Exhibit 99.4

| Exhibit 99.4

|

investor meeting

2015 SANTA CLARA

Diane Bryant

Senior Vice President & General Manager

Data Center Group

|

|

| 2 |

|

Key Messages

Adoption of cloud computing growing and transforming all segments

Non-CPU products contribute meaningful growth

Fundamental growth drivers remain strong

*Forecast is based on current expectations given available information and is subject to change without notice

Source: Intel

|

|

| 3 |

|

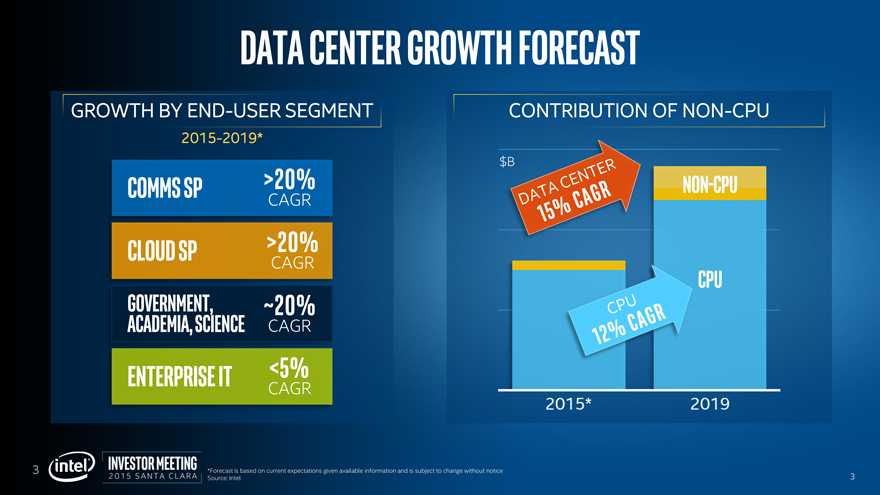

Data Center Growth Forecast

*Forecast is based on current expectations given available information and is subject to change without notice

Source: Intel

CONTRIBUTION OF NON-CPU

GROWTH BY END-USER SEGMENT

2015-2019*

$B

CPU

NON-CPU

CPU

12% CAGR

DATA CENTER

15% CAGR

>20%

CAGR

COMMS SP

CLOUD SP

>20%

CAGR

GOVERNMENT,

ACADEMIA, SCIENCE

~20%

CAGR

ENTERPRISE IT

<5%

CAGR

|

|

| 4 |

|

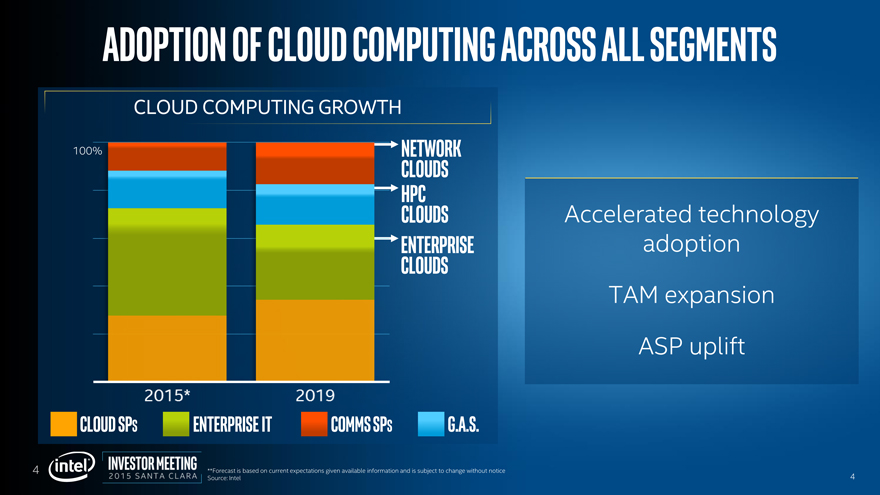

Accelerated technology

adoption

TAM expansion

ASP uplift

Adoption of Cloud Computing Across All Segments

CLOUD COMPUTING GROWTH

ENTERPRISE

CLOUDS

HPC

CLOUDS

NETWORK

CLOUDS

100%

ENTERPRISE IT

COMMS SPS

CLOUD SPS

G.A.S.

**Forecast is based on current expectations given available information and is subject to change without notice

Source: Intel

|

|

| 5 |

|

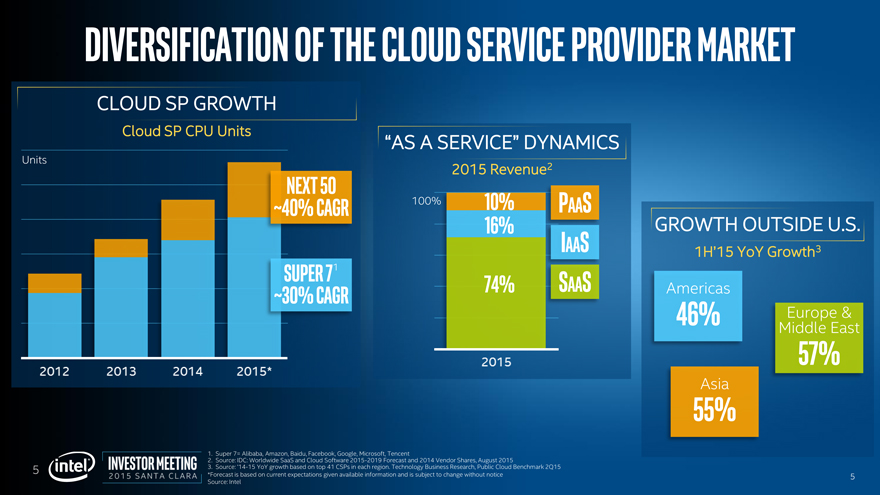

Diversification of the Cloud Service Provider Market

1. Super 7= Alibaba, Amazon, Baidu, Facebook, Google, Microsoft, Tencent

2. Source: IDC: Worldwide SaaS and Cloud Software 2015-2019 Forecast and 2014 Vendor Shares, August 2015

3. Source: ‘14-15 YoYgrowth based on top 41 CSPs in each region. Technology Business Research, Public Cloud Benchmark 2Q15

2015 Revenue2

“AS A SERVICE” DYNAMICS

100%

10%

16%

74%

IaaS

SaaS

PaaS

Europe &

Middle East

57%

Asia

55%

Americas46%

GROWTH OUTSIDE U.S.

1H’15 YoYGrowth3

Cloud SP CPU Units

CLOUD SP GROWTH

Units

*Forecast is based on current expectations given available information and is subject to change without notice

Source: Intel

Next 50

~40% CAGR

Super 71

~30% CAGR

|

|

| 6 |

|

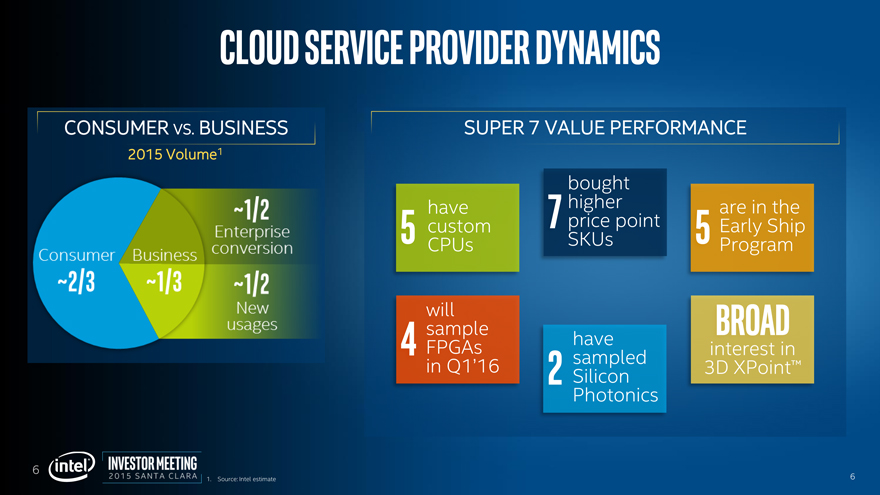

Cloud Service Provider Dynamics

SUPER 7 VALUE PERFORMANCE

| 5 |

|

have

custom

CPUs

| 5 |

|

are in the

Early Ship

Program

| 4 |

|

will

sample

FPGAs

in Q1’16

Broad

interest in

3D XPoint™

| 2 |

|

have

sampled

Silicon

Photonics

2015 Volume1

CONSUMER VS.BUSINESS

1.Source: Intel estimate

| 7 |

|

bought

higher

price point

SKUs

|

|

| 7 |

|

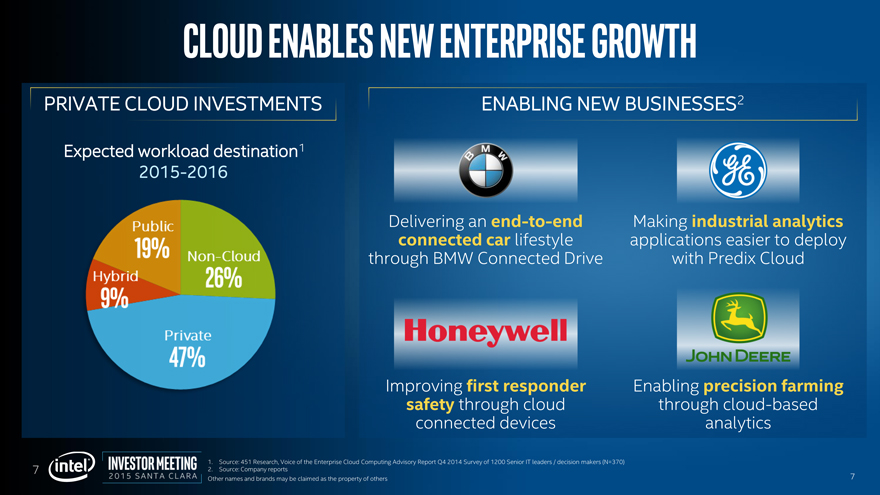

Cloud Enables new Enterprise Growth

ENABLING NEW BUSINESSES2

Improving first responder

safetythrough cloud

connected devices

Delivering an end-to-end

connected car lifestylethrough BMW Connected Drive

Other names and brands may be claimed as the property of others

PRIVATE CLOUD INVESTMENTS

2015-2016

Expected workload destination1

1.Source: 451 Research, Voice of the Enterprise Cloud Computing Advisory Report Q4 2014 Survey of 1200 Senior IT leaders / decision makers(N=370)

2.Source: Company reports

Making industrial analytics

applications easier to deploy

with Predix Cloud

Enabling precision farming

through cloud-based

analytics

|

|

| 8 |

|

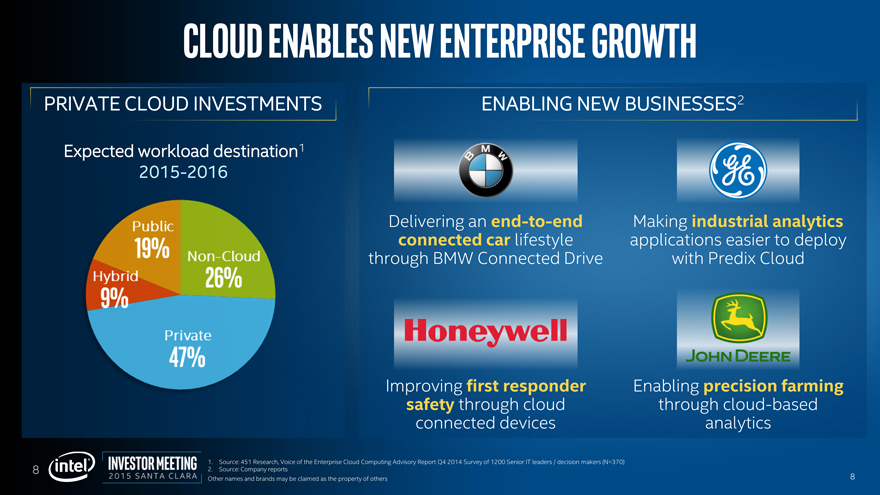

Cloud Enables new Enterprise Growth

ENABLING NEW BUSINESSES2

Improving first responder

safetythrough cloud

connected devices

Delivering an end-to-end

connected car lifestylethrough BMW Connected Drive

Other names and brands may be claimed as the property of others

PRIVATE CLOUD INVESTMENTS

2015-2016

Expected workload destination1

1.Source: 451 Research, Voice of the Enterprise Cloud Computing Advisory Report Q4 2014 Survey of 1200 Senior IT leaders / decision makers(N=370)

2.Source: Company reports

Making industrial analytics

applications easier to deploy

with Predix Cloud

Enabling precision farming

through cloud-based

analytics

|

|

9

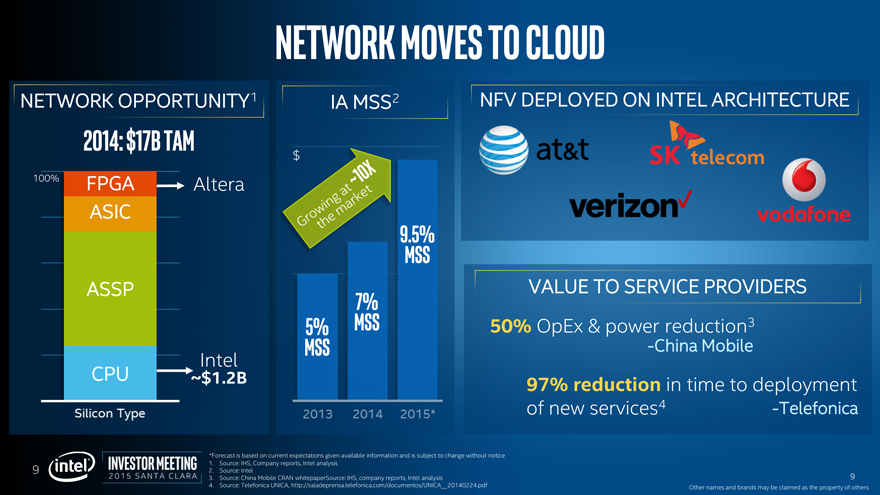

Network Moves to Cloud

VALUE TO SERVICE PROVIDERS

Other names and brands may be claimed as the property of others

NETWORK OPPORTUNITY1

1.Source: IHS, Company reports, Intel analysis

2.Source: Intel

3.Source: China Mobile CRAN whitepaperSource: IHS, company reports, Intel analysis

4.Source: Telefonica UNICA, http://saladeprensa.telefonica.com/documentos/UNICA__20140224.pdf

2014: $17B TAM

NFV DEPLOYED ON INTEL ARCHITECTURE

FPGA

ASIC

CPU

ASSP

Altera

Intel

~$1.2B

Growing at

~10

X

t

he market

5%

MSS

7%

MSS

9.5%

MSS

$

IA MSS2

97% reduction in time to deployment

of new services4

-Telefonica

50% OpEx& power reduction3

-China Mobile

*Forecast is based on current expectations given available information and is subject to change without notice

100%

|

|

10

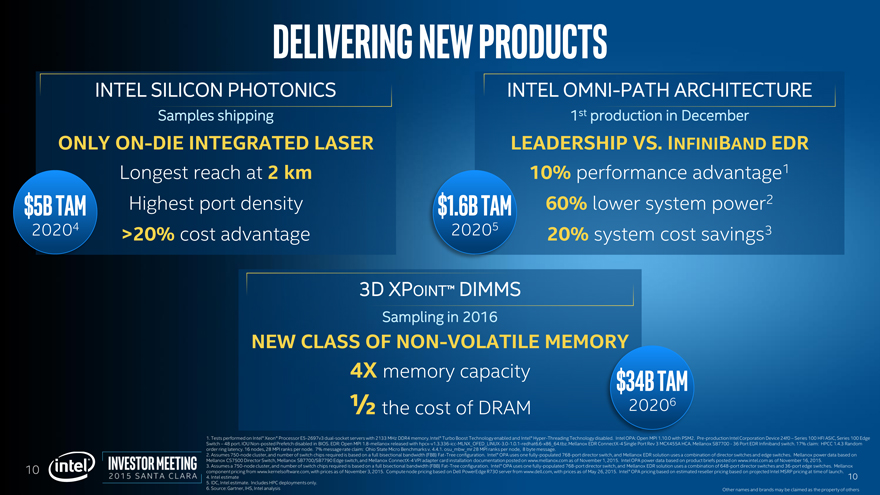

Delivering New Products

INTEL SILICON PHOTONICS

Samples shipping

Longest reach at 2 km

Highest port density

>20% cost advantage

ONLY ON-DIE INTEGRATED LASER

INTEL OMNI-PATH ARCHITECTURE

1stproduction in December

10% performance advantage1

60% lower system power2

20% system cost savings3

LEADERSHIP VS. INFINIBANDEDR

1. Tests performed on Intel® Xeon® Processor E5-2697v3 dual-socket servers with 2133 MHz DDR4 memory. Intel® Turbo Boost Technology enabled and Intel® Hyper-Threading Technology disabled. Intel OPA: Open MPI 1.10.0 with PSM2. Pre-production Intel Corporation Device 24f0 –Series 100 HFI ASIC, Series 100 Edge

Switch –48 port. IOU Non-posted Prefetchdisabled in BIOS. EDR: Open MPI 1.8-mellanox released with hpcx-v1.3.336-icc-MLNX_OFED_LINUX-3.0-1.0.1-redhat6.6-x86_64.tbz. MellanoxEDR ConnectX-4 Single Port Rev 3 MCX455A HCA. MellanoxSB7700 -36 Port EDR Infinibandswitch. 17% claim: HPCC 1.4.3 Random

order ring latency. 16 nodes, 28 MPI ranks per node. 7% message rate claim: Ohio State Micro Benchmarks v. 4.4.1. osu_mbw_mr28 MPI ranks per node, 8 byte message.

2. Assumes 750-node cluster, and number of switch chips required is based on a full bisectional bandwidth (FBB) Fat-Tree configuration. Intel® OPA uses one fully-populated 768-port director switch, and MellanoxEDR solution uses a combination of director switches and edge switches. Mellanoxpower data based on

MellanoxCS7500 Director Switch, MellanoxSB7700/SB7790 Edge switch, and MellanoxConnectX-4 VPI adapter card installation documentation posted on www.mellanox.com as of November 1, 2015. Intel OPA power databased on product briefs posted on www.intel.com as of November 16, 2015.

3. Assumes a 750-node cluster, and number of switch chips required is based on a full bisectional bandwidth (FBB) Fat-Tree configuration. Intel® OPA uses one fully-populated 768-port director switch, and MellanoxEDR solution uses a combination of 648-port director switches and 36-port edge switches. Mellanoxcomponent pricing from www.kernelsoftware.com, with prices as of November 3, 2015. Compute node pricing based on Dell PowerEdgeR730 server from www.dell.com, with prices as of May 26, 2015. Intel® OPA pricing based on estimated reseller pricing based onprojected Intel MSRP pricing at time of launch.

4. Intel estimate

5. IDC, Intel estimate. Includes HPC deployments only.

6. Source: Gartner, IHS, Intel analysis

$1.6B TAM

20205

3D XPOINT™DIMMS

Sampling in 2016

4X memory capacity

1/2the cost of DRAM

NEW CLASS OF NON-VOLATILE MEMORY

$34B TAM

20206

Other names and brands may be claimed as the property of others

$5B TAM

20204

|

|

11

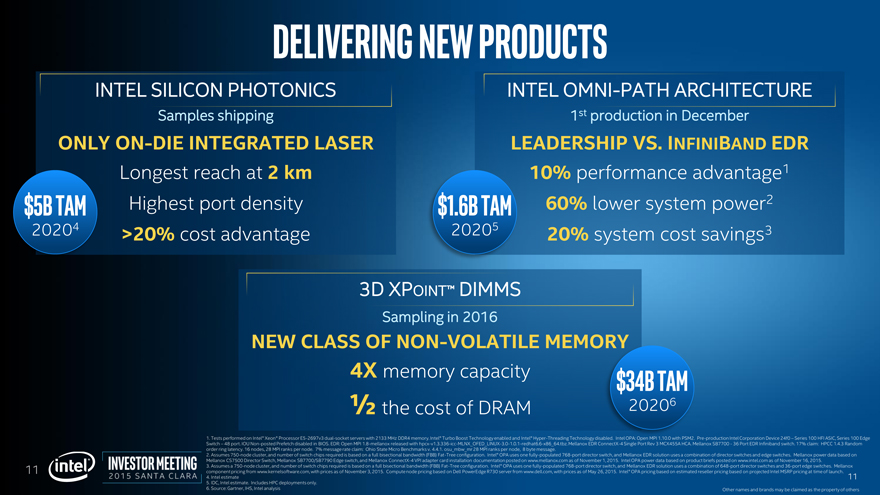

Delivering New Products

INTEL SILICON PHOTONICS

Samples shipping

Longest reach at 2 km

Highest port density

>20% cost advantage

ONLY ON-DIE INTEGRATED LASER

INTEL OMNI-PATH ARCHITECTURE

1stproduction in December

10% performance advantage1

60% lower system power2

20% system cost savings3

LEADERSHIP VS. INFINIBANDEDR

1. Tests performed on Intel® Xeon® Processor E5-2697v3 dual-socket servers with 2133 MHz DDR4 memory. Intel® Turbo Boost Technology enabled and Intel® Hyper-Threading Technology disabled. Intel OPA: Open MPI 1.10.0 with PSM2. Pre-production Intel Corporation Device 24f0 –Series 100 HFI ASIC, Series 100 Edge

Switch –48 port. IOU Non-posted Prefetchdisabled in BIOS. EDR: Open MPI 1.8-mellanox released with hpcx-v1.3.336-icc-MLNX_OFED_LINUX-3.0-1.0.1-redhat6.6-x86_64.tbz. MellanoxEDR ConnectX-4 Single Port Rev 3 MCX455A HCA. MellanoxSB7700 -36 Port EDR Infinibandswitch. 17% claim: HPCC 1.4.3 Random

order ring latency. 16 nodes, 28 MPI ranks per node. 7% message rate claim: Ohio State Micro Benchmarks v. 4.4.1. osu_mbw_mr28 MPI ranks per node, 8 byte message.

2. Assumes 750-node cluster, and number of switch chips required is based on a full bisectional bandwidth (FBB) Fat-Tree configuration. Intel® OPA uses one fully-populated 768-port director switch, and MellanoxEDR solution uses a combination of director switches and edge switches. Mellanoxpower data based on

MellanoxCS7500 Director Switch, MellanoxSB7700/SB7790 Edge switch, and MellanoxConnectX-4 VPI adapter card installation documentation posted on www.mellanox.com as of November 1, 2015. Intel OPA power databased on product briefs posted on www.intel.com as of November 16, 2015.

3. Assumes a 750-node cluster, and number of switch chips required is based on a full bisectional bandwidth (FBB) Fat-Tree configuration. Intel® OPA uses one fully-populated 768-port director switch, and MellanoxEDR solution uses a combination of 648-port director switches and 36-port edge switches. Mellanoxcomponent pricing from www.kernelsoftware.com, with prices as of November 3, 2015. Compute node pricing based on Dell PowerEdgeR730 server from www.dell.com, with prices as of May 26, 2015. Intel® OPA pricing based on estimated reseller pricing based onprojected Intel MSRP pricing at time of launch.

4. Intel estimate

5. IDC, Intel estimate. Includes HPC deployments only.

6. Source: Gartner, IHS, Intel analysis

$1.6B TAM

20205

3D XPOINT™DIMMS

Sampling in 2016

4X memory capacity

1/2the cost of DRAM

NEW CLASS OF NON-VOLATILE MEMORY

$34B TAM

20206

Other names and brands may be claimed as the property of others

$5B TAM

20204

|

|

12

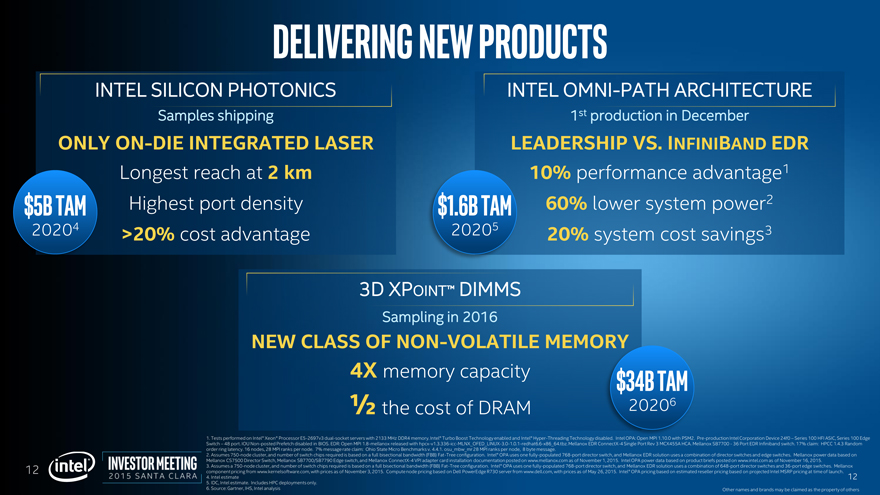

Delivering New Products

INTEL SILICON PHOTONICS

Samples shipping

Longest reach at 2 km

Highest port density

>20% cost advantage

ONLY ON-DIE INTEGRATED LASER

INTEL OMNI-PATH ARCHITECTURE

1stproduction in December

10% performance advantage1

60% lower system power2

20% system cost savings3

LEADERSHIP VS. INFINIBANDEDR

1. Tests performed on Intel® Xeon® Processor E5-2697v3 dual-socket servers with 2133 MHz DDR4 memory. Intel® Turbo Boost Technology enabled and Intel® Hyper-Threading Technology disabled. Intel OPA: Open MPI 1.10.0 with PSM2. Pre-production Intel Corporation Device 24f0 –Series 100 HFI ASIC, Series 100 Edge

Switch –48 port. IOU Non-posted Prefetchdisabled in BIOS. EDR: Open MPI 1.8-mellanox released with hpcx-v1.3.336-icc-MLNX_OFED_LINUX-3.0-1.0.1-redhat6.6-x86_64.tbz. MellanoxEDR ConnectX-4 Single Port Rev 3 MCX455A HCA. MellanoxSB7700 -36 Port EDR Infinibandswitch. 17% claim: HPCC 1.4.3 Random

order ring latency. 16 nodes, 28 MPI ranks per node. 7% message rate claim: Ohio State Micro Benchmarks v. 4.4.1. osu_mbw_mr28 MPI ranks per node, 8 byte message.

2. Assumes 750-node cluster, and number of switch chips required is based on a full bisectional bandwidth (FBB) Fat-Tree configuration. Intel® OPA uses one fully-populated 768-port director switch, and MellanoxEDR solution uses a combination of director switches and edge switches. Mellanoxpower data based on

MellanoxCS7500 Director Switch, MellanoxSB7700/SB7790 Edge switch, and MellanoxConnectX-4 VPI adapter card installation documentation posted on www.mellanox.com as of November 1, 2015. Intel OPA power databased on product briefs posted on www.intel.com as of November 16, 2015.

3. Assumes a 750-node cluster, and number of switch chips required is based on a full bisectional bandwidth (FBB) Fat-Tree configuration. Intel® OPA uses one fully-populated 768-port director switch, and MellanoxEDR solution uses a combination of 648-port director switches and 36-port edge switches. Mellanoxcomponent pricing from www.kernelsoftware.com, with prices as of November 3, 2015. Compute node pricing based on Dell PowerEdgeR730 server from www.dell.com, with prices as of May 26, 2015. Intel® OPA pricing based on estimated reseller pricing based onprojected Intel MSRP pricing at time of launch.

4. Intel estimate

5. IDC, Intel estimate. Includes HPC deployments only.

6. Source: Gartner, IHS, Intel analysis

$1.6B TAM

20205

3D XPOINT™DIMMS

Sampling in 2016

4X memory capacity

1/2the cost of DRAM

NEW CLASS OF NON-VOLATILE MEMORY

$34B TAM

20206

Other names and brands may be claimed as the property of others

$5B TAM

20204

|

|

13

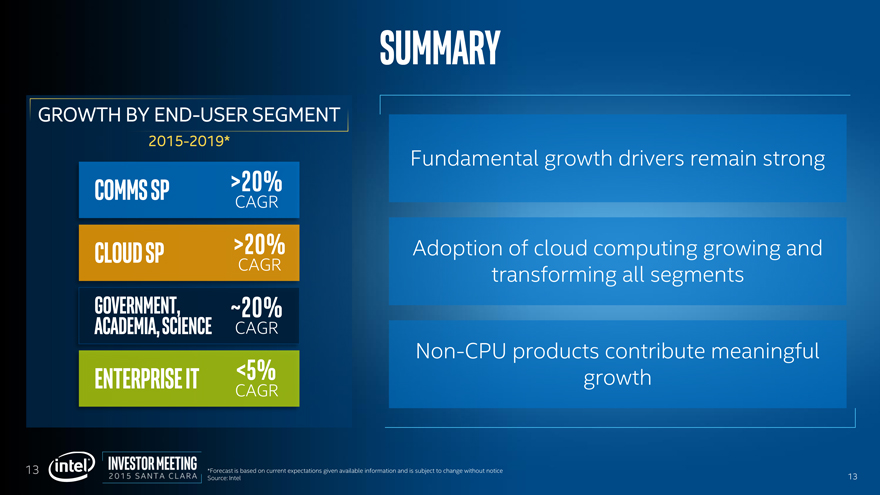

Summary

Adoption of cloud computing growing and

transforming all segments

Non-CPU products contribute meaningful

growth

Fundamental growth drivers remain strong

GROWTH BY END-USER SEGMENT

2015-2019*

>20%

CAGR

COMMS SP

CLOUD SP

>20%

CAGR

GOVERNMENT,

ACADEMIA, SCIENCE

~20%

CAGR

ENTERPRISE IT

<5%

CAGR

*Forecast is based on current expectations given available information and is subject to change without notice

Source: Intel

|

|

investor meeting

2015 SANTA CLARA

|

|

Risk Factors

The statements in this presentation and other commentary that refer to future plans and expectations are forward-looking statements that involve a number of risks and uncertainties. Words such as “anticipates,” “expects,” “intends,” “goals,” “plans,” “believes,” “seeks,” “estimates,” “continues,” “may,” “will,” “should,” and variations of such words and similar expressions are intended to identify such forward-looking statements. Statements that refer to or are based on projections, uncertain events or assumptions also identify forward-looking statements. Many factors could affect Intel’s actual results, and variances from Intel’s current expectations regarding such factors could cause actual results to differ materially from those expressed in these forward-looking statements. Intel presently considers the following to be important factors that could cause actual results to differ materially from the company’s expectations. Demand for Intel’s products is highly variable and could differ from expectations due to factors including changes in business and economic conditions; consumer confidence or income levels; the introduction, availability and market acceptance of Intel’s products, products used together with Intel products and competitors’ products; competitive and pricing pressures, including actions taken by competitors; supply constraints and other disruptions affecting customers; changes in customer order patterns including order cancellations; and changes in the level of inventory at customers. Intel’s gross margin percentage could vary significantly from expectations based on capacity utilization; variations in inventory valuation, including variations related to the timing of qualifying products for sale; changes in revenue levels; segment product mix; the timing and execution of the manufacturing ramp and associated costs; excess or obsolete inventory; changes in unit costs; defects or disruptions in the supply of materials or resources; and product manufacturing quality/yields. Variations in gross margin may also be caused by the timing of Intel product introductions and related expenses, including marketing expenses, and Intel’s ability to respond quickly to technological developments and to introduce new products or incorporate new features into existing products, which may result in restructuring and asset impairment charges. Intel’s results could be affected by adverse economic, social, political and physical/infrastructure conditions in countries where Intel, its customers or its suppliers operate, including military conflict and other security risks, natural disasters, infrastructure disruptions, health concerns and fluctuations in currency exchange rates. Results may also be affected by the formal or informal imposition by countries of new or revised export and/or import and doing-business regulations, which could be changed without prior notice. Intel operates in highly competitive industries and its operations have high costs that are either fixed or difficult to reduce in the short term. The amount, timing and execution of Intel’s stock repurchase program could be affected by changes in Intel’s priorities for the use of cash, such as operational spending, capital spending, acquisitions, and as a result of changes to Intel’s cash flows or changes in tax laws. Product defects or errata (deviations from published specifications) may adversely impact our expenses, revenues and reputation. Intel’s results could be affected by litigation or regulatory matters involving intellectual property, stockholder, consumer, antitrust, disclosure and other issues. An unfavorable ruling could include monetary damages or an injunction prohibiting Intel from manufacturing or selling one or more products, precluding particular business practices, impacting Intel’s ability to design its products, or requiring other remedies such as compulsory licensing of intellectual property. Intel’s results may be affected by the timing of closing of acquisitions, divestitures and other significant transactions. In addition, risks associated with our pending acquisition of Altera are described in the “Forward Looking Statements” paragraph of Intel’s press release dated June 1, 2015, which risk factors are incorporated by reference herein. A detailed discussion of these and other factors that could affect Intel’s results is included in Intel’s SEC filings, including the company’s most recent reports on Form 10-Q, Form 10-K and earnings release.