over the investee, using the equity method. The company's proportionate share of income or losses from investments accounted for under the equity method and any gain or loss on disposal is recorded in interest and other, net. Non-marketable equity securities and other investments, as well as equity-method investments, are included in other assets. Non-marketable equity securities are subject to a periodic impairment review, including assessment of the investee's financial condition, the existence of subsequent rounds of financing and the impact of any relevant contractual preferences, as well as the investee's historical results of operations, projected results and cash flows. Impairment of non-marketable equity investments is recorded in gains (losses) on equity securities, net.

Securities lending > The company, from time to time, enters into secured lending agreements with financial institutions, generally to facilitate hedging transactions. Selected securities are loaned for short periods of time and are secured by collateral in the form of cash or securities. The loaned securities continue to be carried as investment assets on the balance sheet. Cash collateral is recorded as an asset with a corresponding liability. For lending agreements collateralized by securities, the collateral is not recorded as an asset or a liability, unless the collateral is repledged (see "Short-term debt" under "Borrowings").

Fair values of financial instruments > Fair values of cash equivalents approximate cost due to the short period of time to maturity. Fair values of short-term investments, trading assets, marketable strategic equity securities, other long-term investments, certain non-marketable investments, short-term debt, long-term debt, swaps, currency forward contracts, equity options and warrants are based on quoted market prices or pricing models using current market rates. Debt securities are generally valued using discounted cash flows in an industry-standard yield-curve model based on LIBOR. Equity options and warrants are priced using a Black-Scholes option valuation model. For certain non-marketable equity securities, fair value is estimated based on prices recently paid for shares in that company. All of the estimated fair values are management's estimates; however, when there is no readily available market, the fair values may not necessarily represent the amounts that could be realized in a current transaction.

Derivative financial instruments > The company's primary objective for holding derivative financial instruments is to manage interest rate, non-U.S. currency and some equity market risks. The company's derivative instruments are recorded at fair value and are included in other current assets, other assets, other accrued liabilities or long-term debt. The company's accounting policies for these instruments are based on whether they meet the company's criteria for designation as hedging transactions, either as cash flow or fair value hedges. A hedge of the exposure to variability in the cash flows of an asset or a liability, or of a forecasted transaction, is referred to as a cash flow hedge. A hedge of the exposure to changes in fair value of an asset or a liability, or of an unrecognized firm commitment, is referred to as a fair value hedge. The criteria for designating a derivative as a hedge include the instrument's effectiveness in risk reduction and in most cases a one-to-one matching of the derivative instrument to its underlying transaction. Gains and losses on derivatives that are not designated as hedges for accounting purposes are recognized currently in earnings, and generally offset changes in the values of related assets, liabilities or debt.

As part of its strategic investment program, the company also acquires equity derivative instruments, such as warrants, that are not designated as hedging instruments. The gains or losses from changes in fair values of these equity derivatives are recognized in gains (losses) on equity securities, net.

Currency risk. The company transacts business in various non-U.S. currencies, primarily Japanese yen and certain other Asian and European currencies. The company has established revenue, expense and balance sheet risk management programs to protect against reductions in value and volatility of future cash flows caused by changes in exchange rates. The company uses currency forward contracts, currency options, borrowings in various currencies and currency interest rate swaps in these risk management programs. These programs reduce, but do not always entirely eliminate, the impact of currency exchange movements.

Currency forward contracts and currency options that are used to hedge exposures to variability in anticipated non-U.S.-dollar- denominated cash flows are designated as cash flow hedges. The maturities of these instruments are generally less than 12 months. For these derivatives, the effective portion of the gain or loss is reported as a component of other comprehensive income in stockholders' equity and is reclassified into earnings in the same period or periods in which the hedged transaction affects earnings, and within the same income statement line item. The ineffective portion of the gain or loss on the derivative in excess of the cumulative change in the present value of future cash flows of the hedged item, if any, is recognized in interest and other, net during the period of change. Prior to the adoption of SFAS No. 133, derivatives hedging the currency risk of future cash flows were not recognized on the balance sheet.

Currency interest rate swaps and currency forward contracts are used to offset the currency risk of non-U.S.-dollar-denominated debt securities classified as trading assets, as well as other assets and liabilities denominated in various currencies. Changes in fair value of the underlying assets and liabilities are generally offset by the changes in fair value of the related derivatives, with the resulting net gain or loss, if any, recorded in interest and other, net.

Interest rate risk. The company's primary objective for holding investments in debt securities is to preserve principal while maximizing yields, without significantly increasing risk. To achieve this objective, the returns on a substantial majority of the company's investments in long-term fixed-rate marketable debt securities are swapped to U.S. dollar LIBOR-based returns, using interest rate swaps and currency interest rate swaps in transactions that are not designated as hedges for accounting purposes. The floating interest rates on the swaps are reset on a monthly, quarterly or semiannual basis. Changes in fair value of the debt securities classified as trading assets are generally offset by changes in fair value of the related derivatives, resulting in negligible net impact. The net gain or loss, if any, is recorded in interest and other, net.

The company also enters into interest rate swap agreements to modify the interest characteristics of its outstanding long-term debt. These transactions are designated as fair value hedges. The gains or losses from the changes in fair value of the interest rate swaps, as well as the offsetting change in the hedged fair value of the long-term debt, are recognized in interest expense. Prior to the adoption of SFAS No. 133, interest rate swaps related to long-term debt were not recognized on the balance sheet, nor were the changes in the hedged fair value of the debt.