Exhibit 99.6

| Exhibit 99.6

|

Investor MeetingFEBRUARY 2017

|

|

Bob Swan

Chief financial officer

|

|

DISCLOSURES

This presentation contains non-GAAP financial measures relating to our performance. You can find the reconciliation of these measures to the most directly comparable GAAP financial measure in the Appendix at the end of this presentation. The non-GAAP financial measures disclosed by Intel should not be considered a substitute for, or superior to, the financial measures prepared in accordance with GAAP. Please refer to “Explanation of Non-GAAP Measures” in Intel’s quarterly earnings release for a detailed explanation of the adjustments made to the comparable GAAP measures, the ways management uses the non-GAAP measures, and the reasons why management believes the non-GAAP measures provide investors with useful supplemental information.

Statements in this presentation that refer to Business Outlook, forecast, future plans and expectations are forward-looking statements that involve a number of risks and uncertainties. Words such as “anticipates,” “expects,” “intends,” “goals,” “plans,” “believes,” “seeks,” “estimates,” “continues,” “may,” “will,” “would,” “should,” “could,” and variations of such words and similar expressions are intended to identify such forward-looking statements. Statements that refer to or are based on projections, uncertain events or assumptions also identify forward-looking statements. Such statements are based on management’s expectations as of February 9, 2017 and involve many risks and uncertainties that could cause actual results to differ materially from those expressed or implied in these forward-looking statements. Important factors that could cause actual results to differ materially from the company’s expectations are set in Intel’s earnings release dated January 26, 2017, which is included as an exhibit to Intel’s Form 8-K furnished to the SEC on such date. Additional information regarding these and other factors that could affect Intel’s results is included in Intel’s SEC filings, including the company’s most recent reports on Forms 10-K and 10-Q. Copies of Intel’s Form 10-K, 10-Q and 8-K reports may be obtained by visiting our Investor Relations website at www.intc.com or the SEC’s website at www.sec.gov.

3

|

|

A BRIEF RECAP

Industry leader

Expanding TAM… investing in the future Industry trends playing to our strengths Great portfolio of businesses and assets

4

|

|

INDUSTRY LEADER

IDM Advantage Moore’s Law Leadership World Class Products

5

|

|

WE HAVE A GREAT SET OF BUSINESSES WITH LEADING POSITIONS

CCG DCG TG PSG NSG

6

|

|

A SIGNIFICANT TRANSFORMATION…

Moving from PC Centric to powering the cloud and billions of smart, connected devices

CCG Revenue Growth Business Revenue

CAGR

13% CAGR

2014 2016 20142016

CCG: Excellent performance in a declining market

Growth Business: Strong growth… continue to invest

Growth business revenue includes DCG, IOTG, NSG, PSG and all other revenue. This excludes revenue from Intel Security.

7

|

|

SHIFTING OUR RESOURCES

Reduction… Reallocation… Reinvesting… Repositioning

$ 22B Spending 2016 to 2017F

$ 18

2016Intel SecurityCCG Reduction, Growth BusinessesMoore’s2017F

RestructuringLaw

Forecast

Restructuring in process…

while investing in growth segment and Moore’sLaw

2017 forecasts are Intel estimates, based upon current expectations and available information and is subject to change without notice.

Growth business spending is primarily driven by DCG, IOTG, and NSG.

8

|

|

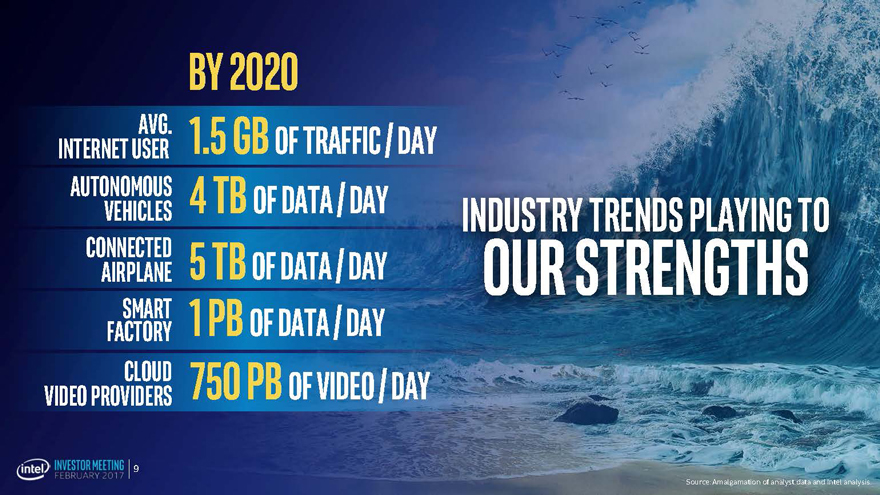

BY 2020

AVG. 1.5 GB OF TRAFFIC / DAY

INTERNET USER

AUTONOMOUS 4 TB OF DATA / DAY

VEHICLES INDUSTRY TRENDS PLAYING TO

CONNECTED 5 TB OF DATA / DAY

AIRPLANE OUR STRENGTHS

SMART 1 PB OF DATA / DAY

FACTORY

CLOUD 750 PB OF VIDEO / DA

VIDEO PROVIDERS

Source: Amalgamation of analyst data and Intel analysis.

9

|

|

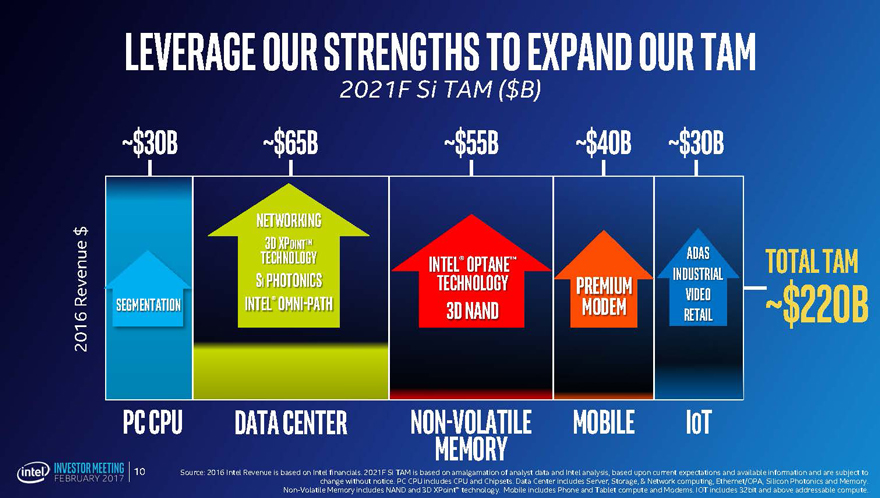

LEVERAGE OUR STRENGTHS TO EXPAND OUR TAM

2021F Si TAM ($B)

~$30B ~$65B~$55B~$40B~$30B

Networking

$

TechnologyADASTotal Tam

PhotonicstechnologyIndustrial

Video

2016 Revenue Segmentation Intel Ompath3D NANDmodemRetail~$220B

PC CPU Data centerNon-volatileMobileIoT

Memory

Source: 2016 Intel Revenue is based on Intel financials. 2021F Si TAM is based on amalgamation of analyst data and Intel analysis, based upon current expectations and available information and are subject to change without notice. PC CPU includes CPU and Chipsets. Data Center includes Server, Storage, & Network computing, Ethernet/OPA, Silicon Photonics and Memory.

Non-Volatile Memory includes NAND and 3D XPoint™ technology. Mobile includes Phone and Tablet compute and Modems. IOT includes 32bit and above addressable compute.

10

|

|

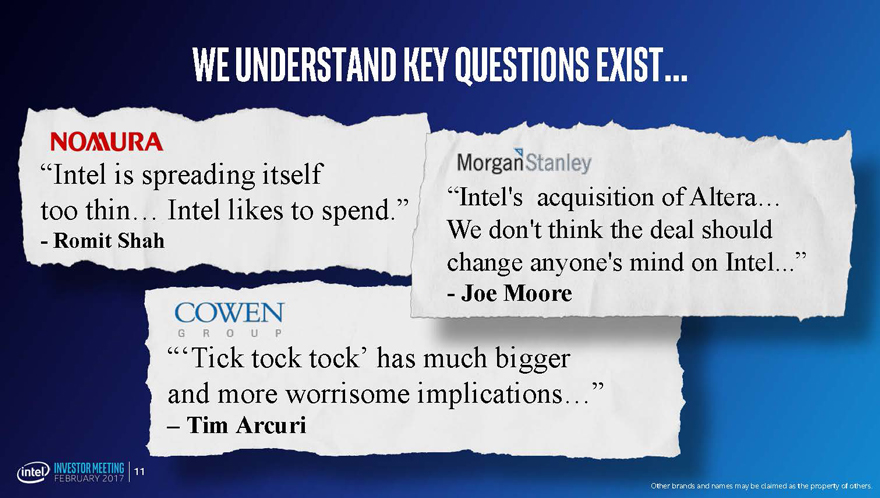

WE UNDERSTAND KEY QUESTIONS EXIST…

“Intel is spreading itself too thin… Intel likes to spend.” “Intel’s acquisition of Altera…

- Romit Shah We don’t think the deal should change anyone’s mind on Intel...”

- Joe Moore

“‘Tick tock tock’ has and more worrisome implications…”

– Tim Arcuri

Other brands and names may be claimed as the property of others.

11

|

|

DELIVER THE PRESENT…

CREATE THE FUTURE

|

|

DELIVER ON THE PRESENT… 2017 GUIDE (NON-GAAP)

REVENUE GROSS MARGIN EPS LOW SINGLE ~63% ~$2.80 DIGIT GROWTH

(excluding Security Business)

2017 forecasted figures are on a non-GAAP basis. Refer to the Appendix for a reconciliation of these non-GAAP measures. 2017 forecasts are Intel estimates, based upon current expectations and available information and are subject to change without notice. The full year revenue guidance excludes Intel Security from both 2016 and 2017. The full year 2017 Gross Margin and EPS forecasts include one quarter of our Intel Security business’ forecasted results.

13

|

|

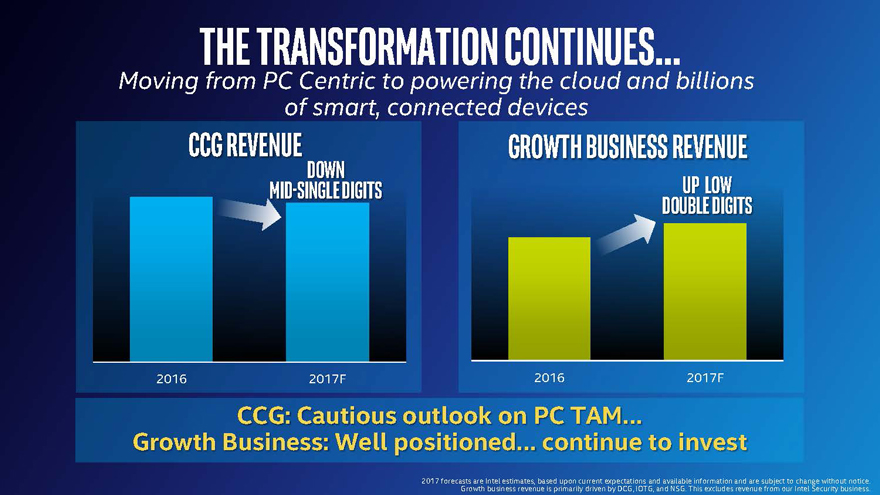

THE TRANSFORMATION CONTINUES…

Moving from PC Centric to powering the cloud and billions of smart, connected devices

CCG REVENUE GROWTH BUSINESS REVENUE

MI SINGLE DIGITS

DOUBLE DIGITS

2016 2017F 2016 2017F

CCG: Cautious outlook on PC TAM…

Growt Business Well positioned… continue to invest

2017 forecasts Growth are Intel business estimates, revenue based is primarily upon current driven expectations by DCG, IOTG, and and available NSG. This information excludes and revenue are subject from our to Intel change Security without business. notice.

|

|

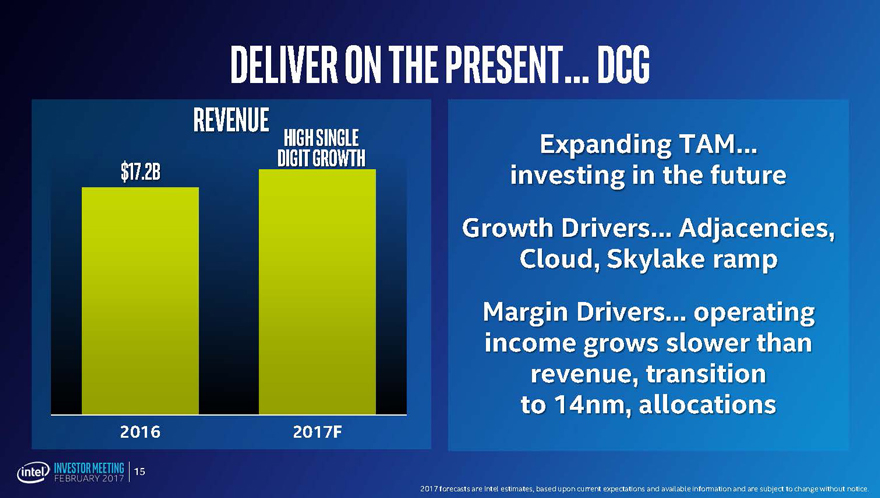

DELIVER ON THE PRESENT… DCG

Revenue

$17.2B git growth

2016 2017F

Expanding TAM… investing in the future Growth Drivers… Adjacencies, Cloud Skylak ramp Margin Drivers… operating income grows slower than revenue, transition to 14nm, allocations

2017 forecasts are Intel estimates, based upon current expectations and available information and are subject to change without notice.

15

|

|

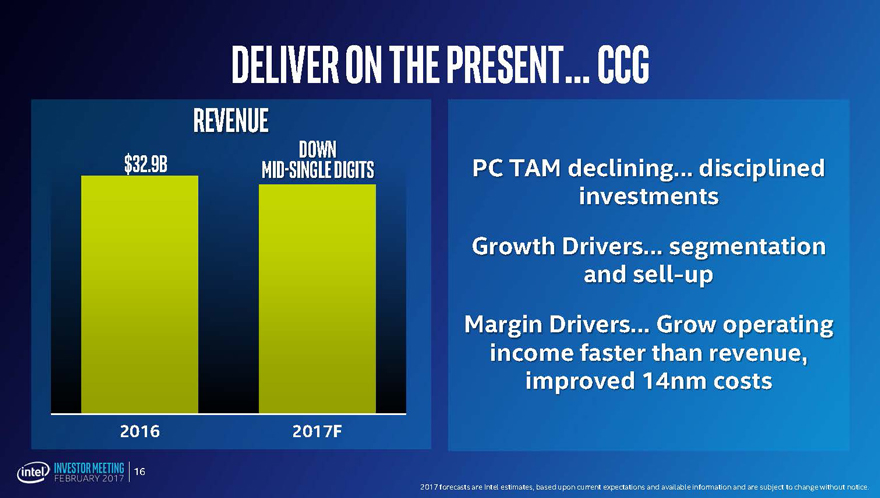

DELIVER ON THE PRESENT… CCG

Revenue

$32.9B Mi single digits

2016 2017F

PC TAM declining… disciplined investments Growth Drivers… segmentation and sel up Margin Drivers… Grow operating income faster than revenue, improved 14nm costs

2017 forecasts are Intel estimates, based upon current expectations and available information and are subject to change without notice.

16

|

|

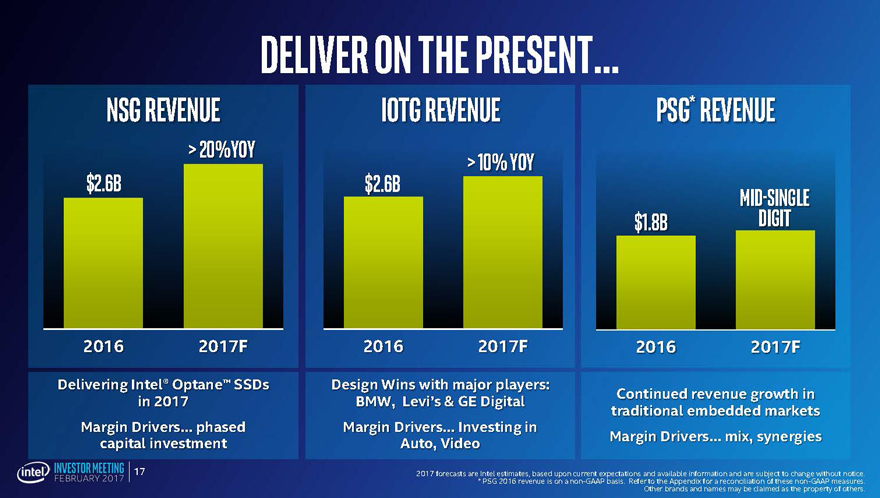

DELIVER ON THE PRESENT…

NSG Revenue IOTG Revenue PSGRevenue

oY > 1YoY

$2.6B $2.6BMi

$1.8Bdigit

2016 2017F 20162017F20162017F

Delivering Inte Optan ™ SSDs Design Wins with major players:

in 2017 BMW, Levi’s & GE Digital Continued revenue growth in

traditional embedded markets

Margin Drivers… phased Margin Drivers… Investing in

capital investment Auto, Video Margin Drivers… mix, synergies

2017 forecasts are* Intel PSG estimates, 2016 revenue based is on upon a non-GAAP current expectations basis. Refer and to the available Appendix information for a reconciliation and are subject of these to change non-GAAP without measures. notice.

Other brands and names may be claimed as the property of others.

17

|

|

CREATING THE FUTURE… BIG BETS

+ 00B TAM ~$10B TAM5+50Bs

(in 2021F) (2025F L3+ Automated Semi)(Connected Devices)

NVM

2021F

NVM fastest growing segment Semi content Per car Diversification of devices onto the

Positive Operating Margin late 2018 Today ~$100 to $200wireless network

Disciplined, staged capital investment New market opportunities

2025~10 to 15x

Source: Amalgamation of analyst data and Intel analysis, based upon current expectations and available information and are subject to change without notice. .

18

|

|

CAPITAL ALLOCATION

19

|

|

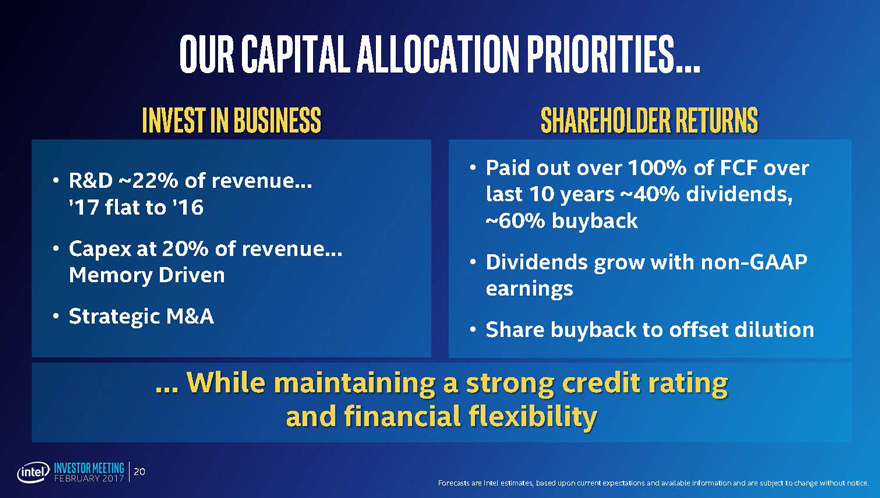

OUR CAPITAL ALLOCATION PRIORITIES…

INVEST IN BUSINESS

• R&D ~22% of revenue… ’17 flat to ’16

• Capex at 20% of revenue… Memory Driven

• Strategic M&A

Shareholder Returns

Paid ver last 10 years ~40% dividends, ~60% buyback

Dividends grow with non-GAAP earnings

Share buyback to offset dilution

… While maintaining a strong credit rating and financial flexibility

Forecasts are Intel estimates, based upon current expectations and available information and are subject to change without notice.

20

|

|

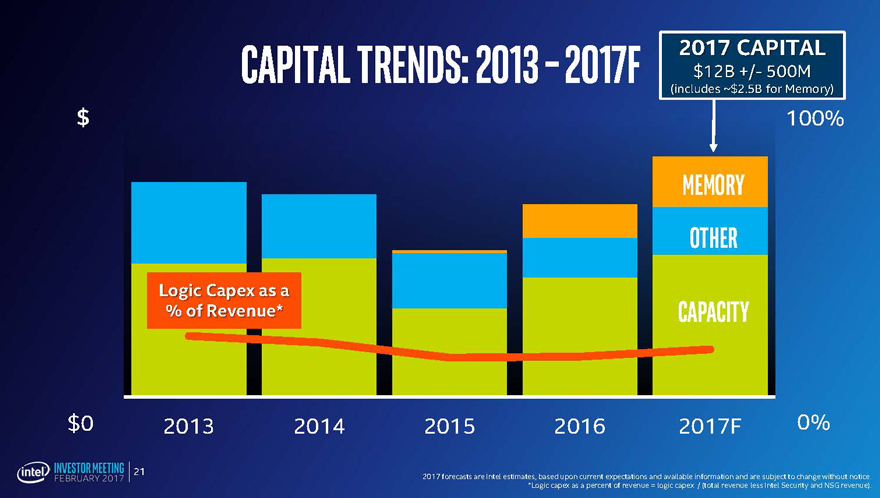

2017 CAPITAL

CAPITAL TRENDS: 2013 – 2017F $12B 500M

(includes ~$2.5B for Memory)

100%

$

Memory

Other

Logi Cape as a

% of Revenue* Capacity

$0 2013 2014201520162017F0%

2017 forecasts are Intel estimates, based upon current expectations and available information and are subject to change without notice.

*Logic capex as a percent of revenue = logic capex / (total revenue less Intel Security and NSG revenue).

21

|

|

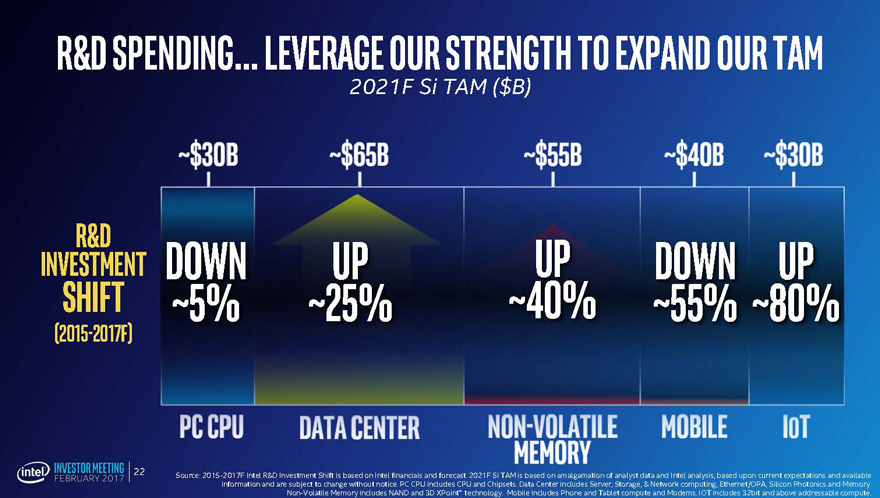

R&D SPENDING… LEVERAGE OUR STRENGTH TO EXPAND OUR TAM

2021F Si TAM ($B)

R&D

INVESTMENT

Shift ~5% ~25%~40%~55%~80%

(2015-2017F)

Source: 2015-2017F Intel R&D Investment Shift is based on Intel financials and forecast. 2021F Si TAM is based on amalgamation of analyst data and Intel analysis, based upon current expectations and available information and are subject to change without notice. PC CPU includes CPU and Chipsets. Data Center includes Server, Storage, & Network computing, Ethernet/OPA, Silicon Photonics and Memory.

Non-Volatile Memory includes NAND and 3D XPoint™ technology. Mobile includes Phone and Tablet compute and Modems. IOT includes 32bit and above addressable compute.

22

|

|

STRATEGIC M&A… STRENGTHENING OUR INTEGRATION

Forecasts are Intel estimates, based upon current expectations and available information and are subject to change without notice.

|

|

ACCELERATE

OUR CAPABILITIES

STRATEGIC M&A

24

|

|

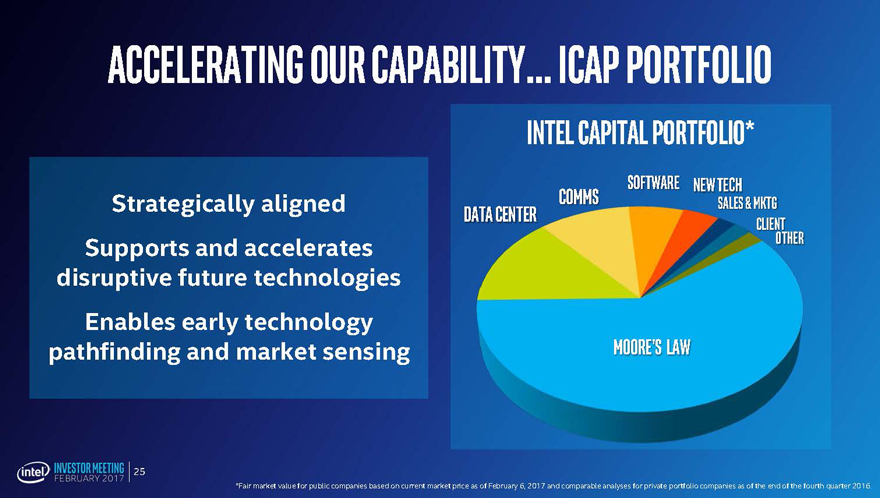

ACCELERATING OUR CAPABILITY… ICAP PORTFOLIO

Strategically aligned Supports and accelerates disruptive future technologies Enables early technology pathfinding and market sensing

Intel Capital Portfolio*

Software New Tech

Comms Sales & Mktg

Data Center Client

Other

MoorE’ LAW

*Fair market value for public companies based on current market price as of February 6, 2017 and comparable analyses for private portfolio companies as of the end of the fourth quarter 2016.

25

|

|

SHAREHOLDER RETURNS… DIVIDEND INCREASE PLANNED STARTING IN Q2 ‘17

Dividend/Share

2017 $1.04

$0.05*

2005 2006 2007200820092010201120122013201420152016

*Pending final approval by Intel’s Board of Directors.

26

|

|

OVER THE NEXT 3 YEARS…

Revenue Growth Operating efficiency earnings

CCG declines Gross Margins decline Net cash

low single digits modestly… remain in top growt and/or

half of historical range opportunistic buybacks

Growth’ businesses

doubl digit growth Direct spending as % ICAP portfolio returns

o revenue declines

Effective tax rate

R&D Efficienc & flat or down

SG& Leverage

Lo single dig growth Operating income growth > Revenue EPS growtOperating income

Forecasts are Intel estimates, based upon current expectations and available information and are subject to change without notice.

27

|

|

IN CLOSING

Transformation continues… from PC centric to powering the cloud and billions of smart, connected devices A data oriented company… expanding our TAM

We are making big bets… but will improve our efficiency

Capital returns remain a high priority

28

|

|

Q&A

|

|

Investor MeetingFEBRUARY 2017

|

|

APPENDIX

|

|

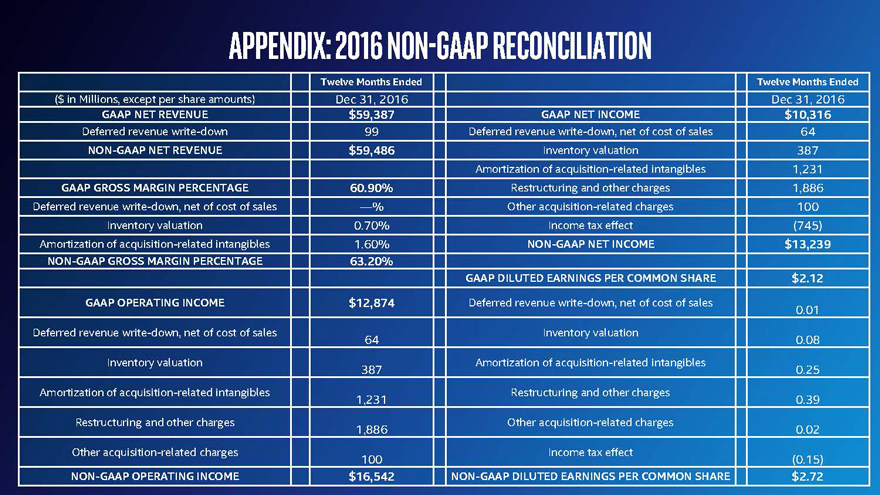

APPENDIX: 2016 NON-GAAP RECONCILIATION

Twelve Months Ended Twelve Months Ended

($ in Millions, except per share amounts) Dec 31, 2016 Dec 31, 2016

GAAP NET REVENUE $59,387 GAAP NET INCOME$10,316

Deferred revenue write-down 99 Deferred revenue write-down, net of cost of sales64

NON-GAAP NET REVENUE $59,486 Inventory valuation387

Amortization of acquisition-related intangibles1,231

GAAP GROSS MARGIN PERCENTAGE 60.90% Restructuring and other charges1,886

Deferred revenue write-down, net of cost of sales —% Other acquisition-related charges100

Inventory valuation 0.70% Income tax effect(745)

Amortization of acquisition-related intangibles 1.60% NON-GAAP NET INCOME$13,239

NON-GAAP GROSS MARGIN PERCENTAGE 63.20%

GAAP DILUTED EARNINGS PER COMMON SHARE$2.12

GAAP OPERATING INCOME $12,874 Deferred revenue write-down, net of cost of sales0.01

Deferred revenue write-down, net of cost of sales Inventory valuation

64 0.08

Inventory valuation Amortization of acquisition-related intangibles

387 0.25

Amortization of acquisition-related intangibles Restructuring and other charges

1,231 0.39

Restructuring and other charges Other acquisition-related charges

1,886 0.02

Other acquisition-related charges Income tax effect

100 (0.15)

NON-GAAP OPERATING INCOME $16,542 NON-GAAP DILUTED EARNINGS PER COMMON SHARE$2.72

|

|

APPENDIX: 2017 NON-GAAP RECONCILIATION

2017 Outlook

GAAP GROSS MARGIN PERCENTAGE 62%

Adjustment for amortization of acquisition-related intangibles 1%

NON-GAAP GROSS MARGIN PERCENTAGE 63%

GAAP EARNINGS PER SHARE $2.53

Adjustment for restructuring and other charges $0.08

Adjustment for amortization of acquisition-related intangibles $0.19

(Gains) losses from divestiture ($0.08)

Income tax effect $0.08

NON-GAAP EARNINGS PER SHARE $2.80

Twelve Months Ended

($ in Billions) Dec 31, 2016

GAAP PSG NET REVENUE $1.7

Deferred revenue write-down $0.1

NON-GAAP PSG NET REVENUE $1.8

33