Exhibit 99.2 Future node performance and other metrics, including power and density, are projections and are inherently uncertain and, in the case of other industry nodes, are derived from or estimated based on publicly available information. Intel’s node numbers do not represent the actual dimension of any physical feature on a transistor or structure. They also do not pinpoint a specific level of improvement in performance, power or area, and the magnitude of a decrease from one node number to the next is not necessarily proportionate to the level of improvement in one or more metrics. Historically, new Intel node numbers were based solely on improvements in area/density; now, node numbers generally reflect a holistic assessment of improvement across metrics and can be based on improvement in one or more of performance, power, area, or other important factors, or a combination, and will not necessarily be based on area/density improvement alone. Non-GAAP Financial Measures. This presentation contains non-GAAP financial measures. Intel gross margin and earnings per share, as well as Intel revenue for fiscal years 2021 and earlier, are presented on a non-GAAP basis unless otherwise indicated. This presentation also includes a non-GAAP free cash flow (FCF) measure. The appendix to these materials available at www.intc.com provides a reconciliation of these measures to the most directly comparable GAAP financial measure. The non-GAAP financial measures disclosed by Intel should not be considered a substitute for, or superior to, the financial measures prepared in accordance with GAAP. Forward-Looking Statements. Statements in this presentation that refer to business outlook, plans, and expectations are forward-looking statements that involve risks and uncertainties. Words such as anticipate, expect, intend, goal, plans, believe, seek, estimate, continue,“ “committed,” “on-track,” ”positioned,” “ramp,” “momentum,” “roadmap,” “path,” “pipeline,” “progress,” “schedule,” “forecast,” “likely,” “guide,” “potential,” “next gen,” “future,” may, will, “would,” should, “could,” strategy, accelerate, cadence, deliver, and variations of such words and similar expressions are intended to identify such forward-looking statements. Statements that refer to or are based on estimates, forecasts, projections, uncertain events, or assumptions also identify forward-looking statements. Forward-looking statements in this presentation include: statements relating to Intel’s strategy and its anticipated benefits; Intel's process and packaging technology roadmap and schedules; innovation cadence; business plans; financial projections and expectations; total addressable market (TAM) and market opportunity; manufacturing expansion, financing, and investment plans; future manufacturing capacity; future technology, services, and products and the expected benefits and availability of such technologies, services, and products, including PowerVia and RibbonFET technologies, future process nodes, and other technologies and products; product and manufacturing plans, goals, timelines, ramps, progress, and future product and process leadership and performance; future economic conditions; future impacts of the COVID-19 pandemic; plans and goals related to Intel’s foundry business; future legislation; future capital offsets; pending or future transactions; the proposed Mobileye IPO; the memorandum of understanding with Brookfield; supply expectations including regarding industry shortages; future external foundry usage; future use of EUV and other manufacturing tools and technologies; expectations regarding customers, including designs, wins, orders, and partnerships; projections regarding competitors; ESG goals; and anticipated trends in our businesses or the markets relevant to them, including future demand, market share, industry growth, and technology trends, also identify forward-looking statements. Such statements involve many risks and uncertainties that could cause actual results to differ materially from those expressed or implied in these forward-looking statements. Important factors that could cause actual results to differ materially are set forth in Intel's earnings release dated January 26, 2022, which is included as an exhibit to Intel’s Form 8-K furnished to the SEC on such date, and in Intel's SEC filings, including the company's most recent reports on Forms 10-K and 10-Q. Copies of Intel’s SEC filings may be obtained by visiting our Investor Relations website at www.intc.com or the SEC's website at www.sec.gov. All information in this presentation reflects management’s views as of February 17, 2022, unless an earlier date is indicated. Intel does not undertake, and expressly disclaims any duty, to update any statement made in this presentation, whether as a result of new information, new developments or otherwise, except to the extent that disclosure may be required by law. Intel technologies may require enabled hardware, software or service activation. No product or component can be absolutely secure. Your costs and results may vary. Product and process performance varies by use, configuration and other factors. Learn more at www.Intel.com/PerformanceIndex and www.Intel.com/ProcessInnovation. Future product and process performance and other metrics are projections and are inherently uncertain. © Intel Corporation. Intel, the Intel logo, and other Intel marks are trademarks of Intel Corporation or its subsidiaries. Other names and brands may be claimed as the property of others.

Investor Meeting 2022

Investor Meeting 2022 CEO, Intel

We’re setting a … with much left to do, but… Unleashed Accelerated Architecture Innovation IEDM Today Day Our Commitment to: IDM & Process Product Open Moore’s Growth & Foundry Leadership Leadership Ecosystems Law Shareholders ….we are

We’re rebuilding our “Groveian” execution engine We have the right strategy We are leveraging our core strengths to grow traditional markets and disrupt new ones Intel is the next great growth story

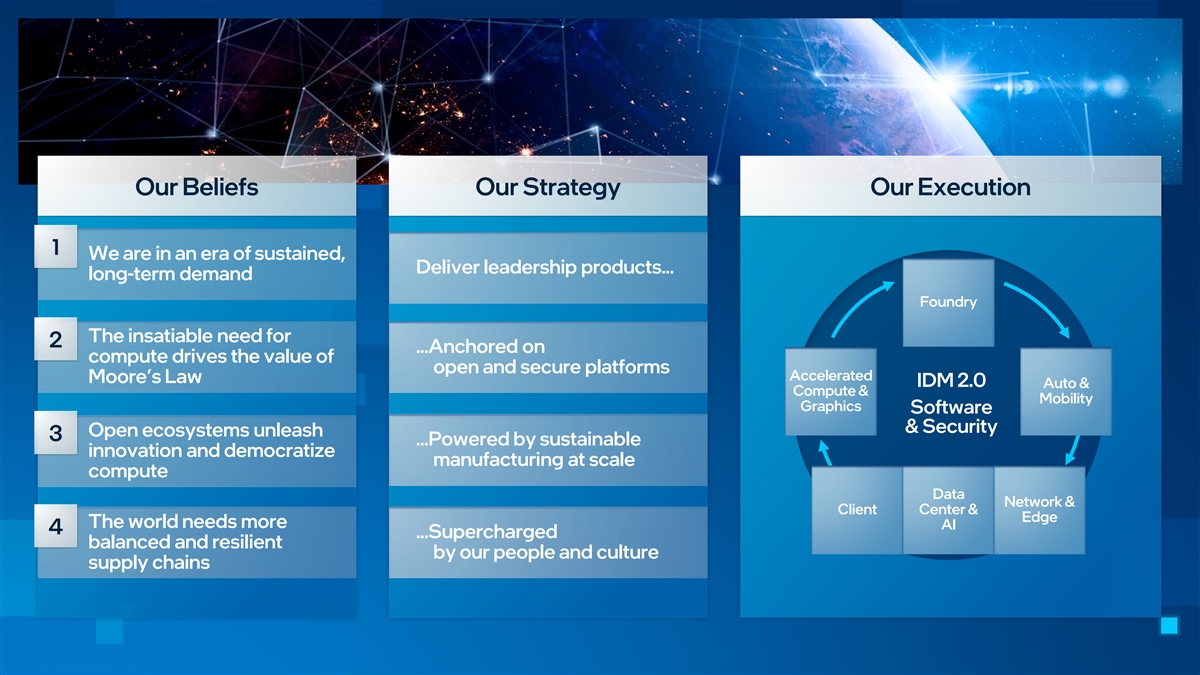

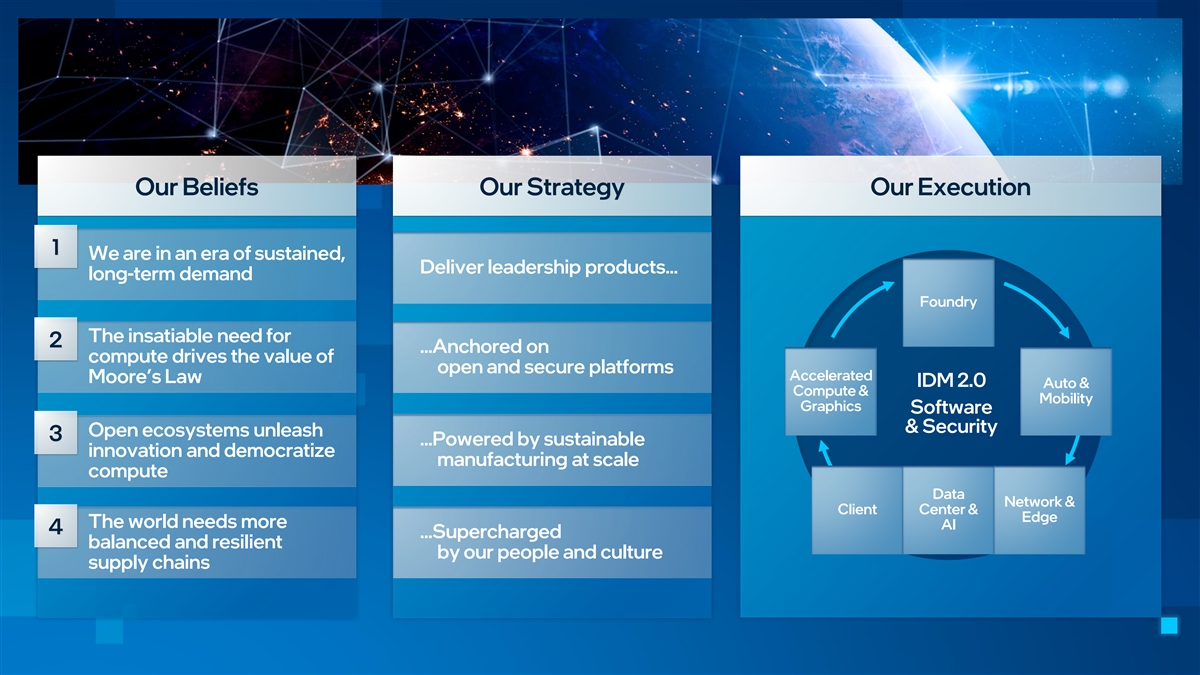

Our Beliefs Our Strategy Our Execution 1 We are in an era of sustained, Deliver leadership products… long-term demand Foundry The insatiable need for 2 …Anchored on compute drives the value of open and secure platforms Accelerated Moore’s Law IDM 2.0 Auto & Compute & Mobility Graphics Software & Security Open ecosystems unleash 3 …Powered by sustainable innovation and democratize manufacturing at scale compute Data Network & Client Center & Edge The world needs more AI 4 …Supercharged balanced and resilient by our people and culture supply chains

Our Beliefs Our Strategy Our Execution 1 We are in an era of sustained, Deliver leadership products… long-term demand Foundry The insatiable need for 2 …Anchored on compute drives the value of open and secure platforms Accelerated Moore’s Law IDM 2.0 Auto & Compute & Mobility Graphics Software & Security Open ecosystems unleash 3 …Powered by sustainable innovation and democratize manufacturing at scale compute Data Network & Client Center & Edge The world needs more AI 4 …Supercharged balanced and resilient by our people and culture supply chains

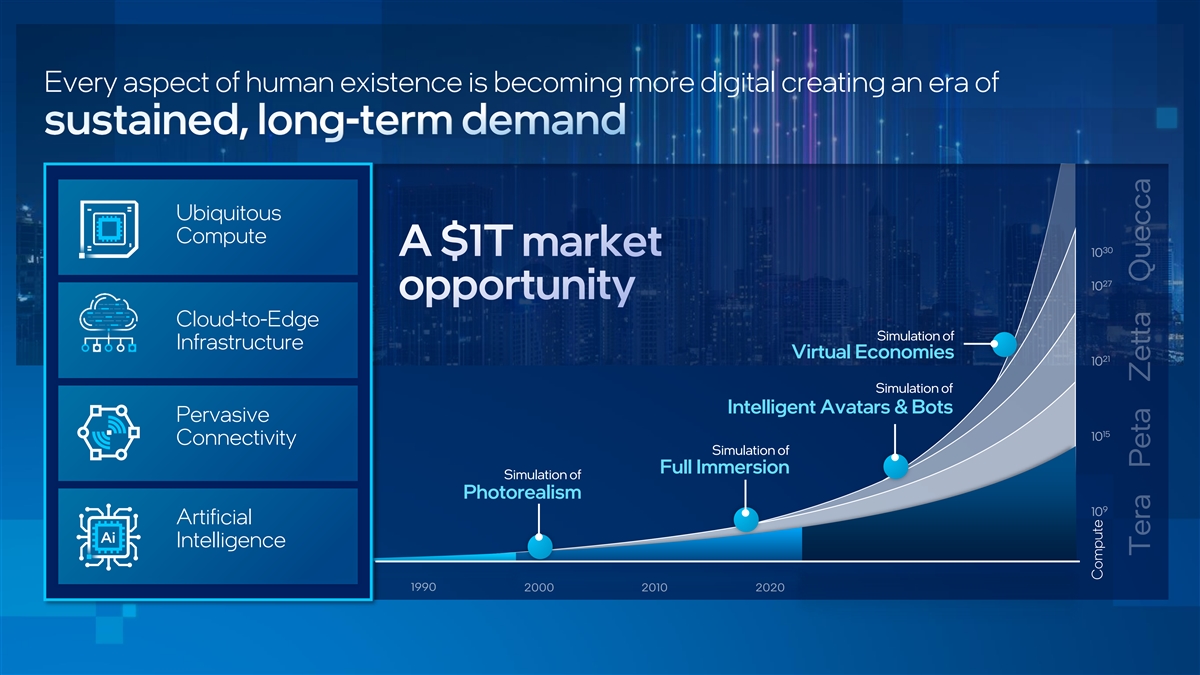

Every aspect of human existence is becoming more digital creating an era of Ubiquitous Compute Cloud-to-Edge Simulation of Infrastructure Virtual Economies Simulation of Intelligent Avatars & Bots Pervasive Connectivity Simulation of Full Immersion Simulation of Photorealism Artificial Intelligence Compute

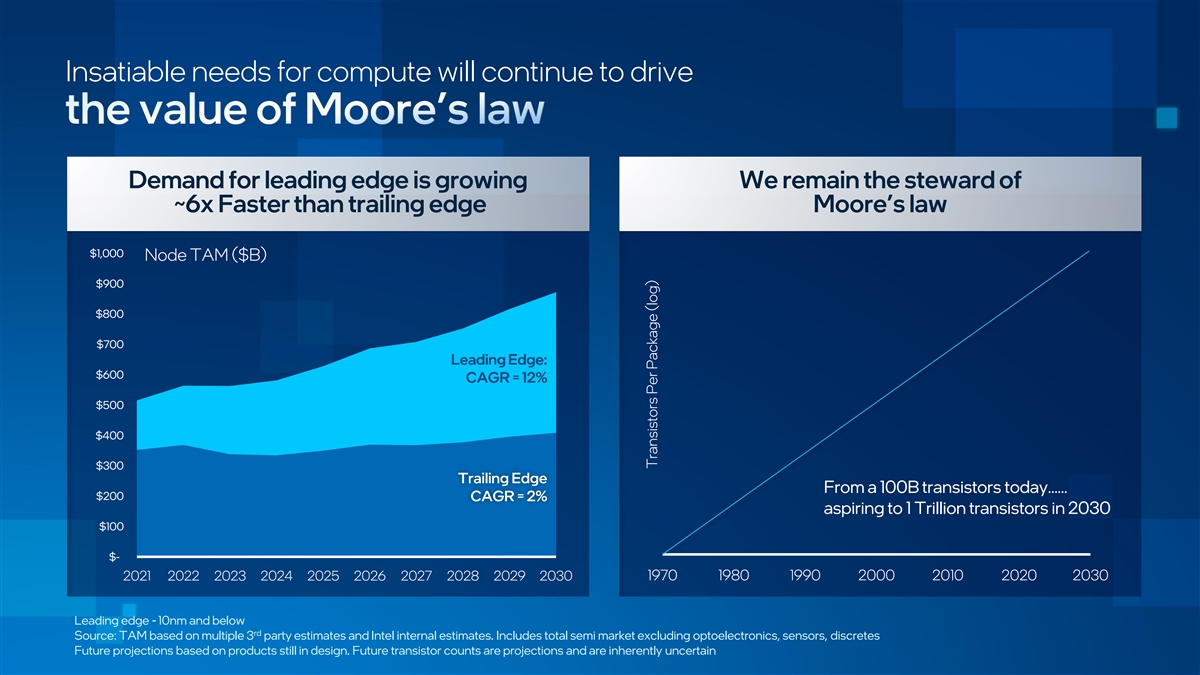

Insatiable needs for compute will continue to drive Demand for leading edge is growing We remain the steward of ~6x Faster than trailing edge Moore’s law $1,000 Node TAM ($B) $900 $800 $700 Leading Edge: $600 CAGR = 12% $500 $400 $300 Trailing Edge From a 100B transistors today…… $200 CAGR = 2% aspiring to 1 Trillion transistors in 2030 $100 $- 1970 1980 1990 2000 2010 2020 2030 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 Leading edge - 10nm and below rd Source: TAM based on multiple 3 party estimates and Intel internal estimates. Includes total semi market excluding optoelectronics, sensors, discretes Future projections based on products still in design. Future transistor counts are projections and are inherently uncertain Transistors Per Package (log)

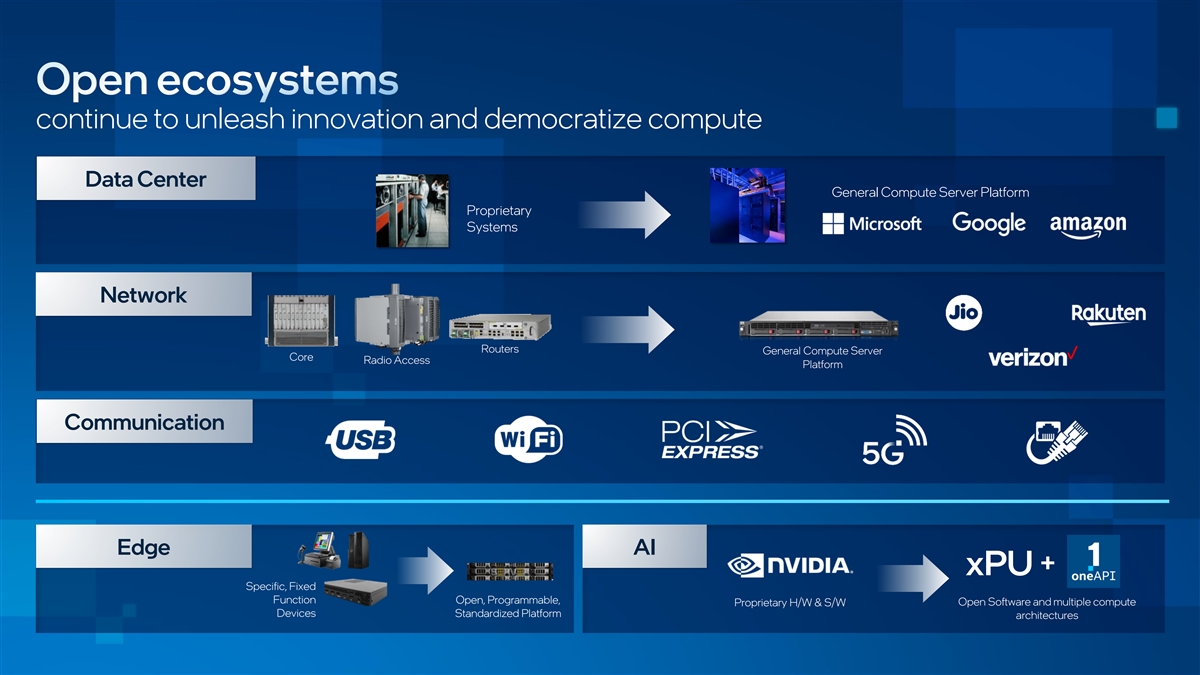

continue to unleash innovation and democratize compute Data Center General Compute Server Platform Proprietary Systems Network Routers General Compute Server Core Radio Access Platform Communication Edge AI xPU + Specific, Fixed Function Open, Programmable, Proprietary H/W & S/W Open Software and multiple compute Devices Standardized Platform architectures

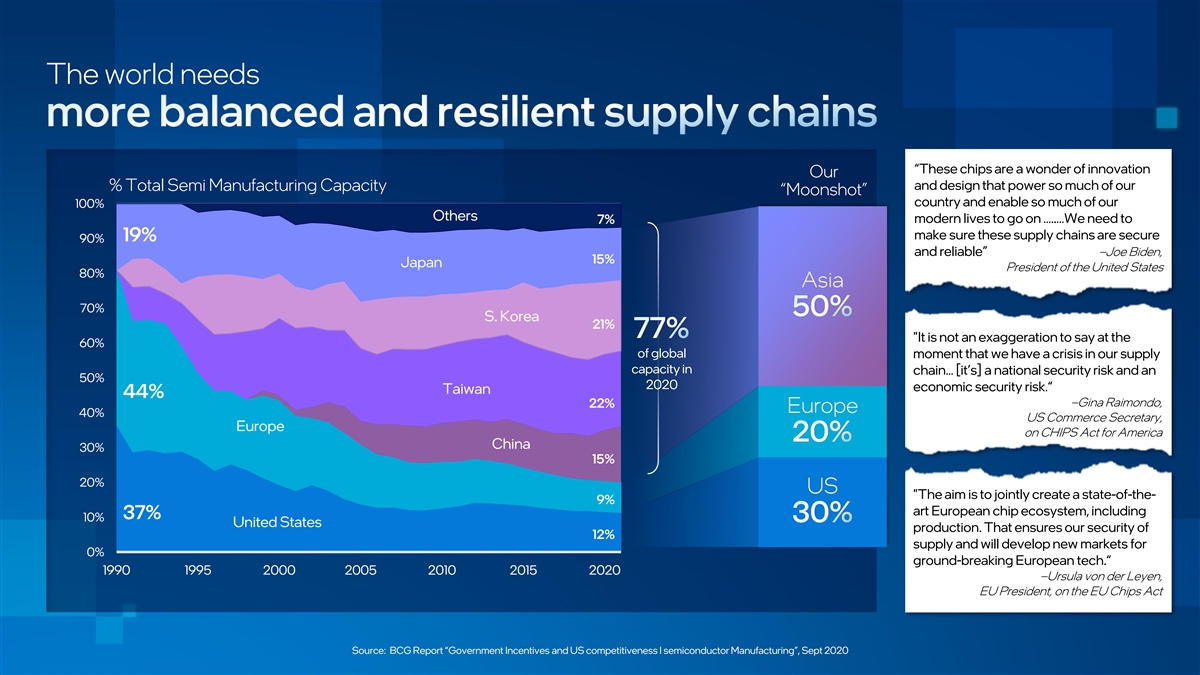

The world needs “These chips are a wonder of innovation Our and design that power so much of our % Total Semi Manufacturing Capacity “Moonshot” country and enable so much of our 100% 3% Others 7% modern lives to go on …..…We need to make sure these supply chains are secure 19% 90% and reliable” –Joe Biden, 17% 15% Japan President of the United States 80% Asia 70% 13% S. Korea 21% It is not an exaggeration to say at the 60% of global moment that we have a crisis in our supply 22% capacity in chain… [it’s] a national security risk and an 50% 2020 economic security risk.“ Taiwan 44% –Gina Raimondo, 22% Europe 40% US Commerce Secretary, Europe on CHIPS Act for America China 30% 24% 15% 20% US The aim is to jointly create a state-of-the- 9% art European chip ecosystem, including 37% 10% 19% United States production. That ensures our security of 12% supply and will develop new markets for 0% ground-breaking European tech.“ 1990 1995 2000 2005 2010 2015 2020 –Ursula von der Leyen, EU President, on the EU Chips Act Source: BCG Report “Government Incentives and US competitiveness I semiconductor Manufacturing”, Sept 2020

Our Strategy Deliver leadership products… …Anchored on open and secure platforms We have …Powered by sustained manufacturing at scale …Supercharged by our people and culture

Delivering across all of our businesses o Fastest Up to a 30x Hyperscale-ready, best- Industry-leading FLOPs 11 camera 360 coverage, Client Processor gen-on-gen AI performance in-class programmable and compute density to RSS, 2x EyeQ5 SoCs, …Ever gain for Xeon packet processing accelerate AI and HPC over-the-air updates Learn more at www.intel.com/PerformanceIndex. Results may vary.

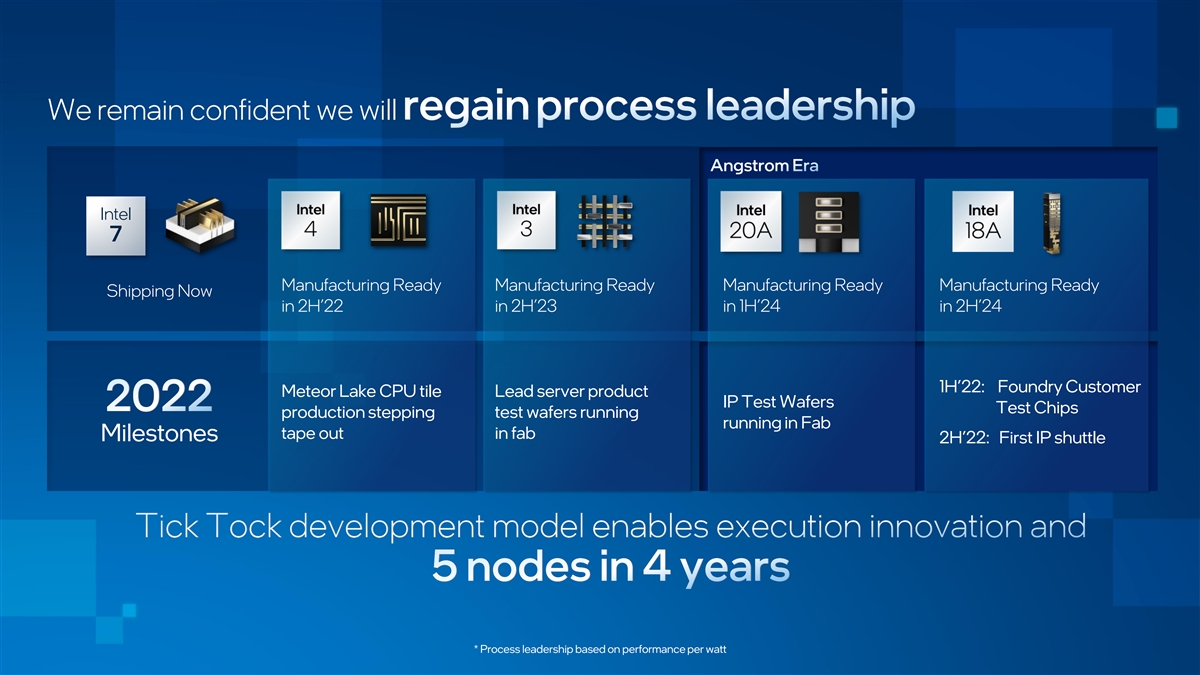

We remain confident we will Intel 7 Manufacturing Ready Manufacturing Ready Manufacturing Ready Manufacturing Ready Shipping Now in 2H’22 in 2H’23 in 1H’24 in 2H’24 1H’22: Foundry Customer Meteor Lake CPU tile Lead server product IP Test Wafers Test Chips production stepping test wafers running running in Fab tape out in fab Milestones 2H’22: First IP shuttle * Process leadership based on performance per watt

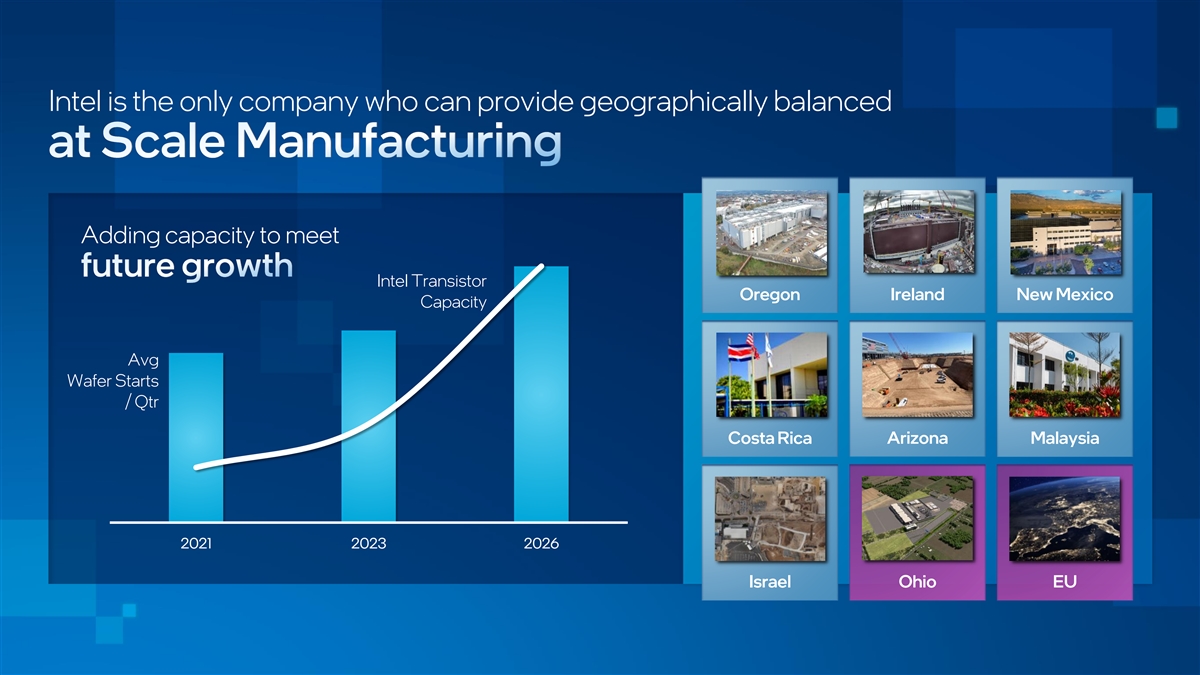

Intel is the only company who can provide geographically balanced Adding capacity to meet Intel Transistor Oregon Ireland New Mexico Capacity Avg Wafer Starts / Qtr Costa Rica Arizona Malaysia 2021 2023 2026 Israel Ohio EU

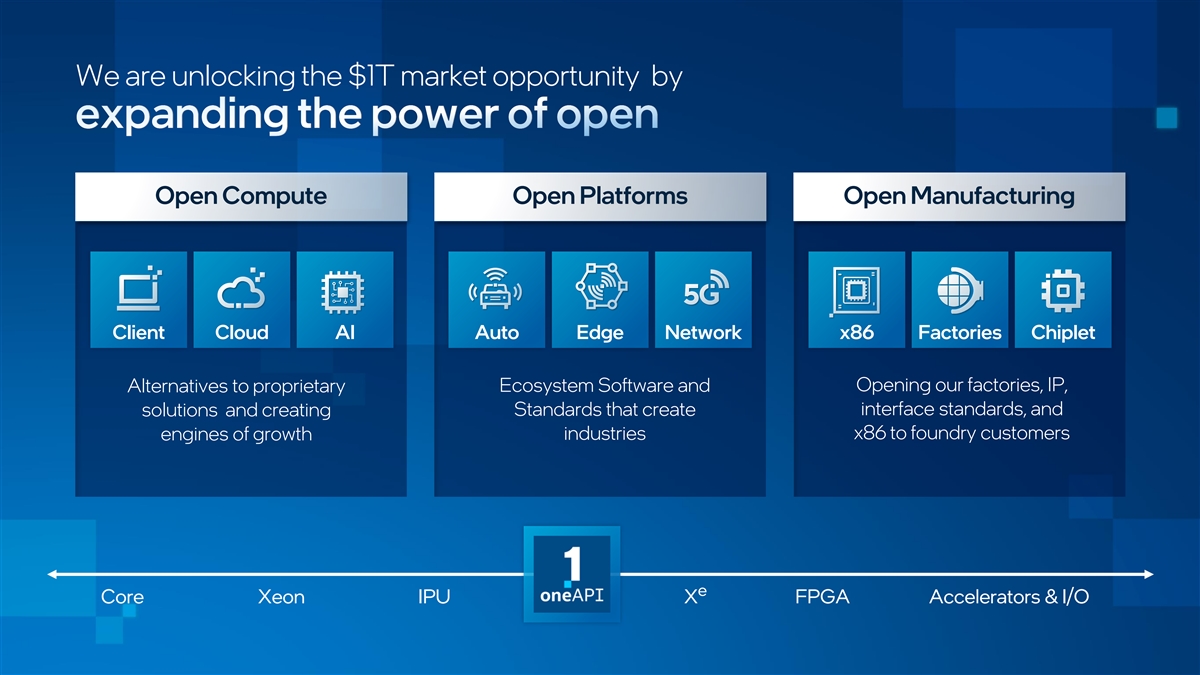

We are unlocking the $1T market opportunity by Open Compute Open Platforms Open Manufacturing Client Cloud AI Auto Edge Network x86 Factories Chiplet Opening our factories, IP, Alternatives to proprietary Ecosystem Software and interface standards, and solutions and creating Standards that create engines of growth industries x86 to foundry customers e Core Xeon IPU X FPGA Accelerators & I/O

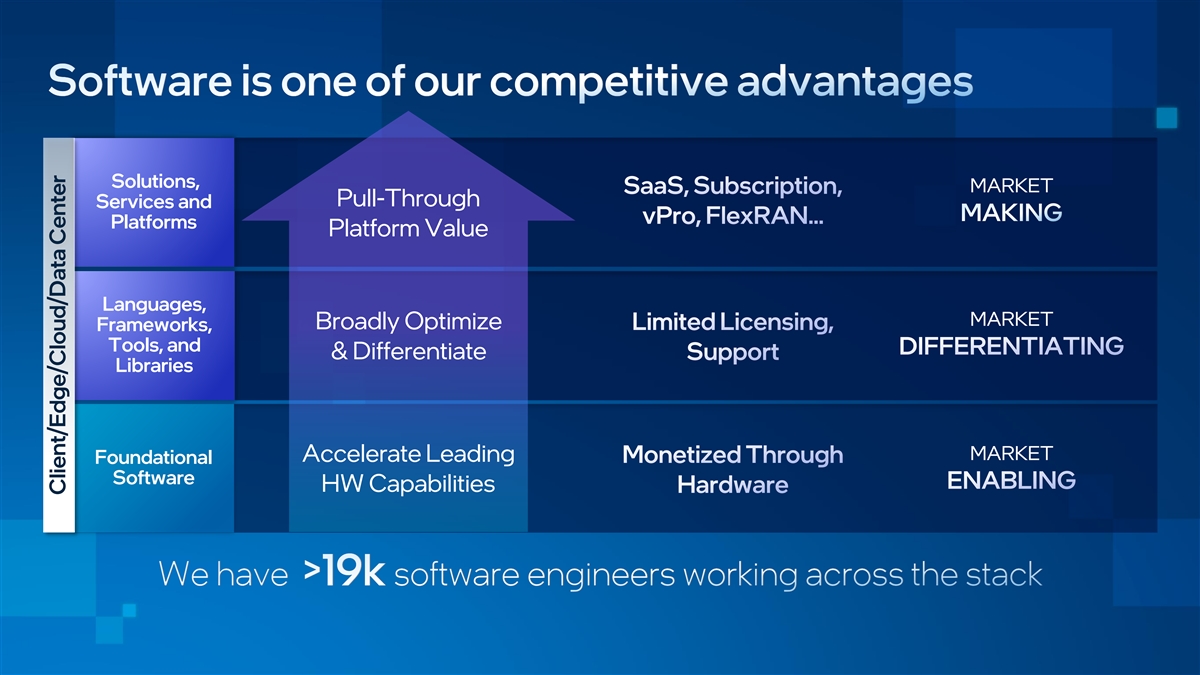

Solutions, MARKET Pull-Through Services and Platforms Platform Value Languages, MARKET Broadly Optimize Frameworks, Tools, and & Differentiate Libraries MARKET Accelerate Leading Foundational Software HW Capabilities Client/Edge/Cloud/Data Center

Winning developers and delivering better products with our 1 Enable Developers 2 Foster Choice Open. Choice. Trust. 3 Build Confidential Compute Visit: Open.Intel 20 #1 120+ 700+ 6 CHROME OS Years of Investment Linux Kernel Intel Employed GitHub Architectures Leading Contributor Across hundreds Corporate Contributor Maintainers Projects Supported in oneAPI of independent projects since 2007¹ ¹SOURCE: https://www.linuxfoundation.org/wp-content/uploads/2020_kernel_history_report_082720.pdf

We are reigniting our innovation and execution through One Voice Sales, Marketing & Communications to Market Michelle Johnston Holthaus & Customer Client Computing Accelerated Computing Network & Edge Michelle Johnston Holthaus Systems & Graphics Nick McKeown Jim Johnson - interim Raja Koduri Distinct Business Units Datacenter & AI Mobileye Foundry Services Sandra Rivera Amnon Shashua Randhir Thakur Manufacturing, Software & Technology Design Functional Supply Chain & Advanced Development Engineering Groups Operations Technology Ann Kelleher Sunil Shenoy Keyvan Esfarjani Greg Lavender Human Growth Corporate General & Finance Resources Acceleration Strategy Administrative David Zinsner Christy Susie Giordano Saf Yeboah Pambianchi (acting)

We are reigniting our innovation and execution through employees with 89% technical expertise 121,000+ patent assets worldwide ~70,000 countries with Intel employees 53 Andy Bryant - Former Intel Chairman Andy Grove - Former Intel CEO & Chairman

Our Execution Foundry Accelerated Auto & Compute & Intel is the next Mobility Graphics Data Network & Client Center & Edge AI

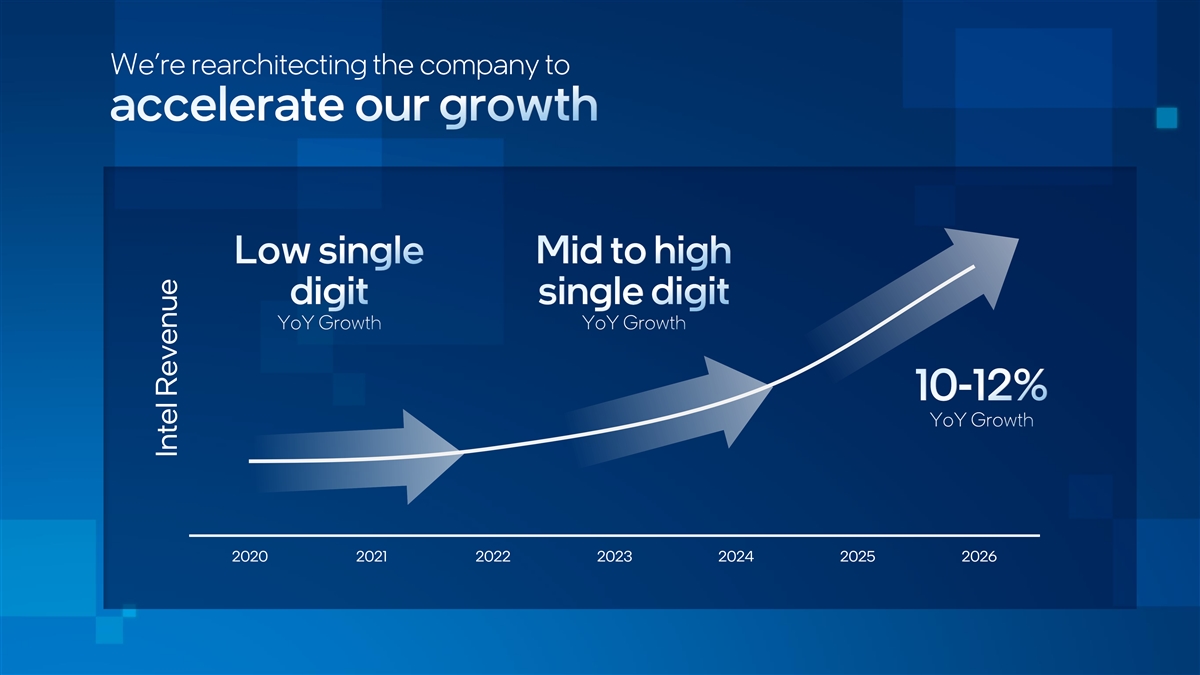

We’re rearchitecting the company to 2020 2021 2022 2023 2024 2025 2026 Intel Revenue

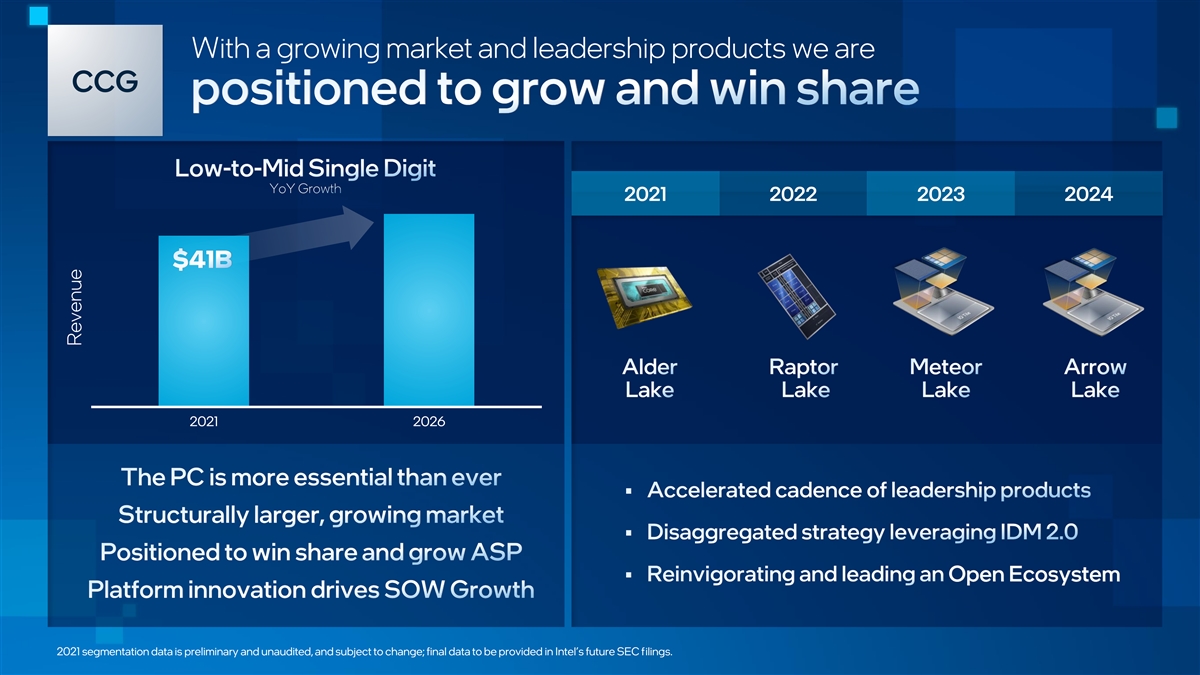

With a growing market and leadership products we are CCG 2021 2022 2023 2024 2021 2026 Open Ecosystem 2021 segmentation data is preliminary and unaudited, and subject to change; final data to be provided in Intel’s future SEC filings. Revenue

P-Core E-Core New dual track roadmap with differentiated features DCAI 2021 2022 2023 2024 Ice Lake Sapphire Emerald Granite Rapids Rapids Rapids Sierra 2021 2023 2026 Forest 2021 segmentation data is preliminary and unaudited, and subject to change; final data to be provided in Intel’s future SEC filings. Revenue

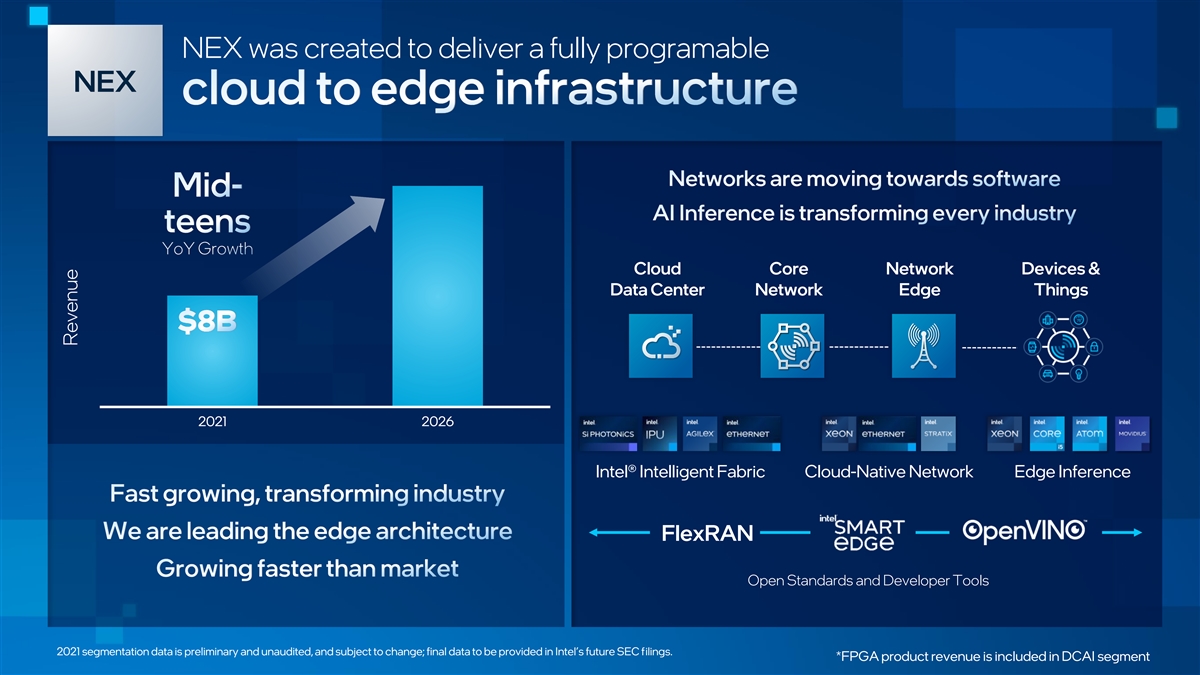

NEX was created to deliver a fully programable NEX Cloud Core Network Devices & Data Center Network Edge Things 2021 2026 Intel® Intelligent Fabric Cloud-Native Network Edge Inference FlexRAN Open Standards and Developer Tools 2021 segmentation data is preliminary and unaudited, and subject to change; final data to be provided in Intel’s future SEC filings. *FPGA product revenue is included in DCAI segment Revenue

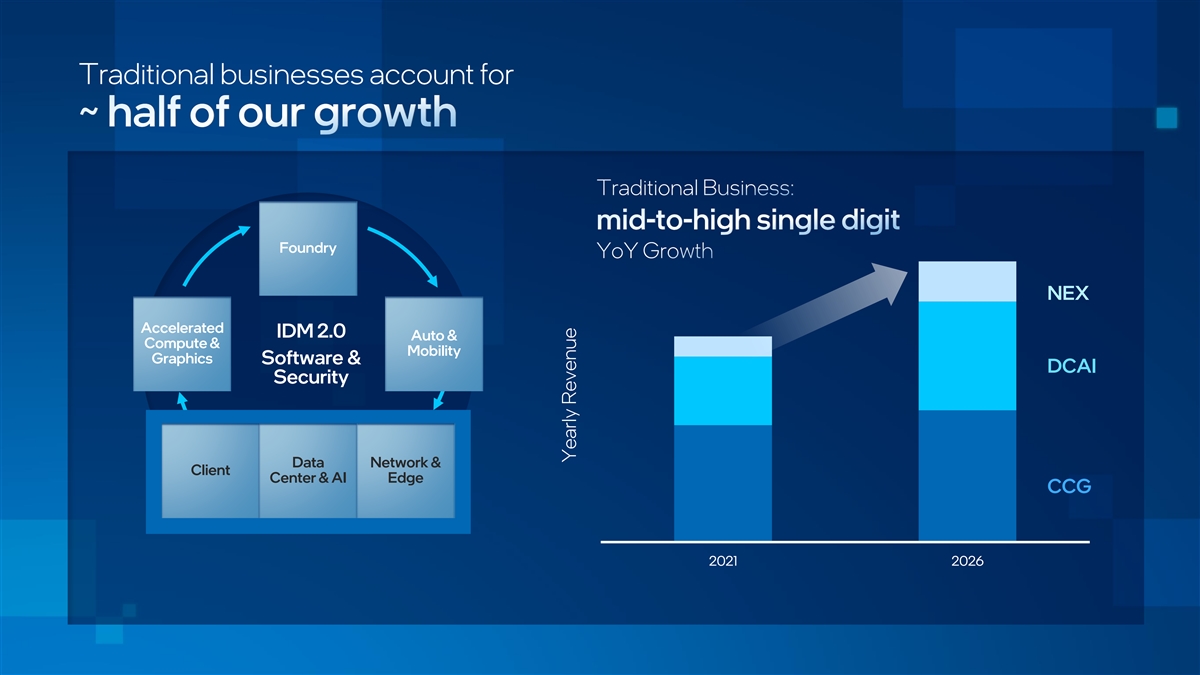

Traditional businesses account for Foundry NEX Accelerated IDM 2.0 Auto & Compute & Mobility Graphics Software & DCAI Security Data Network & Client Center & AI Edge CCG 2021 2026 Yearly Revenue

Building on our installed base and a thriving open ecosystem we expect AXG 2021 2022 2023 2024 Sapphire Xeon next Super Rapids HBM HBM Falcon Compute Shores HPC- AI Ponte Vecchio Ponte Vecchio next Arctic Sound Media & Analytics Arctic Sound next Visual Alchemist Battlemage Compute (Client GPU) 2021 2022 2026 *Revenue Outlook includes intersegment graphics royalty that is eliminated in Intel consolidated results 2021 segmentation data is preliminary and unaudited, and subject to change; final data to be provided in Intel’s future SEC filings. Learn more at www.intel.com/PerformanceIndex. Results may vary. Revenue

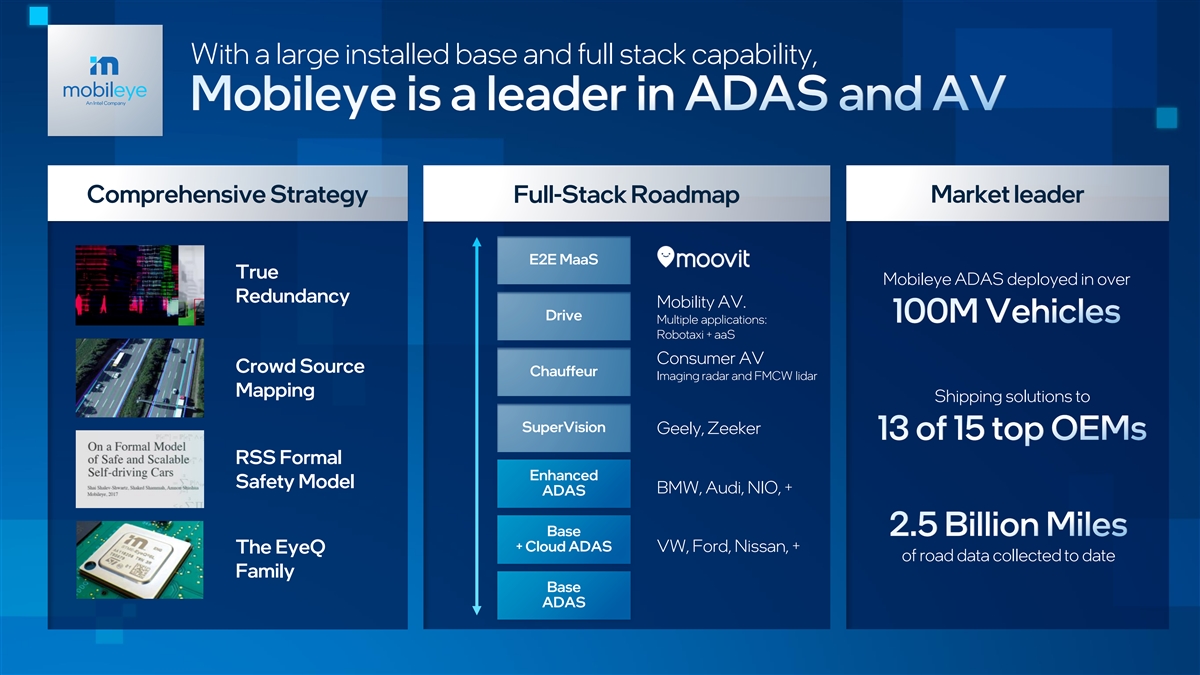

With a large installed base and full stack capability, Comprehensive Strategy Full-Stack Roadmap Market leader E2E MaaS True Mobileye ADAS deployed in over Redundancy Mobility AV. Drive Multiple applications: Robotaxi + aaS Consumer AV Crowd Source Chauffeur Imaging radar and FMCW lidar Mapping Shipping solutions to SuperVision Geely, Zeeker RSS Formal Enhanced Safety Model BMW, Audi, NIO, + ADAS Base + Cloud ADAS VW, Ford, Nissan, + The EyeQ of road data collected to date Family Base ADAS

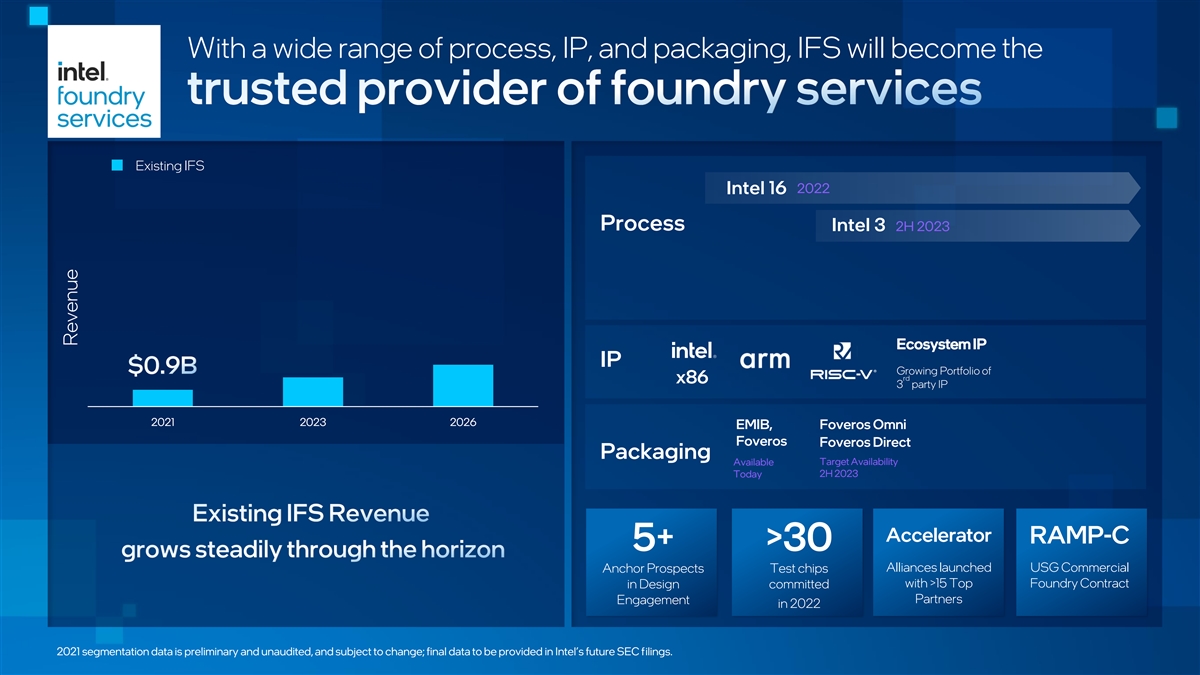

With a wide range of process, IP, and packaging, IFS will become the Existing IFS 2022 Intel 16 Process Intel 3 2H 2023 Ecosystem IP IP Growing Portfolio of rd x86 3 party IP 2021 2023 2026 EMIB, Foveros Omni Foveros Foveros Direct Packaging Available Target Availability Today 2H 2023 Accelerator RAMP-C 5+ >30 Anchor Prospects Test chips Alliances launched USG Commercial with >15 Top Foundry Contract in Design committed Engagement Partners in 2022 2021 segmentation data is preliminary and unaudited, and subject to change; final data to be provided in Intel’s future SEC filings. Revenue

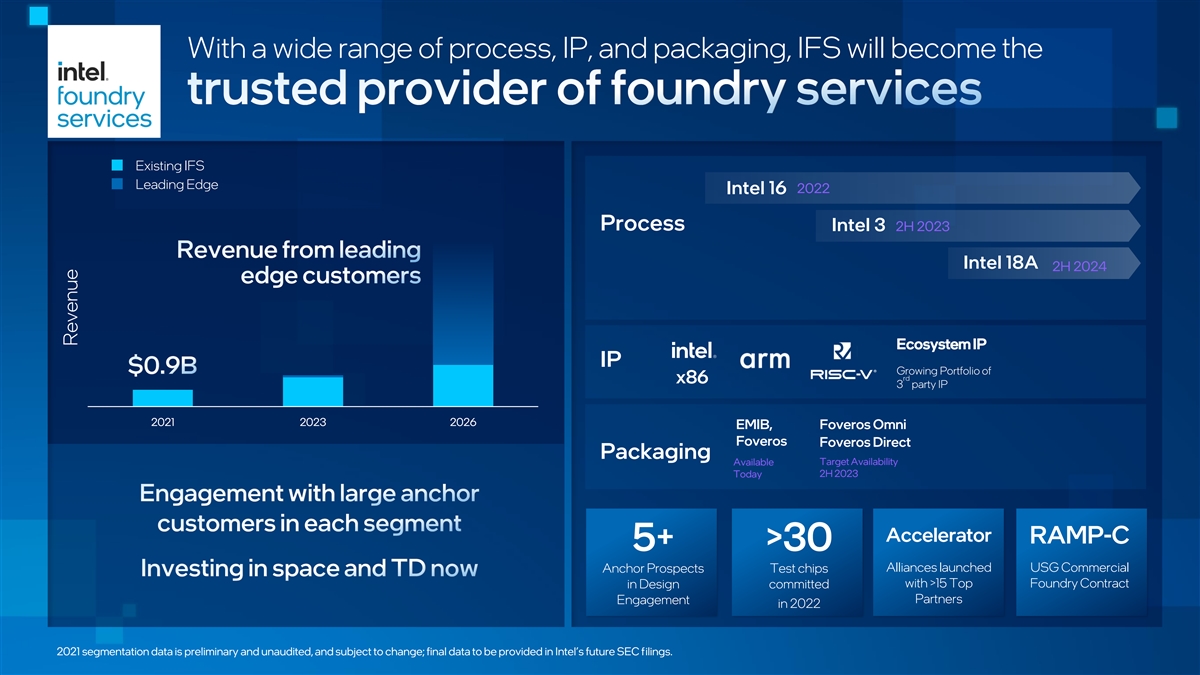

With a wide range of process, IP, and packaging, IFS will become the Existing IFS Leading Edge 2022 Intel 16 Process Intel 3 2H 2023 Intel 18A 2H 2024 Ecosystem IP IP Growing Portfolio of rd x86 3 party IP 2021 2023 2026 EMIB, Foveros Omni Foveros Foveros Direct Packaging Available Target Availability Today 2H 2023 Accelerator RAMP-C 5+ >30 Anchor Prospects Test chips Alliances launched USG Commercial with >15 Top Foundry Contract in Design committed Engagement Partners in 2022 2021 segmentation data is preliminary and unaudited, and subject to change; final data to be provided in Intel’s future SEC filings. Revenue

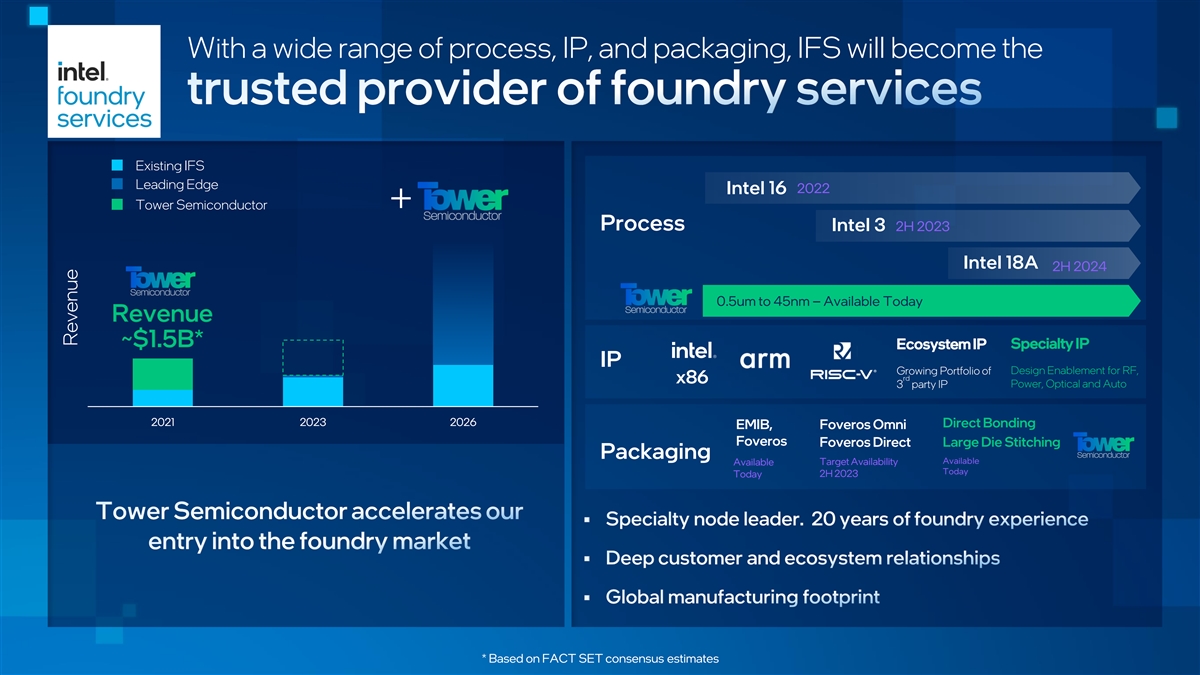

With a wide range of process, IP, and packaging, IFS will become the Existing IFS Leading Edge 2022 Intel 16 Tower Semiconductor Process Intel 3 2H 2023 Intel 18A 2H 2024 0.5um to 45nm – Available Today Revenue ~$1.5B* Ecosystem IP Specialty IP IP Design Enablement for RF, Growing Portfolio of rd x86 Power, Optical and Auto 3 party IP 2021 2023 2026 Direct Bonding EMIB, Foveros Omni Foveros Foveros Direct Large Die Stitching Packaging Available Available Target Availability Today Today 2H 2023 * Based on FACT SET consensus estimates Revenue

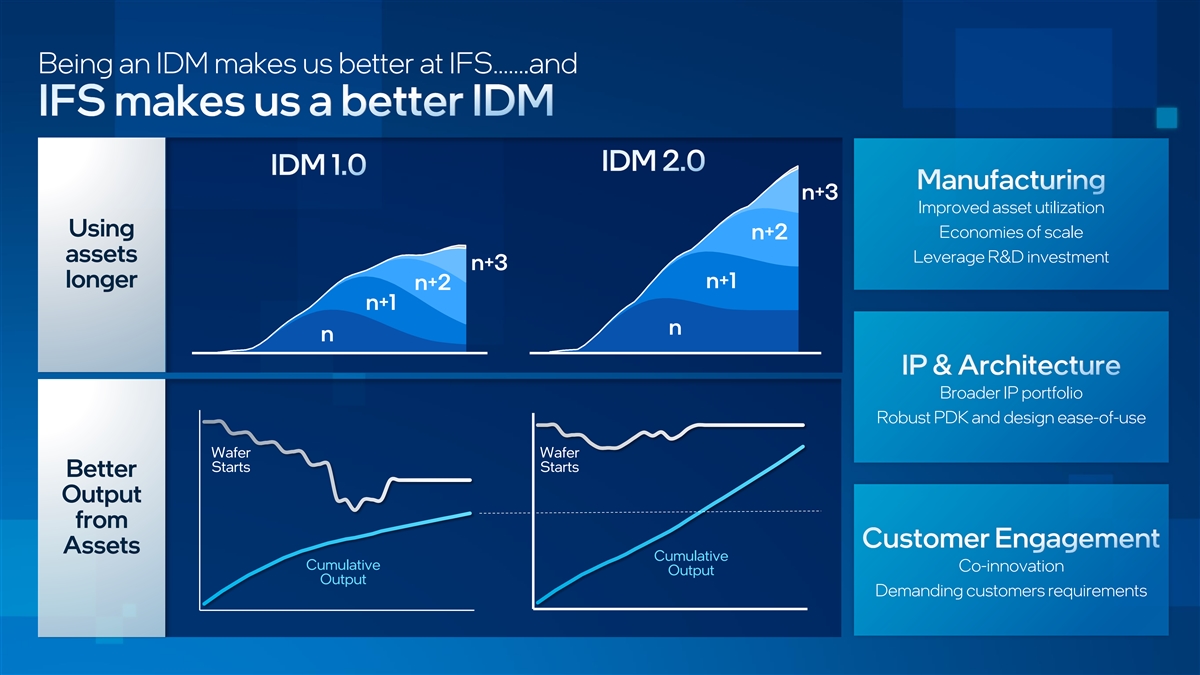

Being an IDM makes us better at IFS…….and n+3 Improved asset utilization Using Economies of scale n+2 assets Leverage R&D investment n+3 longer n+1 n+2 n+1 n n Broader IP portfolio Robust PDK and design ease-of-use Wafer Wafer Starts Starts Better Output from Assets Cumulative Cumulative Co-innovation Output Output Demanding customers requirements

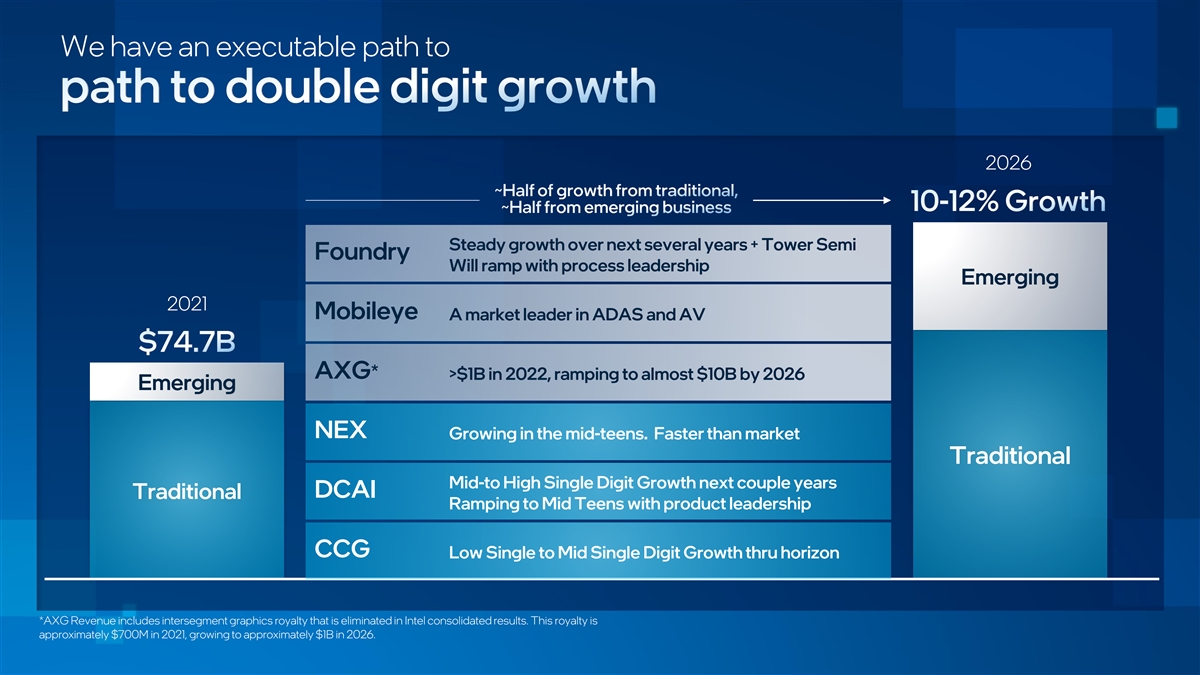

We have an executable path to 2026 Steady growth over next several years + Tower Semi Foundry Will ramp with process leadership Emerging 2021 Mobileye A market leader in ADAS and AV AXG* >$1B in 2022, ramping to almost $10B by 2026 Emerging NEX Growing in the mid-teens. Faster than market Traditional Mid-to High Single Digit Growth next couple years DCAI Traditional Ramping to Mid Teens with product leadership CCG Low Single to Mid Single Digit Growth thru horizon *AXG Revenue includes intersegment graphics royalty that is eliminated in Intel consolidated results. This royalty is approximately $700M in 2021, growing to approximately $1B in 2026.

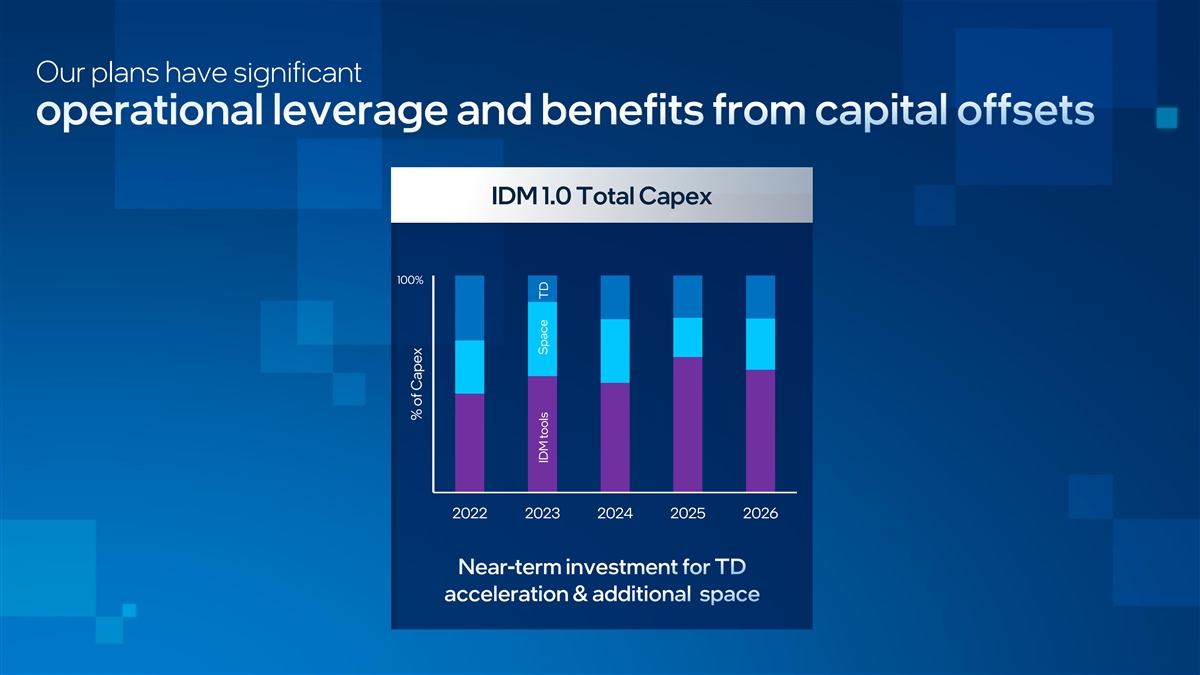

Our plans have significant IDM 1.0 Total Capex 100% 2022 2023 2024 2025 2026 % of Capex IDM tools Space TD

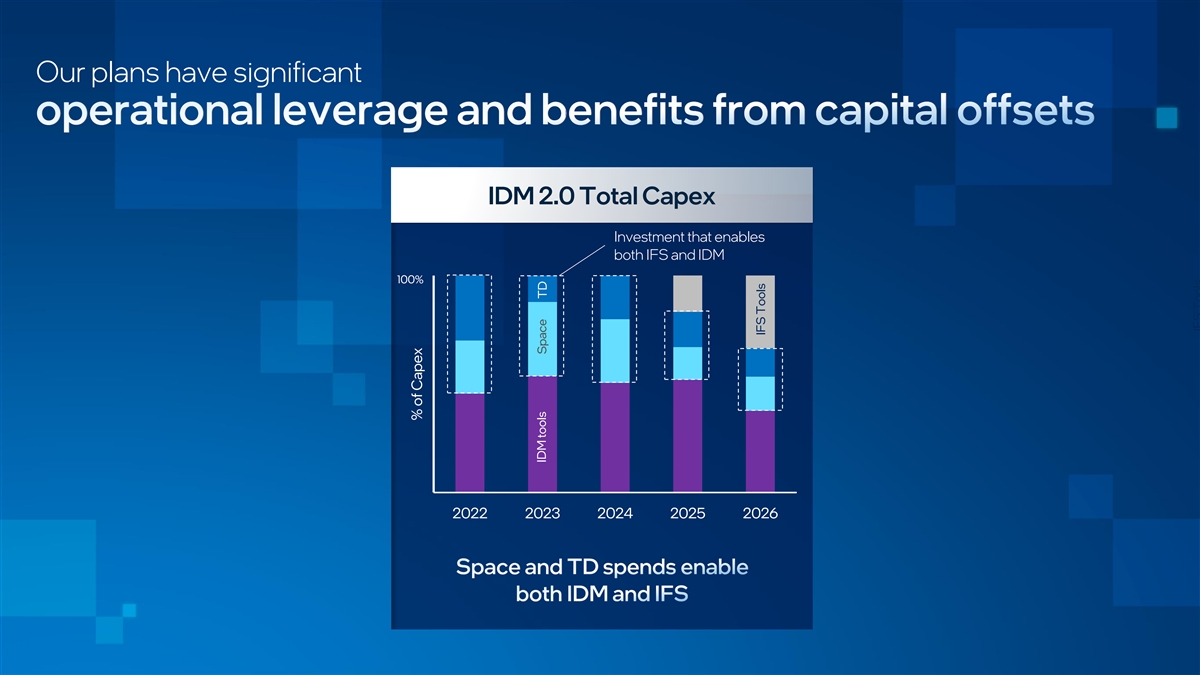

Our plans have significant IDM 2.0 Total Capex Investment that enables both IFS and IDM 100% 2022 2023 2024 2025 2026 % of Capex IDM tools Space TD IFS Tools IFS Tools

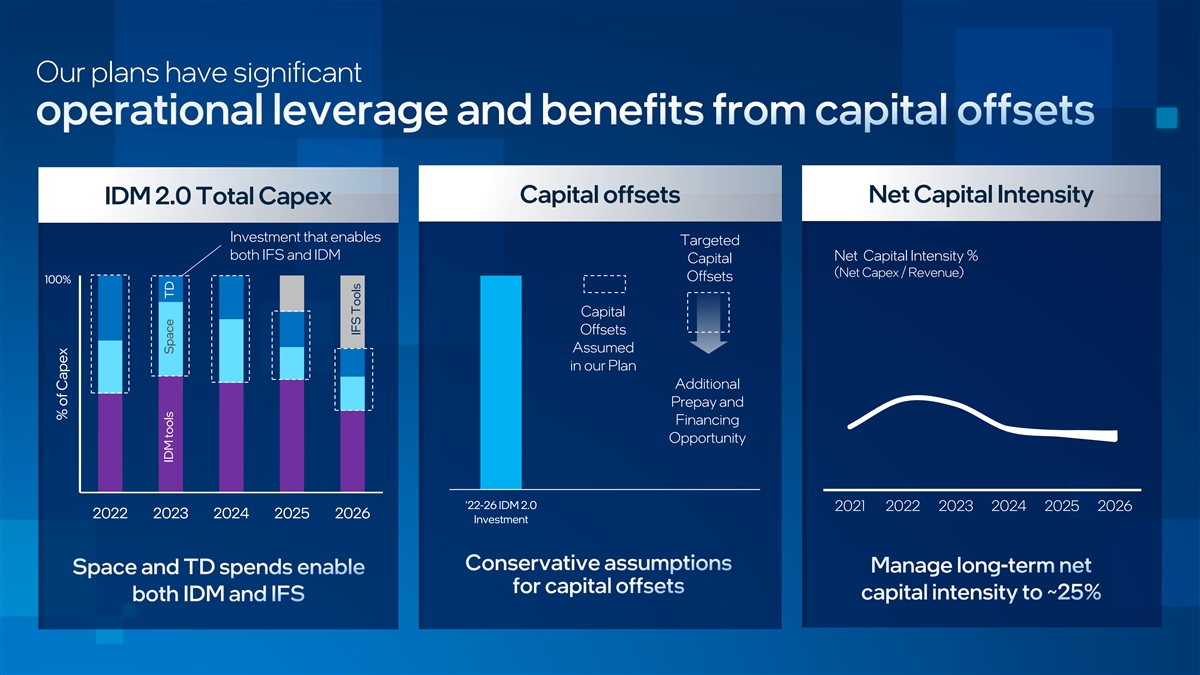

Our plans have significant Capital offsets Net Capital Intensity IDM 2.0 Total Capex Investment that enables Targeted both IFS and IDM Net Capital Intensity % Capital (Net Capex / Revenue) Offsets 100% Capital Offsets Assumed in our Plan Additional Prepay and Financing Opportunity '22-26 IDM 2.0 2021 2022 2023 2024 2025 2026 2022 2023 2024 2025 2026 Investment % of Capex IDM tools Space TD IFS Tools

Our Beliefs Our Strategy Our Execution 1 We are in an era of sustained, Deliver leadership products… long-term demand Foundry The insatiable need for 2 …Anchored on compute drives the value of open and secure platforms Accelerated Moore’s Law IDM 2.0 Auto & Compute & Mobility Graphics Software & Security Open ecosystems unleash 3 …Powered by sustainable innovation and democratize manufacturing at scale compute Data Network & Client Center & Edge The world needs more AI 4 …Supercharged balanced and resilient by our people and culture supply chains

To Date 1H’22 2H’22 Alder Lake Sapphire Raptor Ramp Rapids Lake Alchemist Ponte shipping Vecchio Intel Manufacturing Shipping 7 Ready Ohio EU Mobileye IPO IFS Anchor Customer

To Date 1H’22 2H’22 2023 2024 Arrow Alder Lake Sapphire Raptor Meteor Lake Ramp Rapids Lake Lake Granite Sapphire Alchemist Rapids & Ponte Emerald Rapids HBM shipping Vecchio Sierra Rapids Forest Intel Manufacturing Shipping 7 Ready Ohio EU Manufacturing Ready Mobileye IPO IFS Anchor Customer

Participating in high-growth markets Sustainable competitive advantages Executing the right strategy Strong leadership and culture Innovative ways to unlock shareholder value